A P11D is the employer form used to report taxable benefits and expenses (Benefits in Kind) provided to employees and directors during the tax year to HMRC.

Tax season in the UK can often feel like a puzzle where the pieces are constantly changing shape. For business owners and employees alike, one of the most important and often misunderstood pieces is the P11D form. As we navigate the 2026/27 tax cycle, staying on top of your reporting obligations isn’t just about following the rules; it’s about protecting your finances from unnecessary penalties.

At MyIVA, we know that tax jargon can be overwhelming. That’s why we’ve put together this definitive guide to help you master the P11D, understand your deadlines, and ensure you’re filing correctly. Whether you’re a director of a limited company or an employee enjoying a few workplace perks, this guide is for you.

What is a P11D form?

A P11D is a tax document that a UK employer completes to report to HM Revenue and Customs (HMRC) about the ‘perks’ or ‘Benefits in Kind’ (BiK) provided to their employees and directors in the tax year.

But what exactly is a Benefit in Kind? It can be any item that your employer provides you in addition to your regular wages.

The form covers a wide range of benefits, such as:

- Company cars

- Private medical insurance

- Beneficial loans

- Living accommodation

- Assets transferred to employees

- Certain travel and entertainment expenses

HMRC considers these benefits to be income due to their monetary value, which you have received without paying for it yourself but benefited from; HMRC typically wants its cut—tax.

The P11D form acts as the official record of these items. It ensures that the right amount of Income Tax and National Insurance is collected on the total value of your compensation package, not just your base pay.

What does a P11D mean if you’re an employee?

If you receive a P11D from your employer, it doesn’t necessarily mean you owe money immediately.

The form simply informs HMRC about the value of benefits you’ve received during the tax year. HMRC may then:

- Adjust your tax code

- Collect additional tax through PAYE

- Use the information for your Self Assessment tax return (if applicable)

For employees, the P11D acts as a record of non-salary benefits provided by an employer.

P11D vs. P11D(b)—what’s the difference?

One of the most common areas of confusion is the distinction between P11D vs P11D(b).

P11D

- A P11D reports the value of benefits and expenses provided to individual employees or directors.

- A separate P11D is generally completed for each employee receiving reportable benefits.

P11D(b)

- A P11D(b) is a declaration completed by the employer that summarises the total amount of Class 1A National Insurance Contributions (NICs) due on benefits reported.

- While the P11D focuses on employees, the P11D(b) focuses on the employer’s NIC liability.

| P11D | P11D(b) |

| Reports employee benefits | Reports the employer’s Class 1A NIC liability |

| Prepared for individual employees | Prepared once for the employer |

| Shows taxable benefit values | Shows NIC payable on benefits |

| May not be required if all benefits are payrolled | May still be required depending on circumstances |

Understanding the difference between these forms is necessary for accurate reporting and compliance.

P11D form vs P11D value—clearing up the confusion

One common area of confusion is the difference between the “form” and the “value.”

- The P11D Form: This is the actual document (or digital file) submitted to HMRC.

- The P11D Value: This is the “cash equivalent” price tag attached to a benefit.

For example, with company cars, the P11D value generally includes:

- Manufacturer’s list price

- Optional extras

- Delivery charges

- VAT (where applicable)

This value is then used to calculate the employee’s taxable benefit charge.

So, while the names sound similar, they refer to entirely different things.

Who needs to file a P11D (and who doesn’t)

If you are an employer and you’ve provided

- Any non-exempt benefits to your staff or directors,

- Have reimbursed expenses that are not exempt

- If you have not fully paid for the benefits provided,

You generally need to file a P11D. This includes limited company directors, even if they are the only person working in the business.

This applies to:

- Limited companies

- SMEs

- Large organisations

- Charities employing staff

- Directors receiving benefits

You might NOT need to file if

- You have paid all your benefits. This is a system where you calculate the tax on benefits yourself and deduct it from the employee’s pay every month through your payroll software. If you do this and have registered with HMRC in advance, you don’t need individual P11Ds.

