You’ve built your business from the ground up. You are down the long road, you have found your place, and now the numbers are quite good. As you get more successful, though, the news likely brings up a question you’ve been asking yourself: Am I paying too much tax?

Quick answer: In 2026/27, most UK accountants recommend switching from a sole trader to a limited company when your annual profits consistently exceed £50,000. Below this level, the extra accountancy costs and administrative burden typically outweigh the tax savings — particularly given the reduced Dividend Allowance of just £500 from April 2024.

One of the biggest financial choices you’ll make as a business owner in the UK is between being a sole trader vs limited company. As a sole trader, it’s an easy, quick and natural first step for many and provides you with 100% independence. However, as your profits climb, the tax efficiency of a limited company becomes harder to ignore.

In this guide, we will examine the differences between a sole trader and a limited company, including the profit threshold at which incorporation becomes worthwhile, and when the switch to a limited company is the best choice for the 2026/27 tax year.

What Is a Sole Trader and What Is a Limited Company in the UK?

Before getting into the numbers, it’s important to have an understanding of the basic legal structures.

You as a Sole Trader

If you work as a sole trader, then you are the business. Your personal assets are not clearly separated from your business assets. You retain 100% of the profits after tax but are also personally responsible for all the debts of the business. Your belongings, such as your home, may be vulnerable if your business fails.

You as a Limited Company

A limited company is an entity distinct from you. It is a legal entity and can have its own legal persona, i.e. assets, liabilities and obligations. Your personal liability will be restricted to the amount invested by you or guaranteed to the company as a director and shareholder of the company. This “corporate veil” gives it some protection that a sole trader doesn’t.

Sole Trader vs Limited Company — Key Differences at a Glance

When you are weighing your options, you shouldn’t just look at the tax bill. You need to consider the administrative and legal realities of the difference between a sole trader and a limited company.

| Sole Trader | Limited Company | |

| Liability | You have unlimited personal liability | Your liability is limited |

| Privacy | Your business is private; you are a sole trader | You have to submit accounts and information on “Persons with Significant Control” to Companies House, which is made public |

| Administration | A sole trader has minimal paperwork (Self Assessment) | There is a lot of administration involved in limited companies, such as filing Annual Returns, Statutory Accounts and Corporation Tax returns. |

| Registration Cost | Free to register as self-employed | £50 online via Companies House |

| Making Tax Digital | MTD for Income Tax applies from April 2026 (income >£50k) and April 2027 (income >£30k). Quarterly digital submissions required. | MTD for Corporation Tax is still in consultation — no mandatory date confirmed for 2026/27. |

| Perception | Some clients prefer dealing with Ltd companies | “Ltd” can help win larger contracts and appear more established |

How Are Sole Traders and Limited Companies Taxed Differently in the UK? (2026/27)

Understanding sole trader vs limited company tax is usually the primary driver for switching. The two structures are taxed in completely different ways.

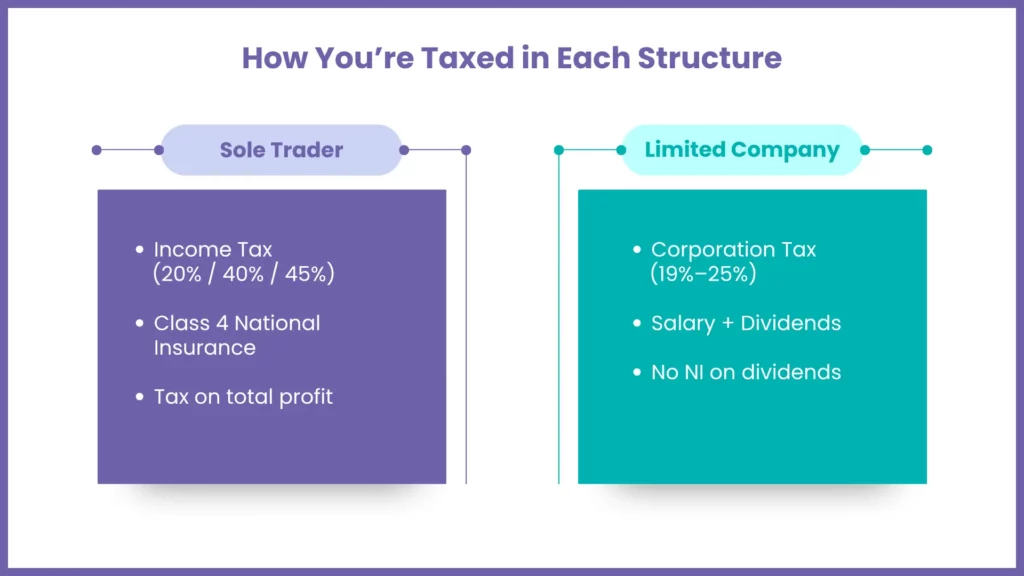

How Is a Sole Trader Taxed in the UK?

