Did you know that thousands of small business owners in the UK pay penalties every year simply because they do not understand how Corporation Tax works? Many limited company directors start trading without real clarity on what tax they owe, when it is due, or how to file it correctly.

Corporation Tax is a key responsibility for every UK-registered limited company. When it is handled properly, a small business stays compliant and avoids fines. When mistakes happen, even unintentionally, it can result in penalties, interest charges, and extra pressure that no business owner wants.

This guide explains Corporation Tax in simple terms for beginners. In this blog, you will learn what Corporation Tax is (a tax on company profits), who must pay it, how to register, how to calculate it, key deadlines, current rates (19-25%), penalties, reliefs, and 2025/26 updates. By the end, you will know exactly what your limited company needs to do and how expert support can make the process easier.

What is Corporation Tax?

Corporation Tax is a tax paid by limited companies on their profits. Any limited company registered in the UK must calculate and pay Corporation Tax on the money it earns after allowable expenses.

Corporation Tax applies to profits from trading, investments, and the sale of assets. This includes income earned by a small business through sales, services, rental income, or capital gains. Once the accounting period ends, the company must work out its taxable profit and submit a Corporation Tax Return to HMRC.

Corporation Tax is different from personal tax. It is paid by the company itself, not the director or shareholders personally. Even if you run a small business alone, your limited company is a separate legal entity and must meet its Corporation Tax obligations every year.

Who is Liable to Pay Corporation Tax?

If you operate through a limited company, Corporation Tax is not optional. Understanding who is liable helps avoid mistakes from day one.

Limited Companies Registered in the UK

Any small business set up as a limited company in the UK must pay Corporation Tax on its profits, even if it makes a small amount.

Foreign Companies Trading in the UK

Overseas companies with a permanent presence or trading activity in the UK may also be liable for Corporation Tax on UK profits.

Clubs, Societies, and Associations

Some nonprofit organisations must pay Corporation Tax on surplus income or gains, depending on their structure.

Housing Associations and Co-Operatives

Certain housing bodies are required to submit a Corporation Tax Return if they generate taxable profits.

If your small firm operates as a limited company and makes a profit, Corporation Tax will apply. Knowing this early helps you plan better and stay compliant.

How to Register for Corporation Tax with HMRC?

Registering for Corporation Tax is one of the first responsibilities after forming a limited company. HMRC expects this to be done on time.

Step 1: Incorporate Your Limited Company

Your small business must be registered with Companies House before you can register for Corporation Tax.

Step 2: Start Trading

You must inform HMRC once your company starts trading or receives income.

Step 3: Create a Government Gateway Account

This online account allows your small firm to manage taxes and submissions.

Step 4: Register for Corporation Tax

Log in and register your company for Corporation Tax within three months of starting trading.

Step 5: Provide Company Details

You will need your company number, trading start date, and business address.

Step 6: Set Up Online Services

Activate Corporation Tax services to submit returns and make payments online.

Step 7: Choose Your Accounting Period

This determines the dates used for your Corporation Tax calculation.

Step 8: Keep Confirmation Records

Save HMRC confirmation emails and references for future use.

Registering correctly ensures your small business meets HMRC rules and avoids penalties later.

Corporation Tax Deadlines

Paying Corporation Tax on time is critical. Missing deadlines can cost your small firm money and reputation.

If Corporation Tax is paid late, HMRC may charge interest, penalties, and issue compliance notices. Repeated delays can trigger investigations.

Corporation Tax Deadlines Table

| Task | Deadline |

| Register for Corporation Tax | Within 3 months of trading |

| File Corporation Tax Return | 12 months after accounting period end |

| Pay Corporation Tax | 9 months and 1 day after accounting period end |

Understanding Corporation Tax deadlines helps your small business plan cash flow and avoid last minute stress. Timely filing builds trust with HMRC and keeps operations smooth.

How to Calculate Your Corporation Tax

Calculating Corporation Tax correctly ensures you pay the right amount and not more than necessary.

Step 1: Work Out Total Income

Add all income earned by your small business during the accounting period. This includes sales, service fees, interest received, and any other money coming into the company. Make sure the figures match your invoices and bank records so nothing is missed.

Step 2: Deduct Allowable Expenses

Subtract costs such as rent, wages, software, and marketing. These must be genuine business expenses that were needed to run your small firm. Personal costs should never be included, as this can cause issues with HMRC.

Step 3: Adjust for Capital Allowances

Claim relief on equipment, vehicles, and assets where allowed. Instead of deducting the full cost as an expense, capital allowances spread or reduce the tax impact depending on the item. This step can significantly lower your Corporation Tax if applied correctly.