- You provided no benefits at all during the year.

- The benefits you provided are exempt (more on that below).

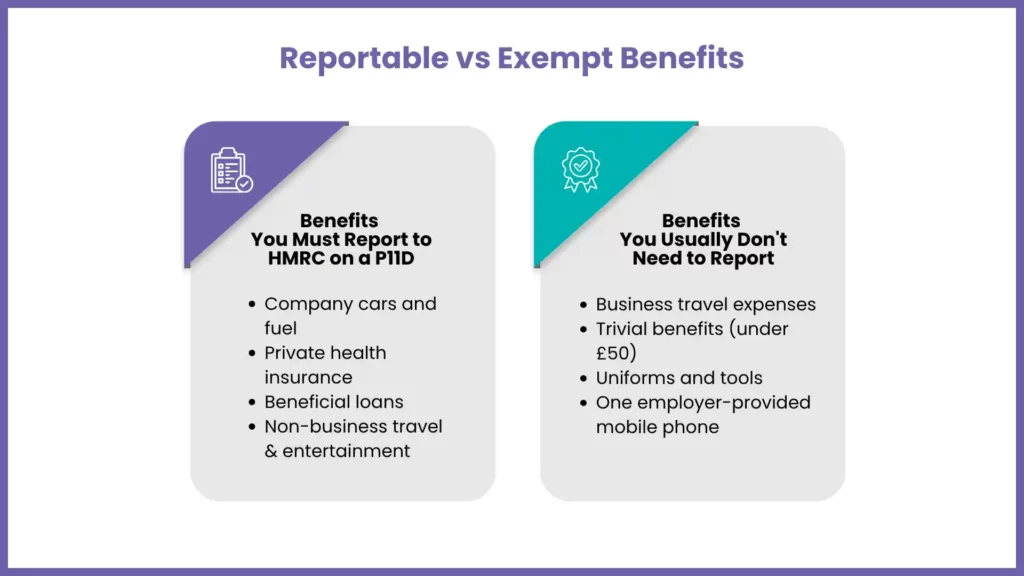

What goes on a P11D? (reportable benefits)

HMRC wants to know about a wide variety of perks. Some of the most common reportable benefits include:

- Company Cars and Fuel: If you have a car provided by work that you also use for personal trips (including commuting), it needs to be reported.

- Private Health Insurance: If the company pays for your medical or dental coverage.

- Beneficial Loans: If your employer gives you a loan at a low interest rate as compared to the market rates.

- Living Accommodation: If the company provides a flat or house for you to live in.

- Assets for Personal Use: If you are given a laptop, phone, or even gym equipment that you use significantly for non-work purposes.

- Non-Business Travel and Entertainment: Any personal travel or meals paid for by the company that don’t qualify as business expenses.

- Professional Memberships: Some memberships are exempt, while others may require reporting.

What is exempt from a P11D?

The good news is that not everything is taxable! HMRC provides P11D exemption for several common business costs to save everyone from extra paperwork.

Common exemptions include:

- Business Travel Expenses: A trip to a client’s office or to conduct business by phone or to get supplies for the office.

- Trivial benefits: These are small items, not exceeding £50 in value. They cannot be cash (or a cash voucher), cannot be under a contract, and cannot be a reward for doing a good job (e.g., a bunch of flowers for a birthday is OK; a £50 bonus for achieving a sales target is not).

- Uniforms and Tools: Clothing or specific types of clothing required for work.

- Professional Fees: Some professional subscriptions/memberships that are required for your job are also excluded.

- Mobile Phones: One employer-provided mobile phone per employee is typically exempt.

- Workplace Parking: Parking spaces provided at or near the workplace are generally exempt.

- Staff Canteens: Certain subsidised workplace meals may qualify for exemption.