As a sole trader, you pay Income Tax on your business profits. You are entitled to a Personal Allowance — frozen at £12,570 for 2026/27 — the amount you earn before you pay tax. Once you exceed this, you pay tax at the following rates:

- Basic Rate (20%) on profits from £12,571 to £50,270

- Higher Rate (40%) on profits from £50,271 to £125,140

- Additional Rate (45%) above £125,140

Note: Your Personal Allowance tapers by £1 for every £2 of income above £100,000, reducing to nil at £125,140.

In addition to Income Tax, you must pay Class 4 National Insurance Contributions (NICs) on your profits. For 2026/27, the rates are:

- 6% on profits between £12,570 and £50,270

- 2% on profits above £50,270

Note: Class 2 NICs were abolished from 6 April 2024.

How Is a Limited Company Taxed in the UK?

A limited company pays Corporation Tax on its profits after all business expenses have been deducted.

For 2026/27, Corporation Tax rates are:

- 19% Small Profits Rate — on profits up to £50,000

- 25% Main Rate — on profits above £250,000

- Marginal Relief applies on profits between £50,001 and £249,999, tapering the effective rate between 19% and 25%

To get money out of the company and into your pocket, you typically use a combination of:

- A Low Salary: For 2026/27, the optimal director salary is typically £12,570 (the Personal Allowance) if you are the sole employee, or £9,100 (the Secondary Threshold) to avoid employer NICs. The right level depends on your circumstances.

- Dividends: Paid out of distributable profits after Corporation Tax. For 2026/27, the Dividend Allowance is £500 (reduced from £1,000 in 2023/24). Above this, dividend tax rates are: 10.75% (basic rate), 35.75% (higher rate), 39.35% (additional rate). Dividends do not attract National Insurance.

At What Profit Level Should You Switch from Sole Trader to Limited Company?

In 2026/27, the profit threshold at which switching becomes worthwhile is approximately £50,000–£60,000 in annual profit. Below this level, additional accountancy costs and administration typically cancel out the tax savings — especially with the Dividend Allowance now just £500.

Historically, the tipping point was around £25,000. However, the reduction of the Dividend Allowance to just £500 (from April 2024) means the real-world saving below £50,000 is now marginal at best. Most UK accountants now place the tipping point firmly at £50,000–£60,000 for 2026/27.

Below this level, the added costs of accountancy fees (which can be £1,000–£1,500+ more per year for a company) and the time spent on admin might outweigh the small tax savings.

Other Reasons to Switch to a Limited Company Beyond Tax Savings

Tax isn’t everything. You might find that a limited company is better for you even if the tax savings are small.

- Limited Liability: If your business carries risk (e.g., you have employees, large contracts, or high overheads), the protection of your personal assets is invaluable.

- Brand Image: Some clients view “Ltd” as a sign of a more “serious” business. It can help you win bigger contracts.

- Pension Planning: Limited companies can make direct employer contributions into your pension, which is a highly tax-efficient way to move money out of the business. Employer pension contributions are fully deductible from Corporation Tax profits and do not attract employer National Insurance — making this one of the most powerful tools available to a limited company director.

- Raising Capital: If you want to bring in investors or sell shares in the future, you must be a limited company.

- Business Asset Disposal Relief (BADR): If you ever sell your limited company, you may qualify for BADR (formerly Entrepreneurs’ Relief), taxing the gain at just 10% Capital Gains Tax up to a lifetime limit of £1 million — a significant long-term incentive unavailable to sole traders.

Reasons to Stay as a Sole Trader Instead of Going Limited

Don’t feel pressured to switch just because your profits are up. There are valid reasons to stay as you are:

- Simplicity: You have much less “red tape”.No need to worry about payroll, complex annual accounts, or Companies House filings.

- Privacy: Your earnings and business details stay between you and HMRC.

- Lower Costs: Your accounting fees will be significantly lower, and you won’t have to pay the £50 registration fees to Companies House.

- Losses: If your business makes a loss, you can sometimes offset these losses against your other personal income, which is more flexible than for a limited company.

- MTD simplicity: Until MTD for Income Tax applies to you (see thresholds in FAQ below), sole trader filing remains a single annual Self Assessment return — simpler than the quarterly reporting and payroll involved in running a limited company.

