In the UK, some tax obligations can be confusing for many self-employed people, freelancers, and landlords. One of these sources of confusion concerns the Payment on Account (POA) system. Payment on Account is one of the most misunderstood parts of the Self Assessment Tax Return (SATR) that often leads to an unexpected tax bill, which can create pressure on the cash flow.

If you are a new self-employer or an experienced one, any sudden surge in profits can also lead to a surprise tax bill, which seems higher than one might expect. In most of the cases, it is not an error, but it is the result of Payment on Account.

Payments on Account are two advance instalments HMRC asks Self Assessment taxpayers to pay towards next year’s Income Tax and Class 4 National Insurance. Each instalment is half of your previous year’s tax bill and they usually fall due on 31 January and 31 July, which can create a cash-flow “double hit” if income rises.

Imagine a freelance web developer named David. He logged into his HMRC account expecting to pay a £3,000 tax bill. Instead, the total amount due was £4,500. The additional £1,500 was labelled “Payment on Account.” Like many taxpayers, David assumed something had gone wrong.

In reality, HMRC was asking him to pay part of his next year’s tax bill in advance.

In this blog, we will understand how Payment on Account works, who it applies to, and what options are available if you cannot pay it. How it can help you avoid costly surprises and manage your finances more effectively.

Quick summary (TL;DR):

– Payments on Account = two advance payments (50% each) of last year’s Income Tax + Class 4 NI

– Key dates: 31 January (return + balancing + 1st POA) and 31 July (2nd POA)

– Applies if your tax bill is over £1,000 and less than 80% of your tax is paid at source

What Is Payment on Account?

Essentially, a payment on account is an advance payment made towards your upcoming Self Assessment tax bill. HMRC would require you to pay your tax in advance, as it splits up your estimated tax liability into two regular payments instead of waiting until the end of the financial year to pay it once.

The core intent behind this framework is to align your self-employment tax collection more closely with the PAYE (Pay As You Earn) system that was used for employees, where tax is deducted automatically from their pay packets each month.

Both advance instalments are worked out as half of what you paid in last year’s bill (for both your Income Tax and Class 4 National Insurance).

Who Needs to Make Payments on Account?

The advance payment structure does not automatically apply to every single person who completes a Self Assessment return. HMRC applies specific thresholds to determine who enters the cycle. You are legally required to make payments on account unless you meet either of the following two exemptions:

- Your Tax Bill is Under £1,000: If the total tax liability resulting from your latest Self Assessment return—after accounting for any deductions at source—amounts to less than £1,000, you are exempt. You will simply pay that balance as a one-off sum.

- 80% or More of Your Tax Is Already Paid: If the vast majority of your annual tax is already captured at source—such as through an employer’s PAYE scheme, deducted from a company pension, or processed via the Construction Industry Scheme (CIS)—you do not need to make advance payments, provided this captured amount accounts for at least 80% of your overall tax liability.

If you are a sole trader, freelancer, partner in a business, or a residential landlord earning significant untaxed income that pushes your final annual bill past £1,000, you will automatically find yourself enrolled in the payment on account system.

How Are Payments on Account Calculated?

The calculation is relatively simple.

HMRC assumes your income for the coming year will be similar to the income reported on your most recent tax return. Based on this assumption, your Income Tax and Class 4 National Insurance bill are divided into two equal instalments.

For example:

- If your 2024/25 tax year’s tax liability is £3,000

- Your first payment on account for the 2025/26 tax year will be £1,500

- Your second payment on account for the 2025/26 tax year will be £1,500

These advance payments are then offset against your final 2025/26 tax bill when the next return is submitted.