- Payrolling benefits: If you have correctly registered benefits for payrolling and processed them through HMRC’s payrolling benefits system, you do not need to report those benefits on a P11D. From 6 April 2026, payrolling of most benefits in kind is mandatory, so most employers will not file P11Ds for those benefits.

What are the P11D and P11D(b) deadlines for 2025/26?

Timing is everything for HMRC. For the 2025-26 tax year (which ends on April 5th, 2026), below are the dates you must remember as P11D deadlines:

- July 6, 2026: This is the “Big One” for the employers providing benefits. By this date, all the P11D and P11D(b) forms must be submitted to HMRC. It is also the deadline for employers to give their employees a copy of their P11D information.

- July 19, 2026: The deadline to pay any Class 1A National Insurance owed if you are paying by cheque or post.

- July 22, 2026: The deadline to pay Class 1A National Insurance electronically. Since most people pay online now, this is the date most businesses aim for.

P11D penalties—what happens if you’re late

HMRC doesn’t take kindly to missed deadlines. If you’re late with your filings, the costs can add up fast.

If your P11D(b) is late, you will face a fine of £100 per 50 employees for each month (or part month) it is late as P11D penalties.

If your P11D or P11D(b) is inaccurate, HMRC may charge a penalty based on:

- your behaviour (careless, deliberate, or concealed)

- The amount of tax or National Insurance lost

Penalties can range from 0–30% of the tax/NIC lost for careless errors, up to 100% for deliberate and concealed errors. There is no fixed ‘£3,000 per P11D’ penalty.

HMRC also charges interest on any late Class 1A National Insurance payments.

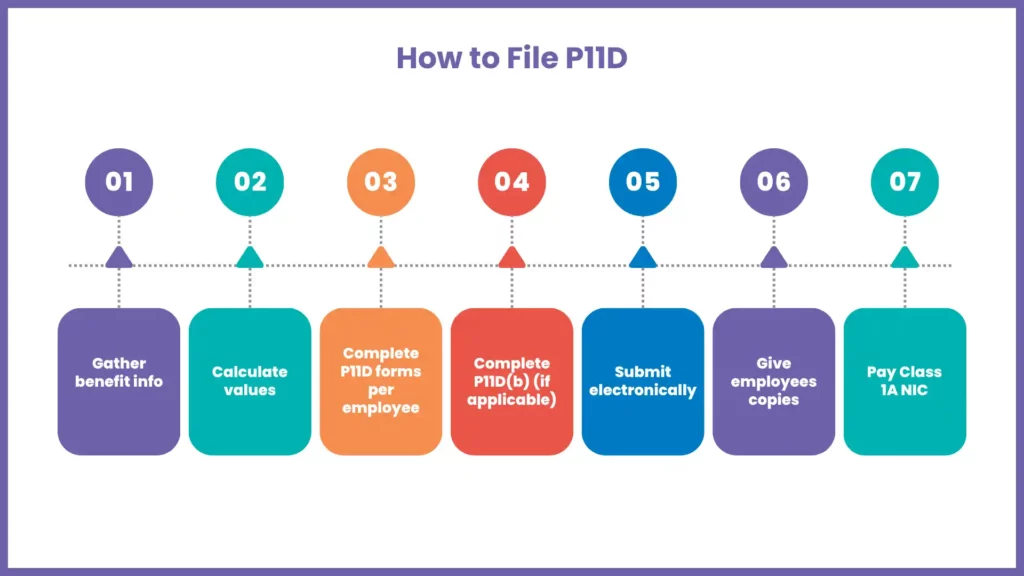

How to file a P11D in the UK?

Throwing out stacks of paper and sending them to an HMRC office is a thing of the past. The introduction of the digital-only filing of P11D from 2023 onwards.

Follow these steps:

Step 1: Gather Benefit Information

Collect details of all taxable benefits and expenses provided during the tax year.

Step 2: Calculate Benefit Values

Determine the taxable value of each benefit according to HMRC rules.

Step 3: Complete P11D Forms

Prepare a separate P11D for each employee receiving reportable benefits.