How to Switch from Sole Trader to Limited Company in the UK

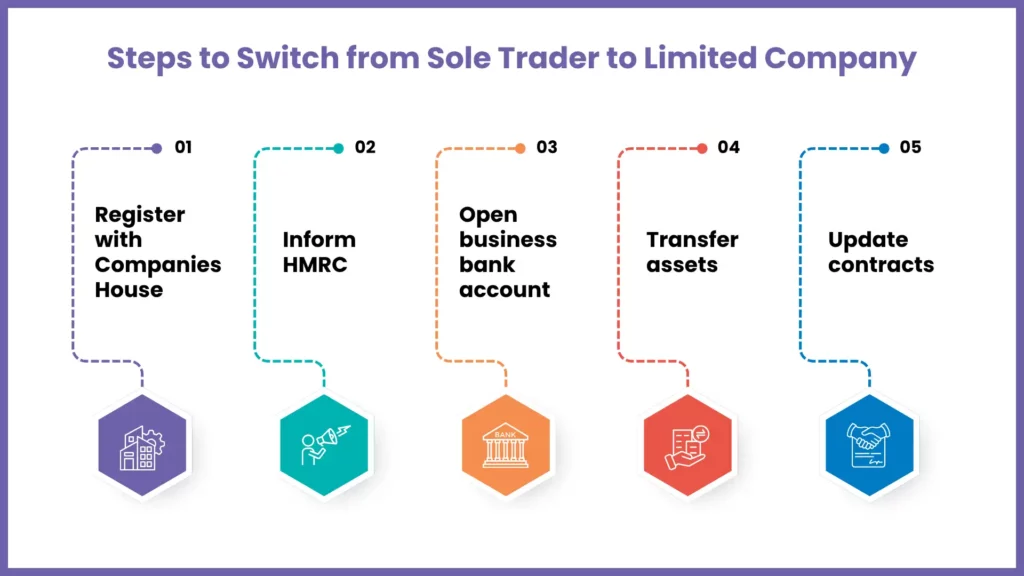

If you’ve decided the time is right, here is how you make the jump:

- Incorporate: Register your new limited company with Companies House. The online process takes approximately 24 hours and costs £50. You will receive a Certificate of Incorporation and a unique Company Registration Number (CRN).

- Inform HMRC: Tell them you are ending your sole trader business and starting a limited company. You must register the company for Corporation Tax within 3 months of starting to trade.

- Business Bank Account: You must open a separate business bank account for the company. You cannot use your personal account.

- Transfer Assets: Any equipment or vehicles used by the sole trader business need to be transferred or sold to the new company. Be aware that this can trigger Capital Gains Tax — take advice before doing so.

- Update Contracts: Ensure all your clients, suppliers, and insurance providers are informed of the change in legal status.

- Set up Payroll: As a director taking a salary, you must register as an employer with HMRC and operate PAYE.

How MyIVA Can Help You Navigate Your Business Growth

While growing a business is exciting, it can also be very complex financially. From settling business debts to simply restructuring their finances for greater stability, MyIVA’s here for them. We are experts at assisting sole traders and limited companies in navigating their financial situations. When the need to change structures or handle overheads begins to become too much to handle, our experts can offer customised guidance to shield your future and keep your business going.

FAQs: Frequently Asked Questions

Who pays more tax — a sole trader or a limited company?

It depends on your profit. Generally, at profits above £50,000–£60,000, a limited company is more tax-efficient. At lower profit levels, a sole trader may pay less once you factor in accountancy costs and the reduced Dividend Allowance of £500 for 2026/27.

When should I go from sole trader to limited company?

When your profits consistently exceed £50k-£60k, or when you need the protection of limited liability for your personal assets.

Is it better to be a sole trader or a limited company?

There is no “best” option. It’s a trade-off between the simplicity of being a sole trader and the tax efficiency and protection of a limited company.

Can I switch back to being a sole trader if I don’t like it?

Yes, you can close your limited company and return to being a sole trader, but the process of “winding up” a company can be complex and may have tax implications. Take professional advice before closing.

Do I need an accountant to go limited?

While not legally required, it is highly recommended. The tax rules and filing requirements for companies are much stricter than for sole traders.

What is the optimal salary for a limited company director in 2026/27?

Typically £12,570 (the Personal Allowance) if you are the sole employee, or £9,100 (the Secondary Threshold) to avoid employer NICs. Your accountant will advise on the right level for your situation.

What is IR35, and does it affect my decision to go limited?

IR35 determines whether HMRC views your working arrangement as genuine self-employment or disguised employment. If your contracts are deemed inside IR35, you pay tax like an employee — wiping out most of the limited company tax advantage. If you’re outside IR35, a limited company still works in your favour. Speak to a specialist accountant before incorporating.

Does Making Tax Digital (MTD) affect sole traders in 2026?

Yes. From April 2026, sole traders earning above £50,000 must submit quarterly digital updates to HMRC instead of one annual return. The threshold drops to £30,000 from April 2027. This narrows the simplicity advantage sole traders traditionally held over limited companies.

Does Making Tax Digital affect limited companies?

MTD for Corporation Tax is still in consultation for 2026/27 — no mandatory start date has been confirmed. Limited companies face less immediate MTD pressure than sole traders at this stage.

Conclusion

The journey from sole trader to limited company is a rite of passage for many UK entrepreneurs. For the 2026/27 tax year, the decision remains a balance of tax efficiency, legal protection, and administrative appetite. With the Dividend Allowance now reduced to just £500, the real tipping point is closer to £50,000–£60,000 in annual profit — and IR35 status, MTD obligations, and your long-term plans all play a part in the decision. If you value simplicity and privacy, staying as a sole trader might be your best bet. If you are looking to scale, protect your assets, and minimise your tax bill, going limited is likely the right move.

Take the Next Step for Your Business Success

Don’t let tax confusion or financial stress hold your business back. Choosing the right structure is about more than just today’s profit—it’s about your long-term security.

Are you ready to optimise your business finances? Whether you need a professional review of your tax position or advice on managing business debt, reach out to the experts today.

Contact MyIVA for a Free Consultation and take control of your financial future!