When choosing a salary vs dividend mix as a UK limited company director, the most tax-efficient strategy is a blended approach: taking a low, tax-optimised salary to secure your State Pension and utilise tax allowances, supplemented by dividends to avoid National Insurance completely.

Balancing this mix can be tricky, as Sarah recently discovered.

On a rainy Tuesday evening, she sat at her kitchen table, ready to transfer a hard-earned bonus from her boutique design agency’s healthy bank account to her personal one. But before hitting “confirm,” she remembered a warning from a fellow business owner: “If you take it as a standard salary, HMRC will take a massive chunk—but if you draw only dividends without the right paperwork, you risk failing a compliance audit.”

Sarah closed the app, frustrated. She is caught in the same dilemma facing thousands of UK directors for the 2026/27 tax year. Extracting your hard-earned profits shouldn’t feel like a high-wire act. Getting your director remuneration UK strategy right is the single best way to maximise your take-home pay while staying fully compliant with HM Revenue & Customs (HMRC).

Let’s look at what has changed, how the system works this year, and how to find the optimal salary for directors in the UK to keep more money in your pocket.

What’s the Difference Between Salary and Dividends?

For designing a tax-efficient pay structure, the first thing to get clear is that HMRC views your salary and your company’s dividend paid as two distinct financial concepts. Each is treated and taxed in a different way and will have entirely different effects on the company’s financial statements.

1. Director’s Salary

A salary is a fixed and regular amount paid by the limited company to you as an employee or director.

Tax Mechanics: It is paid through the formal PAYE (Pay As You Earn) payroll scheme. It is subject to personal Income Tax and Class 1 Primary (employee) and Secondary (employer) National Insurance Contributions (NICs) if it is above a certain statutory threshold (£1,048 per month).

The Corporate Benefit: For the company, a director’s salary is considered a business expense. Which means from your company’s revenue, the total gross salary and the employer’s national insurance of the director will be deducted before the profits are calculated. This reduces the corporation tax.

For example, considering that the gross salary of the director is £12,570, this is the most popular and tax-effective strategy that is adopted for UK limited company directors. For this exact amount of salary, you will be getting the maximum tax perks, which include:

- Income Tax—£0 (since it perfectly matches your personal allowance)

- Employee NI – £0 (Since it is placed right at the primary threshold)

- State Pension Credits (Since you are building your state pension record for free). Since your salary is more than the National Insurance Lower Earnings Limit (LEL) of £6,708.

However, in this case, the Employer’s National Insurance will be working differently based on whether you are a sole director or have team members.

Let us consider that you are a Sole Director (which means no other employee is working in your company)

If you are the only one on your company’s payroll, you are not eligible to claim the Employment Allowance out of your employer’s tax. In such a case, the company’s expense will be:

- Salary Expense: Where your company pays you £12,570.

- Employer NI Expense: The company pays at 15% on everything above the threshold of £5,000.

Calculation of Employer NI

- 15% X (Gross Salary – Employer NI Threshold)

- 15% X (£12,570 – £5,000)

- 15% X £7,570 = £1,135.50

Total tax deduction for the Company: Your company can claim both costs as allowable business expenses. Therefore, your company will be deducting £13,705.50 (£12,570 + £1,135.50) from its revenue to reduce its corporate tax bill.

Now, let us consider the scenario where you have employees or multiple directors in your company

- Assuming that there are atleast five people on the payroll and they are earning above the threshold. In such situations, you qualify for the £10,500 Employment Allowance.

- Salary Expense: Where your company pays you £12,570.

- Employer’s NI Expense: Nominally £1,135.50, as calculated above. However, here the HMRC’s allowance will reduce this bill to £0.

- Total tax deduction for the Company: The company deducts exactly £12,570 from its revenue to reduce the corporate tax bill.

Corporation Tax Dynamics

Corporation Tax rates for 2026-27:

- 19% Small Profits rate — profits under £50,000

- 25% Main rate — profits over £250,000

- Marginal Relief — applies between £50,000 and £250,000 (effective rate tapers from 19% to 25%)

2. Company Dividends

Dividends are the payments of a company’s net income to its shareholders. To draw dividends, you must be a shareholder in the business.

- Tax Mechanics: Dividends are 100% free from National Insurance Contributions. This is one of the biggest advantages. But when they exceed your annual tax-free allowance, they are subject to personal Dividend Income Tax.

- Corporate Catch: Unlike a salary, dividends do not count as a business expense. These are not available to offset your company’s Corporation Tax bill. In addition, under UK company law, your company can only lawfully declare and pay dividends if there are enough “distributable reserves” to cover all operational expenses and corporation tax liabilities that are to be paid.

