Did you know that UK companies claimed around £7.6 billion in R&D Tax Relief support in the latest HMRC figures for the 2023–24 tax year? This figure shows how important tax incentives can be for firms that are pushing boundaries and solving problems, especially when you consider that this represents support for tens of thousands of businesses across the nation.

If you run a small business, have staff grappling with technical challenges, understanding R&D Tax Relief can be a financial advantage. It is not a niche benefit reserved for big science labs or tech giants. From software development to product innovation, there are ways to reduce your corporation tax bill or receive tax credits by recognising eligible costs you have already incurred.

In this blog you will learn:

• What R&D Tax Relief is and how it works under the latest rules.

• Who can claim and what counts as qualifying activity.

• The costs you can include in an R&D claim.

• Which scheme applies to your business in 2026 and the relevant R&D tax credit rates.

• A step‑by‑step guide to completing an R&D claim process in the UK and common FAQs.

What Is R&D Tax Relief?

R&D Tax Relief is a government incentive designed to encourage UK small business to invest in innovation by reducing the overall tax they must pay. It is available through allowances that reduce taxable profits or as a payable tax credit if the company is loss‑making. Simply put, it rewards firms for spending on research and development projects that seek to advance technology or knowledge.

This relief applies when a company incurs costs on projects that seek to resolve scientific or technical uncertainty and use an appreciable level of resource to do so. The focus is not on success, but on the attempt to solve problems that cannot be easily resolved by a professional in the field. If your business has spent money on developing or improving products, services or processes in a way that goes beyond routine activities, you may be able to claim.

R&D Tax Relief allows small businesses of all sizes to recover a portion of qualifying expenditure and potentially improve cash flow, especially useful for smaller companies and start‑ups.

How R&D Tax Relief Works (2026 Rules Explained)

Under the updated regime for R&D Tax Relief from April 2024, HMRC merged previous schemes to simplify claiming and support innovation more effectively.

Key Points in the Claim Process

Merged Scheme for All Businesses

The old SME regime and classic RDEC scheme have been combined into a single merged RDEC-style scheme system for accounting periods beginning on or after April 2024. This makes the claim criteria and calculation more consistent across business sizes.

Enhanced Support for R&D Intensive SMEs

Loss‑making SMEs that meet a higher R&D spending threshold (at least 30% of total expenditure) can qualify for enhanced support under the ERIS rules, meaning potentially greater tax benefits if R&D costs make up a significant part of total expenditure.

What R&D Tax Relief Does for You

• Reduces your corporation tax bill through enhanced deductions.

• Provides a tax credit if your business is making a loss.

• Improves cash flow by reclaiming money spent on qualifying R&D activities.

In practice, this means that when you prepare your corporation tax return, you must identify qualifying R&D expenditure, calculate the relief amount based on the current credit rates, and complete the additional information form with supporting evidence before submitting it to HMRC.

Who Qualifies for R&D Tax Relief?

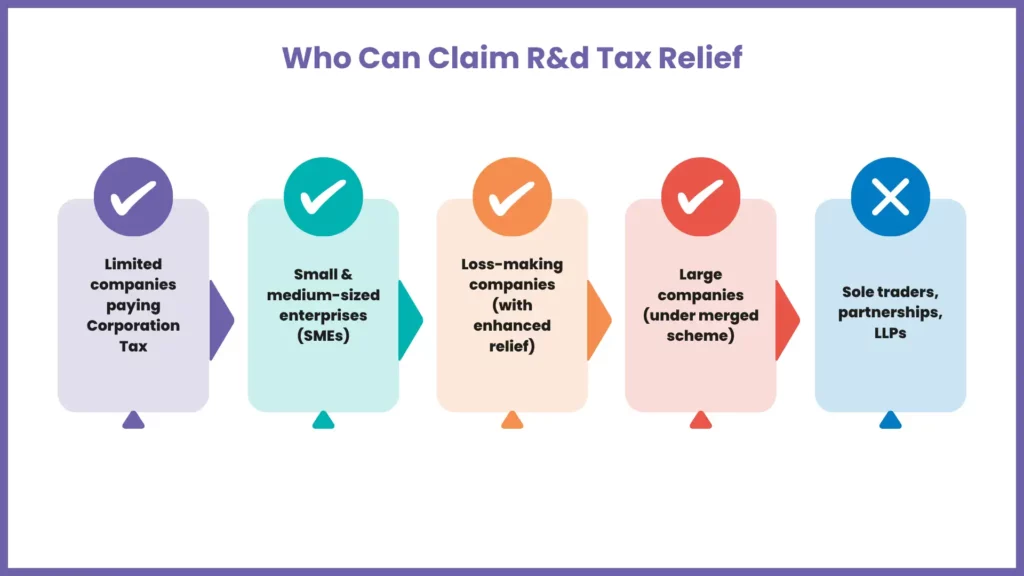

To be eligible for R&D Tax Relief, certain criteria must be met. This is not limited to science labs or engineering firms. Only limited companies that pay Corporation Tax are eligible if they meet HMRC’s conditions. Sole traders, partnerships and LLPs cannot claim R&D Tax Relief directly because they do not pay Corporation Tax.