Step 4: Include Other Income

Add gains from asset sales or investments. This could include selling equipment, property, or shares owned by the company. These gains form part of your taxable profit and must be reported accurately.

Step 5: Apply Corporation Tax Rates

Use the correct Corporation Tax rate based on your profit level. Some small businesses fall into different bands, so it is important to apply the right rate. Using the wrong rate can result in underpayment or overpayment.

Step 6: Check Marginal Relief

Some small firms qualify for reduced rates depending on profits. Marginal relief applies when profits fall between set limits and can lower the effective Corporation Tax rate. Checking this ensures you are not paying more tax than required.

Correct calculation avoids underpayment or overpayment and ensures your Corporation Tax Return is accurate.

How do I Pay my Corporation Tax?

Paying Corporation Tax is done directly to HMRC and should be planned in advance. Choosing the right payment method helps your small business avoid late fees, interest, and unnecessary follow ups from HMRC.

Online Bank Transfer

Transfer funds directly using HMRC bank details and your payment reference. This method is reliable and widely used by small businesses. Payments usually reach HMRC the same or next working day, depending on your bank.

Direct Debit

Set up a direct debit through HMRC for secure payment. This option reduces the risk of forgetting a deadline. It also gives peace of mind as the payment is taken automatically on the agreed date.

Debit or Corporate Credit Card

Pay online through your HMRC account. This is a quick option for small firms that prefer card payments. Be aware that some card providers may charge additional fees.

Faster Payments

Suitable for last minute payments if your bank supports it. Faster Payments can reach HMRC on the same day or the next working day. Always check your bank cut off times to avoid delays.

BACS Transfer

Takes a few days so plan ahead. BACS payments usually take up to three working days to reach HMRC. This method works well if you schedule payments early.

CHAPS Payment

Same day payment for urgent deadlines. CHAPS is often used when a deadline is very close and immediate confirmation is needed. Banks may charge a fee for this service.

Keep Proof of Payment

Always save confirmation for records. This includes bank confirmations, reference numbers, or screenshots. Keeping proof helps resolve any issues quickly if HMRC queries the payment.

Choosing the right payment method ensures your small business avoids delays, penalties, and unnecessary stress.

What are the Current Corporation Tax Rates in the UK?

Corporation Tax rates depend on profit levels and change over time. Knowing the correct rate is essential.

Corporation Tax Rates Table

| Profit Level | Corporation Tax Rate |

| Up to £50,000 | 19% (small profits rate) |

| £50,001 to £250,000 | 25% main rate with Marginal Relief (effective rate tapers from 19-25%) |

| Over £250,000 | 25% (main rate) |

Rates may vary based on associated companies and reliefs. Accurate advice ensures your small firm applies the correct Corporation Tax rate.

Corporation Tax Penalties: What Happens if You’re Late?

Missing Corporation Tax obligations can lead to serious consequences. Even small delays can quickly turn into extra costs and unwanted attention from HMRC.

Late Filing Penalty

A fixed fine is charged if the return is late. This penalty applies even if your small business does not owe any Corporation Tax. The longer the delay, the more likely further action will follow.

Increasing Penalties

Further penalties apply if delays continue. These charges increase after set time periods and can become costly. Repeated late filings also damage your compliance history with HMRC.

Interest on Late Payment

Interest is charged daily until payment is made. This means the amount owed keeps rising the longer it remains unpaid. Even short delays can add unnecessary costs for a small firm.

Estimated Tax Bills

HMRC may estimate what you owe and charge accordingly. These estimates are often higher than the actual amount due. Correcting them later can be time consuming and stressful.

Compliance Checks

Repeated issues may trigger investigations. HMRC may review past returns and request detailed records. This can take up valuable time and disrupt your small business operations.

Staying organised protects your small business from unnecessary financial risk and helps maintain a good relationship with HMRC.

Corporation Tax Reliefs and Allowances You May Be Eligible For

A lot of small businesses pay more Corporation Tax than they need to because they do not know about the reliefs and allowances, they could claim. HMRC lets limited companies lower their taxable profits by claiming certain costs and incentives if they follow the rules. Using these options can cut your Corporation Tax bill and help your small business keep more cash.

Capital allowances are one of the most common reliefs. They let small businesses deduct the cost of equipment, tools, machinery, and some vehicles from their profits. There is also research and development relief, which helps companies working on new products, services, or improvements, even if the project does not work out. Loss relief is another option, allowing you to carry losses forward or sometimes back to reduce Corporation Tax in other years.