Step 4: Complete P11D(b)

Calculate the total Class 1A NIC liability and complete the P11D(b).

Step 5: Submit to HMRC

File electronically using compatible payroll or accounting software.

Step 6: Provide Employee Copies

Employees must receive their P11D by the statutory deadline.

Step 7: Pay Class 1A NICs

Ensure payment reaches HMRC before the applicable deadline.

You have three main options for filing:

- HMRC’s Online Service: This is a free online service offered by HMRC, which is ideal for smaller employers with up to 500 employees.

- Payroll Software: Some of the latest payroll software, such as Sage, QuickBooks, or Xero, enable you to file P11Ds straight from your payroll dashboard. This is typically the best method for getting it right.

- Your Accountant or Payroll Service Provider: Many business owners find it easier to let a professional handle the P11Ds to ensure no mistakes are made and all exemptions are claimed correctly. Alternatively, you can use a payroll service like MyIVA to manage P11Ds, benefits in kind, and all your PAYE obligations from one place.

Do I still need a P11D if I have payroll benefits?

If you have paid your benefits – meaning the tax on those benefits was taken from the employee’s salary throughout the year via payroll – you do not need to file individual P11Ds for those benefits.

For the 2025/26 tax year, you still need to file a P11D(b) to report the total Class 1A National Insurance due on benefits.

However, from 2026/27, most benefits must be payrolled, and Class 1A National Insurance will be calculated in real-time through payroll, so the P11D(b) will generally no longer be required for those payrolled benefits. P11D(b) will still be relevant in limited cases where benefits are not fully payrolled.

Unsure What to Report on Your P11D?

Missing a benefit or claiming the wrong exemption can trigger an HMRC penalty. Our team knows exactly what needs reporting and what doesn’t — so you don’t have to guess.

FAQs: Frequently Asked Questions

Do employees get a copy of their P11D?

Yes. Employers are legally required to provide employees with a copy of their P11D information (or a written statement of the benefits) by July 6th each year. This helps employees check their own tax position.

Does a P11D affect my tax code?

Yes, usually. HMRC will use the P11D information to change your tax code for the following year. This allows them to collect the tax you owe on your perks gradually through your salary, rather than asking for a big payment all at once.

Do I include payrolled benefits on my Self Assessment?

Generally, no. If your benefits were payrolled, they should already be included in the “total pay” figure on your P60. However, if you received benefits that were not payrolled and were instead reported via a P11D, you must include those details in the “Benefits in Kind” section of your Self Assessment tax return.

Can I still file a P11D on paper?

No. As of 2023, HMRC has mandated that all P11D and P11D(b) forms must be filed online. Paper forms will be rejected and could lead to you missing the deadline.

What is a P11D(b) nil return?

If HMRC has sent you a “notice to file” a P11D(b), but you didn’t provide any benefits that year and don’t owe any National Insurance, you should submit a “nil return.” This is making sure for HMRC that you’re not forgetting, you just have nothing to report.

Is the P11D being abolished?

From 6 April 2026, payrolling of benefits in kind is mandatory for most non-cash benefits. For 2025/26, it is the last year HMRC will accept P11Ds and P11D(b)s for annual reporting in most cases. From 2026/27, P11Ds will only need to be filed for loans and accommodation benefits.

Conclusion

The P11D form may appear like a piece of red tape, but it is an essential component of the UK tax system. Keeping HMRC happy isn’t a problem, and neither are your employees, as long as you know what a benefit is, maintain good records throughout the year, and are on time with those all-important July deadlines.

At MyIVA, we think clarity is the easiest approach to tax. P11D season doesn’t have to be a headache if you are organised and utilise the digital tools available to you. When in doubt, it’s always good to double-check the official GOV.UK advice or consult a qualified tax expert to make sure you’re making the right move on a particular benefit or exemption.

Need help with your P11D filing? Contact MyIVA today for expert payroll and tax support tailored to your business.