Eligible Claimants Include

- Limited companies paying corporation tax.

- Small and medium‑sized enterprises with qualifying R&D projects.

- Loss‑making companies that can use enhanced R&D relief rules.

- Large companies under the merged scheme.

- Companies with innovative improvement projects that face technical challenges.

The eligibility test focuses on whether a project involves progress in science or technology and tackles uncertainty that competent professionals cannot easily resolve with standard techniques.

R&D Tax Relief applies to small companies of most sizes that are advancing knowledge or capability. It does not matter if the business is profitable or currently loss‑making as long as you meet the qualifying criteria.

What Counts as R&D for Tax Purposes?

Understanding what constitutes qualifying research and development from HMRC’s perspective is key before you start your claim.

Qualifying R&D Activities

Project with Technical Uncertainty

Work that attempts to overcome problems where the outcome is not readily deducible by a professional in the field. This could be anything from custom software development to novel product design.

Scientific or Technological Advancement

Activities aimed at increasing knowledge, capability, or functionality that are not readily available or easily achieved.

Systematic Investigation

Research must follow a planned approach involving testing, experimentation or iteration rather than routine work.

Examples of Qualifying R&D Projects

• A manufacturing firm redesigning a key component to improve efficiency.

• A software company building new systems to handle large‑scale data in unique ways.

• A biotech start‑up developing a new assay technique under uncertain results.

These are representative examples and not exhaustive. HMRC also accepts projects that attempt partial improvements so long as the technical hurdle is genuine.

What Costs Can You Claim Under R&D Tax Relief?

Not all costs in your business count towards R&D claims. You can include only certain types related directly to the qualifying project.

Qualifying Costs Include

Staff Costs

Wages, PAYE and NIC for employees working directly on R&D projects.

Consumables and Materials

Items used up in the project such as testing materials or prototypes.

Subcontractor Costs

Payments to third parties carrying out qualifying R&D work on your behalf.

Software Costs

Software licences used specifically for R&D activity.

Clinical Trial Volunteers

Payments to volunteers in medical or scientific trials only if they are part of qualifying R&D projects and meet HMRC conditions.

Summary: Claiming correctly means capturing both direct expenditure and a proportion of overheads related to R&D. This will increase the value of your R&D Tax Relief return.

Which R&D Scheme Applies to Your Business in 2026?

2026 sees the continuation of the reformed R&D Tax Relief landscape, which combines previous systems into a more unified framework.

Key Schemes for 2026

Merged RDEC Style Scheme

Applies to all companies for accounting periods beginning on or after 1 April 2024, replacing the older SME and classic RDEC approaches. The merged RDEC credit rate is 20% of qualifying R&D expenditure (taxable above the line credit).

Enhanced R&D Intensive Support (ERIS)

A specific route for loss making SMEs with high levels of R&D expenditure relative to total spend (at least 30% R&D intensity), offering a more generous credit.

Eligible ERIS claimants can:

- As per HMRC, you can deduct an extra 86% of qualifying costs (total 186% deduction including the normal 100% deduction).

- As per gov.uk, you can claim a payable tax credit worth up to 14.5% of the surrender able loss.

The reason these schemes exist is to better focus tax support on genuine research and reward companies that commit significant resources to innovation.

R&D Tax Relief Rates in 2026

Current R&D tax credit rates have changed following reform.

| Claim Type | R&D Tax Credit/Rate | Notes |

| Merged RDEC | 20% of qualifying spend | Taxable above‑the‑line credit for most claims |

| Enhanced Support (ERIS) | Additional 86% deduction + 14.5% payable credit | For loss‑making R&D‑intensive SMEs (≥30% R&D intensity) |

| Payable Credit | Up to 14.5% of surrenderable loss | Effective benefit depends on corporation tax rate and loss position |

These rates ensure that your tax relief aligns with your activities, and that spending on true innovation is recognised appropriately.

Step‑by‑Step: How to Apply for R&D Tax Relief

Applying for R&D tax credits can seem intimidating, but breaking it down into clear steps can make it manageable.