Other allowances may apply depending on how your small business operates. These can include relief on charitable donations, relief for certain intellectual property income, and deductions for staff costs and pensions. Claiming reliefs correctly requires good records and accurate calculations, but when done properly, they can make a real difference to the amount of Corporation Tax your small firm pays.

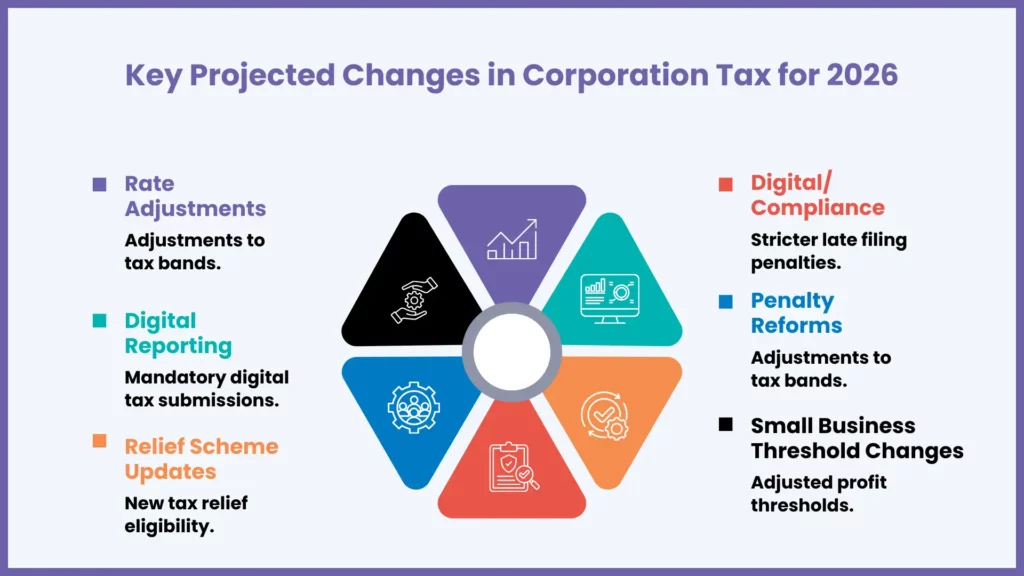

Upcoming Changes to Corporation Tax: What You Need to Know

Corporation Tax rules change regularly and small firms must stay informed. Autumn Budget 2025/26 confirmed rates stable at 19-25% (capped for Parliament term); key 2026 changes:

Rate Adjustments

Future budgets may impact Corporation Tax rates.

Digital Reporting

HMRC continues to push digital submissions.

Relief Scheme Updates

Changes to relief eligibility may affect claims.

Digital/Compliance

MTD for Income Tax starts 2026 (£50k+ threshold)—watch for CT parallels.

Penalty Reforms

Stricter enforcement for late submissions.

Small Business Thresholds

Profit limits may change.

Filing Software Rules

Approved tools may become mandatory.

Director Responsibilities

Greater accountability for filings.

Transparency Rules

Increased data sharing with HMRC.

Staying updated helps your small business avoid surprises and plan ahead.

Don’t miss out on hassle-free tax filing! Get your Corporation Tax filed today

Ensure your limited company stays compliant with accurate Corporation Tax preparation and filing services.

FAQs: Frequently Asked Questions

Do dormant companies pay Corporation Tax?

No, but they must still inform HMRC and file a nil CT600.

Can I pay Corporation Tax monthly?

Most small businesses pay annually, but larger firms may pay in instalments.

Is Corporation Tax paid before dividends?

Yes, dividends are paid from post-tax profits.

Do I need an accountant for Corporation Tax?

Not legally, but expert support reduces errors and saves time.

What happens if I overpay Corporation Tax?

HMRC may issue a refund or credit your account.

Conclusion

Corporation Tax is a key responsibility for every limited company. Understanding how it works helps your small business stay compliant, avoid penalties, and manage cash flow better.

From registration to payment, deadlines, rates, and reliefs, each step matters. Mistakes can be costly, but with the right knowledge, Corporation Tax becomes manageable rather than stressful.

MyIVA supports small businesses, sole traders, and limited company directors with end-to-end Corporation Tax services. From registration and calculation to filing and payment, our expert team makes the process simple and paperless. If you want peace of mind and accurate Corporation Tax support, speak to MyIVA today and let us handle your tax while you focus on growing your small business.