To visualise exactly how this calculation plays out in real terms and impacts your cash flow over multiple years, consider the following structural breakdown:

| Financial Metric | Year 1 (Profits Rise) | Year 2 (Stable Income) |

| Actual Self Assessment Tax Bill | £3,000 | £3,000 |

| First Payment Due (31 January) | £3,000 (Prev. Year) + £1,500 (Advance) = £4,500 | £1,500 (Advance) + £0 (Balancing) = £1,500 |

| Second Payment Due (31 July) | £1,500 (Advance) | £1,500 (Advance) |

| Total Paid Over the Cycle | £6,000 | £3,000 |

Why the First Year Feels So Expensive

Many taxpayers experience a significant shock when they first enter the Payment on Account system.

This is because they must pay:

- The tax bill for the year that has just ended.

- The first 50% advance payment for the following year.

Using the example above:

- Tax due for previous year: £3,000

- First payment on account: £1,500

- Total due on 31 January: £4,500

A second payment of £1,500 is then due on 31 July.

This is often referred to as the “double tax hit,” although you are not actually paying extra tax. You are simply paying part of next year’s liability earlier.

Taxes Not Included in Payments on Account

Certain liabilities are excluded from the advance payment calculation, including:

- Capital Gains Tax

- Student Loan repayments

- Class 2 National Insurance contributions

These amounts are normally settled through the balancing payment after your tax return is submitted.

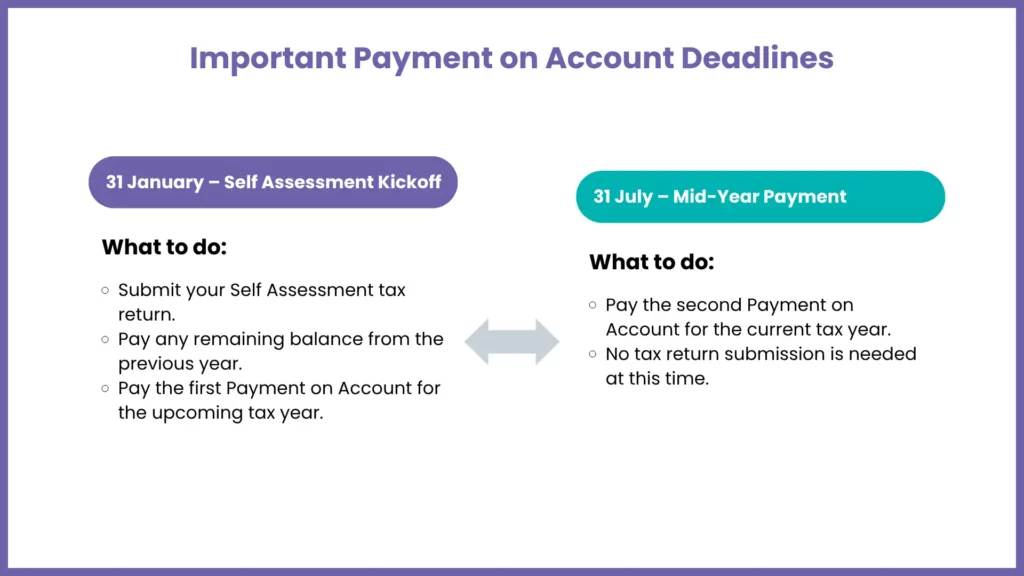

Deadlines and what you must pay by 31 January and 31 July

The Self Assessment system operates around two key dates each year.

31 January deadline

This is the main Self Assessment deadline.

By this date, you must:

- Submit your tax return.

- Pay any balancing payment still owed for the previous year.

- Pay the first Payment on Account for the upcoming tax year.

31 July deadline

The July deadline is simpler.

This mid-year date is dedicated solely to paying your second payment on account for the current tax year. There is no paperwork or tax return submission required in July; it is purely a transaction deadline to clear the remaining 50% advance installment calculated back in January.

In case you miss any of the deadlines, it can lead to additional costs, so it is important to plan ahead.

What Happens If You Cannot Pay by 31 July?

Business income is unpredictable. Your clients can pay you late, you can face seasonal fluctuations, or there can be any unexpected expenses that can make it difficult to meet tax obligations.