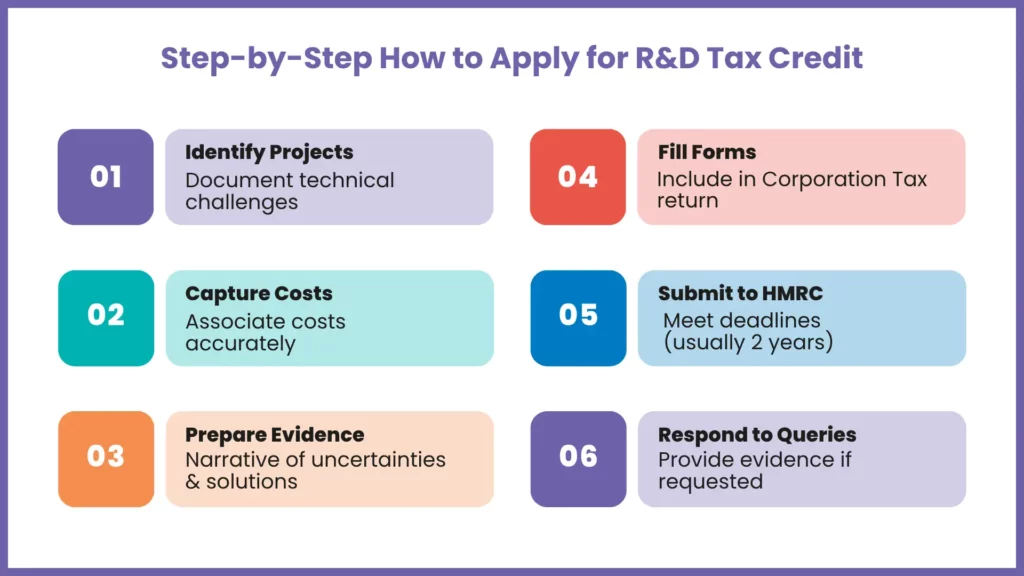

Step 1. Identify Qualifying Projects

List activities that involve scientific or technical challenges and document because they needed problem‑solving.

Step 2. Capture Costs

Associate eligible costs properly in your accounting system so your claim basis is accurate.

Step 3. Prepare Supporting Evidence

Draft a narrative that explains your technical uncertainties, challenges and solutions with dates, staff involvement and results.

Step 4. Fill Out Your Claim Forms

Include R&D figures in your Corporation Tax return with an additional information form for HMRC.

Step 5. Submit to HMRC Before Deadline

Submit your claim along with your company tax return within the statutory deadline: generally, within 2 years of the end of the accounting period for amending returns, the initial claim must be made with the CT return.

Final Step. Respond to Queries

If HMRC has follow‑up questions, be ready with documentation and answers to support your claim.

FAQs: Frequently Asked Questions

What is the deadline for claiming R&D Tax Relief?

You must file your R&D claim with your Corporation Tax return. You can generally amend a return to make a claim within 2 years of the end of the accounting period.

Can you claim R&D Tax Relief for previous years?

Yes. In most cases, you can go back and amend old tax returns to claim R&D Tax Relief for earlier accounting periods. You usually have up to two years from the end of the accounting period to make a backdated claim.

What can trigger an HMRC R&D enquiry?

HMRC may check your claim if your project descriptions are unclear, your costs are not properly supported, or you do not have enough evidence showing the technical challenges you worked on.

What happens during an HMRC R&D compliance check?

HMRC will look at your claim and supporting evidence. They may ask for extra details or explanations about the projects and the costs you included.

What are the penalties for an incorrect R&D Tax Relief claim?

If HMRC thinks your claim is wrong or exaggerated, you could have to pay back the relief along with interest. In some cases, penalties may also apply.

How can you reduce the risk of an HMRC R&D enquiry?

Submit clear, accurate, well‑documented claims with factual narratives and keep records of technical development throughout the year.

Conclusion

R&D Tax Relief in the UK is a great way for businesses to get back some of the money they spend on developing new products, services or processes. It can lower your tax bill and even give you cash if your business is loss‑making. Knowing who can claim, what counts as R&D, and how to make a proper claim can really help your business financially.

Making an R&D claim can be tricky, especially with the rules changing and HMRC checks to consider. Getting help from experts who understand both corporation tax and the R&D claim process in the UK can make it easier to get the full relief you are entitled to and reduce the chance of mistakes. MyIVA’s team are experienced in supporting small businesses, sole traders and individuals with all aspects of tax and relief claims, including R&D support.

Ready to find out what R&D Tax Relief you could claim? Get in touch today for personalised support and make sure your business gets every eligible benefit available.