What’s Changed in 2026/27? (Key Tax Updates)

In case you are still seeking tax advice from a few years ago, you are likely paying too much tax. Several significant legislative changes have come into effect in the 2026/27 tax year, which will dramatically impact small company director tax planning.

Dividend Tax Rate Increase

The tax rates on dividend income above the personal allowance have officially increased by 2% in both the basic and higher rate bands, although the amount of the allowance is still frozen at £12,570, and the tax-free dividend allowance remains at a modest £500.

Dividend tax rates for 2026/27 are as follows:

- Basic Rate Band: Risen to 10.75% (up from 8.75%)

- Higher Rate Band: Risen to 35.75% (up from 33.75%)

- Additional Rate Band: Continues to be static at 39.35%.

Why Most Directors Still Use the Optimal Salary + Dividends Combination

Despite the recent 2% hike in dividend tax rates, the absolute most tax-efficient method for owner-managers to extract profit is to implement a blended strategy: taking a specific, mathematically optimised low salary, supplemented by the remainder of their income in dividends.

For the majority of directors in 2026/27, for pulling our the money safely, the directors tend to top up their base salary by using dividends. Let us understand how this is possible through an example.

Assuming you want the total income of £50,270 annually, which means

- Your salary will be £12,570 – this will leave you with £0 personal tax on this portion.

- Your dividends will be £37,700 (£50,270 – £12,570). This will result in a very low tax rate. So you will be taking home the maximum amount of income.

To illustrate this, below is the full personal tax calculation for your reference based on the 2026-27 rate bands.

Step 1: Your Income Tax on the £12,570 Salary

Your personal allowance covers your entire salary.

- Salary Income: £12,570

- Minus Personal Allowance: -£12,570

- Taxable Salary: £0

- Income Tax Owed: £0

Step 2: Your National Insurance (NI) on the Salary

Because £12,570 matches the Primary Threshold (£12,570/year or £1,048/month for 2026/27), you trigger zero employee contributions.

- Employee NI Owed: £0

Step 3: Your Dividend Tax on the £37,700 Dividends

Dividends are stacked on top of your salary. Since your salary used up the Personal Allowance, the dividends are taxed using investment rules.

Apply the Dividend Allowance: The first £500 of your dividends is completely tax-free.

- £37,700 – £500 = £37,200 taxable dividends

Calculate the Tax (Basic Rate): The remaining £37,200 falls entirely into the basic rate band (£0–£37,700), which is taxed at 10.75%.

- £37,200 × 10.75% = £3,999.00

The Final Personal Summary

By structuring your payments this way, you pull over £50,000 out of your company while keeping your personal tax bill remarkably low.

- Total Income Received: £50,270 (£12,570 salary + £37,700 dividends)

- Total Personal Tax Owed: £3,999.00 (Paid via Self Assessment)

- Your Net Take-Home Pay: £46,271.00

When salary works better than dividends

Though lower salary, high dividends are the norm, there are certain situations where it makes more financial sense to ramp up the salary.