If you cannot pay your Payment on Account by 31 July, do not ignore the problem, as HMRC can levy:

Interest Charges

Interest is charged from the day after the payment is due. Interest runs until the debt is fully repaid. HMRC interest rates are tied to the Bank of England base rate, so they can escalate rapidly.

There is generally no immediate fixed penalty for failing to make a Payment on Account in isolation, but interest may be costly if the debt is not paid back. Penalties and late-payment surcharges can apply in broader Self Assessment contexts (e.g. for late returns or balancing payments), so treating POA as “penalty-free” is misleading.

Time to Pay Arrangement

If you are unable to pay the entire amount, then you might be able to negotiate a Time to Pay (TTP) plan with HMRC.

A Time to Pay arrangement lets you pay the tax debt in monthly payments, which can last up to 12 months depending on your situation.

For those whose debt is under the relevant limit, there is an online process for applying through their HMRC account. Others may need to contact HMRC directly.

Although interest continues to accrue, a Time to Pay agreement can prevent further enforcement action and make repayments more manageable.

What to do if you can’t pay (quick checklist):

- Do not ignore HMRC letters – act as soon as you see the deadline.

- Gather your latest figures – income, expenses, and expected cash flow.

- Contact HMRC before the deadline if you know you’ll miss payment.

- Ask for a Time to Pay arrangement if you cannot pay in full.

- Consider a Budget Payment Plan for future liabilities (different from TTP for existing debt).

Can You Reduce Your Payments on Account?

Yes!!

If you believe your income will be significantly lower than the previous year, you can ask HMRC to reduce your Payments on Account.

Common reasons include:

- Losing a major client.

- Reduced trading activity.

- Extended parental leave.

- Retirement.

- A significant drop in rental income.

You can request a reduction online through your HMRC account or by submitting Form SA303.

Be Careful When Reducing Payments

The only time you should reduce Payment on Account is if there is reasonable evidence that your income will actually be reduced.

If you underpay the tax, you may end up paying interest on the underpaid amount after the tax has been calculated on the original payment due dates by HMRC.

Penalties may also be imposed in some instances where the reduction is unreasonable.

For this reason, it is important to base any reduction request on realistic financial forecasts rather than guesswork.

Does Making Tax Digital Change Payments on Account?

Making Tax Digital for Income Tax Self Assessment (MTD ITSA) does not affect the Payment on Account system; it just changes how income is reported.

MTD will involve quarterly updates and digital records by approved software for eligible taxpayers.

However:

- Payment on Account calculations remain the same.

- Payment deadlines remain 31 January and 31 July.

- Tax is still paid through the existing Self Assessment framework.

Important update for 2026:

MTD ITSA eligibility and rollout have changed since 2024. As of 2026, mandatory MTD for Self Assessment applies to many self-employed people and landlords above specific income thresholds. Check the latest HMRC guidance to see if you must use MTD.

The Main Benefit of MTD

While the payment structure remains unchanged, MTD offers improved visibility.

Compatible software provides ongoing estimates of tax liabilities throughout the year. Instead of discovering a large tax bill months later, taxpayers can monitor their expected obligations in real time.

This makes it easier to:

- Budget for tax.

- Identify cash-flow issues early.

- Prepare for upcoming deadlines.

- Decide whether a reduction request may be appropriate.

What Happens If You Overpay?

Sometimes profits fall during the year, meaning your Payments on Account end up being higher than your actual tax liability.

When your next tax return is submitted, HMRC will calculate the final position.

If you have paid too much, you will have a credit balance on your account.

You can either:

- Request a refund directly to your bank account.

- Leave the credit on your account to offset future tax payments.

The process is generally straightforward, provided you do not have other outstanding HMRC debts.

Three Ways to Avoid Future Tax Shocks

Good planning can make Payments on Account much easier to manage.

1. File Your Tax Return Early

You do not need to wait until January to file your return.

Submitting your return shortly after the tax year ends gives you months of advance notice regarding your upcoming liabilities.

Early filing provides greater certainty and allows more time to prepare for both January and July payments.