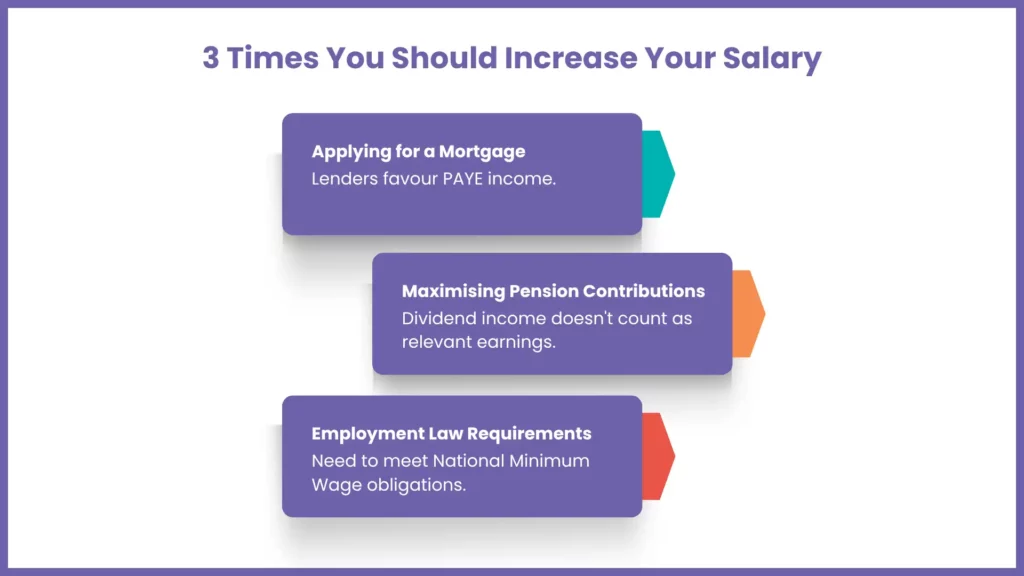

- Securing Personal Borrowing: When you are in the process of applying for a commercial or residential mortgage, the mortgage lender will typically prefer steady salary income (PAYE) over fluctuating or profit-dependent salary income (dividends).

- Maximising Pension Contributions: The rules of personal tax relief for pension contributions into a private pension scheme are capped at 100% of relevant UK earnings (or £60,000). More importantly, dividend income is not considered relevant earnings. For those preferring to make large personal contributions, a higher salary is a prerequisite.

- Fulfilling Contracts of Service: If your role as a director is bound by a formal contract of service that classifies you as an active employee for employment law purposes, you are legally obligated to receive at least the National Minimum Wage via payroll.

When Dividends Are the More Tax-Efficient Choice

Dividends are best when your business is consistently making profitable money and you want to take some money out with maximum flexibility.

- Zero National Insurance Exposure: There is no National Insurance exposure till your personal earnings exceed the £12,570 threshold, after which any additional income from salary is subject to a combined tax and National Insurance rate that quickly surpasses the dividend tax rate. Dividends remain the cost-effective option for drawing funds within the basic rate band, even after accounting for Corporation Tax.

- Flexibility in Lean Months: Unlike a fixed contractual salary that must be paid through payroll each month, regardless of performance, dividends can be declared dynamically. If your company experiences a seasonal dip or a cash crunch, you can simply choose not to declare a dividend, preserving vital working capital within the business structure

Salary vs Dividends 2026/27 — Quick Reference Table

Here is a structural overview to illustrate how these two remuneration elements will work together as per the 2026/27 guidelines.

| Feature | Director Salary (PAYE) | Company Dividends |

| National Insurance (NICs) | Yes (Subject to thresholds) | No (Completely exempt) |

| Corporation Tax Deductible | Yes (Reduces company profit) | No (Paid from post-tax profit) |

| Impact on State Pension | Builds qualifying years (above £6,708) | No impact |

| Payment Limitations | Can be paid even if the company makes a loss | Legally requires distributable reserves |

| 2026/27 Basic Rate Tax | 20% | 10.75% |

| 2026/27 Higher Rate Tax | 40% | 35.75% |

How to Get the Salary vs Dividends Mix Right in 2026/27

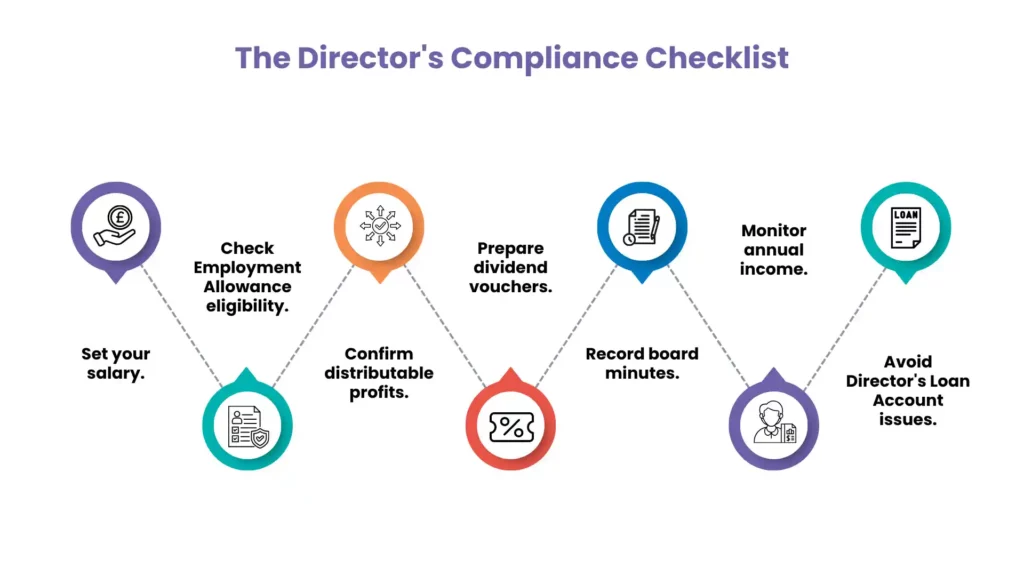

This must be performed in an excellent manner. Use your business bank account like a business bank account; never use it as your personal wallet. Any random miscellaneous transfers from your business account, without real-time documentation, could lead to a risky, messy, overdrawn “Director’s Loan Account” with HMRC, for which you could trigger some serious Section 455 tax penalties.