2. Set Aside Tax Throughout the Year

A common mistake among self-employed individuals is treating all business income as available spending money.

Instead, transfer a percentage of your earnings into a dedicated tax savings account each month.

Many accountants recommend setting aside between 25% and 30% of profits, depending on your circumstances.

This creates a tax reserve and significantly reduces payment-day stress.

3. Use Accounting Software

Cloud accounting software like Xero and QuickBooks can help you monitor income, expenses, and any estimated tax obligations on an ongoing basis.

Real-time reporting helps you better understand the amount of tax you are likely to be liable for and avoids unpleasant surprises at tax time.

How MyIva Can Help with Your Tax Return and Payments on Account

Managing Self Assessment obligations can be challenging, especially when Payments on Account create unexpected cash flow pressures. This is where MyIva can help.

Our experienced tax professionals support self-employed individuals, freelancers, contractors, landlords, and small business owners with every stage of the Self Assessment process. From preparing and submitting accurate tax returns to explaining how Payments on Account are calculated, we help remove the uncertainty surrounding your tax obligations.

With MyIva’s support, you can:

- Prepare and file your Self Assessment tax return accurately and on time.

- Understand exactly how your Payments on Account have been calculated.

- Identify opportunities to legally reduce your tax liability where appropriate.

- If you have seen a drop in your income, then consider whether the amount of Payments on Account is appropriate.

- Get proactive tax planning tips to prevent any unpleasant tax surprises.

- Help with HMRC correspondence and compliance.

- If a payment is due but you are having trouble paying, consider making alternative arrangements by exploring Time to Pay.

MyIva will help you stay ahead of your tax obligations this year instead of waiting to find out in January or July. With clear guidance, support, and practical suggestions on planning, you can ensure that you maintain control of your cash flow and reduce the stresses that can come from that.

Whether you need assistance in completing your first tax return or are in need of the help and support of a tax expert to complete your self-assessment, MyIva can help make it easier, clearer and simpler.

Get Expert Tax Help Today

Take control of your tax planning today! Contact MyIva’s experts to get personalised guidance and avoid unexpected tax bills

Frequently Asked Questions

Why Does HMRC Use Payment on Account?

The system allows HMRC to collect tax closer to the time income is earned, reducing the risk of large unpaid tax balances accumulating.

When did HMRC bring in payment on account?

Payment on Account was introduced as part of the modern Self Assessment system in the 1996/97 tax year.

What Happens If I Miss the 31 July Payment on Account Deadline?

HMRC will charge interest on the unpaid balance from the day after the deadline. Continued non-payment may eventually lead to debt collection action.

Does Making Tax Digital Change Payment Dates?

No. MTD changes reporting requirements but does not alter the 31 January and 31 July payment deadlines.

Can I Pay Monthly Instead?

If you have already missed a deadline, you may need to arrange a Time to Pay agreement instead.

Important distinction:

– Budget Payment Plan = for spreading future estimated liabilities (direct debit)

– Time to Pay = for paying existing debt you already owe

Does Payment on Account Apply to Limited Companies?

No. Payments on Account apply to individuals paying Income Tax through Self Assessment.

Limited companies pay Corporation Tax under separate rules and deadlines.

Conclusion

Payment on Account may seem daunting at first, especially for those starting out in business and self-employed individuals who are growing. But if you realise that it is merely a repayment of your anticipated tax dues, the whole system becomes far easier to handle.

Preparation is the key. There are steps you can take to avoid a tax bill at the end of the year and cash flow problems, such as filing tax returns early, keeping a tax savings account and keeping track of your finances all year.

Making Tax Digital will impact the way tax reporting is done, but the current Payment on Account deadlines will still apply. With knowledge and planning ahead, you can be prepared for taxation without financial strain.

Don’t let unexpected tax bills catch you off guard. Whether you need help filing your Self Assessment tax return, understanding Payment on Account, or managing your tax obligations more effectively, MyIva’s experienced tax specialists are here to help.

Contact MyIVA today for expert guidance and take control of your tax planning with confidence.