Irrespective of whether you are the sole director or not, every time you issue a dividend, you need to formalise it by creating a written dividend voucher and recording brief board minutes.

Lastly, check your cumulative total income across the year. If you are earning more than the basic rate limit of £50,270, your personal tax liability will automatically increase from 10.75% to a high tax rate of 35.75% on excess dividends.

How MyIva Can Help You Optimise Your Salary vs Dividends

Determining the right balance between salary vs dividends isn’t always straightforward. While a £12,570 salary combined with dividend payments is often the most tax-efficient approach for many directors, every business has unique circumstances that can affect the ideal strategy.

At MyIva, we help limited company directors create tailored remuneration plans that maximise tax efficiency while ensuring full HMRC compliance. Our experienced accountants stay up to date with the latest tax legislation, dividend tax rates, National Insurance thresholds, and Corporation Tax rules, helping you make informed decisions throughout the year.

Our services include:

- Reviewing your current salary and dividend structure.

- Identifying opportunities to reduce your overall tax liability.

- Managing PAYE payroll and director salary calculations.

- Preparing dividend vouchers and maintaining proper documentation.

- Advising on Corporation Tax and profit extraction strategies.

- Supporting mortgage applications by helping structure director remuneration appropriately.

- Providing proactive tax planning to avoid unexpected liabilities.

- Ensuring compliance with HMRC and Companies House requirements.

Whether you’re a new company director or an established business owner, MyIva can help you create a tax-efficient strategy that protects your profits while keeping your business fully compliant.

Stop Overpaying Tax on Your Own Profits

Most UK directors leave thousands on the table every year through the wrong salary and dividend mix. Our accountants will map out your optimal structure for 2026/27 — fully compliant, fully personalised.

Frequently Asked Questions (FAQs)

Is it better to pay dividends or a salary in the UK?

A combination is best for most small business directors. A low tax-efficient salary of £12,570 would utilise your personal allowance, ensuring that you receive your state pension, while taking the remainder of your required income as dividends avoids unnecessary National Insurance charges.

Can I pay myself only dividends and no salary?

Yes, legally, as long as your company has money for post-tax profits for distribution. But it is usually not the best. This not only means that you are not claiming any Corporation Tax allowances, but you are also not earning any qualifying years for the UK state pension.

What is the 60% tax trap?

In the UK, if your total personal income (from all sources combined) is between £100,000 and £125,140, your tax-free personal allowance is reduced by £1 for every £2 of income above £100,000. This leads to an effective marginal tax rate of 60% in this particular income range.

Does the Employment Allowance reduce my director’s National Insurance?

£10,500 Employment Allowance will be available to the employer to reduce their National Insurance contributions; however, the allowance is not available to a company where the sole director is the only employee. Where you have two or more directors/employees on the payroll, this allowance will be able to offset the employer NIC cost completely.

Are dividends taxed differently for Scottish taxpayers?

No. Dividend rates are UK-wide, but Scottish income tax bands differ for non-savings/non-dividend income.

Conclusion

Profit extraction does not have a single “one-size-fits-all” approach, as it will vary based on the profitability of your business, the nature of your family, and your long-term wealth objectives. But, as the 2026/27 tax year adjustments demonstrate, proactive planning is no longer a choice to make; it is a necessity.

With the best £12,570 baseline salary and dividend distributions mapped out systematically, you can now do your bit to navigate through the recent tax hikes with complete confidence. Don’t wait till the end of the year to estimate how much you will be rewarded. By working with a specialist small business accountant, you can ensure that your corporate and personal tax positions are aligned to keep your business in compliance and to maximise your real take-home wealth.

Ready to Maximise Your Take-Home Income?

Choosing the right salary vs dividend mix can save you thousands in unnecessary tax each year. Don’t leave your director’s remuneration strategy to guesswork.

Speak to MyIVA’s expert accountants today for personalised advice on salary planning, dividend extraction, Corporation Tax, and overall tax efficiency. We’ll help you structure your income most effectively while ensuring complete HMRC compliance.

Contact MyIva today and discover how much more of your hard-earned profits you could keep