For a lot of micro business owners in the UK, tax season feels like a constant overhang. Juggling between sending out invoices, keeping all your records in order & trying to make sense of HMRC’s rules can be a real challenge. Small business owners can miss a deadline because they’re not 100% sure what counts as taxable income which can quickly leave you facing unexpected fines and plenty of unnecessary hassle. But with a bit of knowledge & the right systems in place, managing UK business tax doesn’t have to be a nightmare. By just getting the basics: what you need to pay, when you need to pay it & how to stay on the right side of the law, you can get a grip on your finances and get your business back on track.

A micro-enterprise in the UK is basically a business with less than ten employees with a turnover less than £1 million and or balance sheet total of £500k or less. These types of businesses make up the vast majority of the UK’s business population – often struggle with tax compliance. However, managing UK business taxes isn’t rocket science & doesn’t have to be complicated.

This guide will take you by the hand through the key bits of UK business tax, from Corporation Tax & VAT right down to PAYE & National Insurance, highlighting deadlines, reliefs and all the common pitfalls to watch out for.

Understanding Basics of UK Business Taxation

Every UK business has a relationship with HM Revenue & Customs (HMRC), the government department that runs business taxes. From registering your business to filing your annual return, HMRC’s systems ensure that income, profits and payroll contributions are reported and paid correctly.

Key deadlines to remember:

• Corporation Tax return (CT600): 12 months after your accounting year end.

• VAT returns: quarterly.

• PAYE and National Insurance: monthly or quarterly if you have employees.

• Self-Assessment: sole traders 31 January each year.

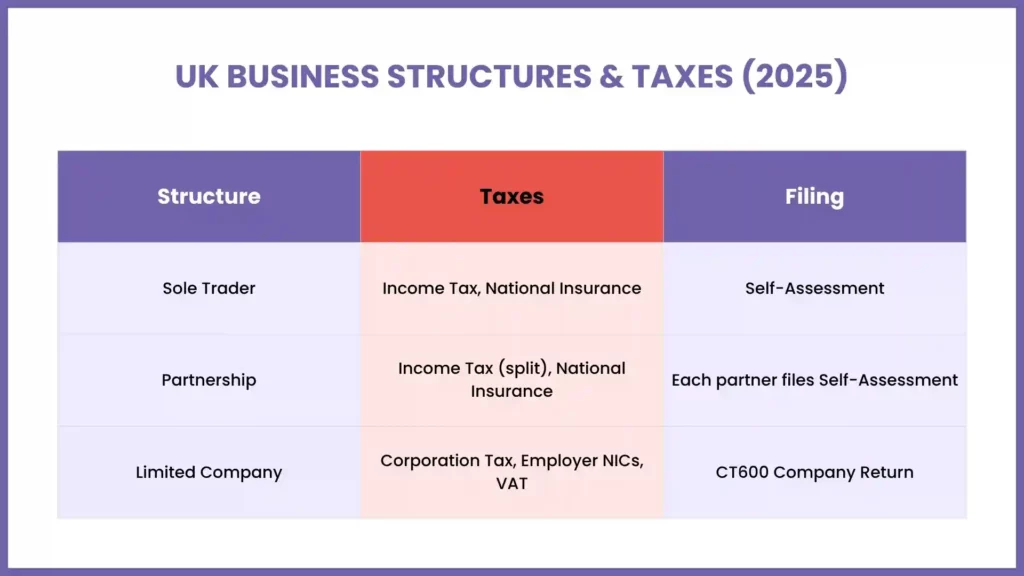

Different business structures face different obligations.

| Structure | Main Taxes | Notes |

| Sole Trader | Income Tax, National Insurance | Profits taxed through Self-Assessment. |

| Partnership | Income Tax, National Insurance | Partners share profits and file individually. |

| Limited Company | Corporation Tax, Employer NICs, VAT | The company itself pays Corporation Tax. |

Tax on Profits: Corporation Tax for Small Enterprises

Limited companies pay Corporation Tax on their trading profits. The main rate in 2025 is 25%, but small businesses with profits below £50,000 qualify for a 19% small-profits rate.

Your taxable profit is what remains after subtracting allowable expenses and capital allowances from total income. If you invest in tools, software, or machinery used for the business, those costs can often reduce your tax bill.

Most small companies use either:

- Cash accounting, where income and expenses are recorded when money changes hands, or

- Accrual accounting, which records transactions when they occur.

Corporation Tax is due nine months and one day after your financial year ends. If your business makes a loss, that loss can be carried forward to offset future profits, which is particularly useful in a business’s early years.

Payroll Taxes: PAYE and National Insurance

If you have employees or directors in your business you’ll need to set up Pay As You Earn (PAYE) — HMRC’s system for collecting Income Tax and National Insurance from wages.

When you pay staff you deduct tax and NICs from their salary and send it to HMRC. As the employer you’ll also pay a separate Employer National Insurance Contribution.

| Type | Who Pays | Rate (2025) |

| Employee NIC (Class 1) | Employee | 10% on earnings above £12,570 |

| Employer NIC (Class 1) | Employer | 13.8% on earnings above £9,100 |

You can register for PAYE online and manage it through payroll software that automatically reports pay details to HMRC. Many small enterprises pay directors a small salary and top up income with dividends to make use of lower tax bands — but it’s best to get professional advice before doing so.

Value Added Tax (VAT) and Your Business

Value Added Tax (VAT) is another big part of UK business tax. It applies to most things you sell in the UK. If your annual taxable turnover is over £90,000 then VAT registration is compulsory. Businesses below the threshold can still register voluntarily to reclaim VAT on their purchases.

Once registered you charge VAT (usually 20%) on sales, that’s called output VAT and reclaim VAT you’ve paid on expenses, that’s called input VAT. The difference is what you pay to HMRC or reclaim back.

For smaller businesses there are simplified options:

- Flat Rate Scheme: pay a fixed percentage of turnover, keep admin simple.

- Cash Accounting Scheme: only pay VAT when your customers pay you.

- Annual Accounting Scheme: one VAT return a year with instalments.

Some sectors like education, finance and healthcare have exemptions or reduced rates so make sure you check how VAT applies to your business.

Key Deductions and Tax Reliefs to Minimize Your Tax Bill

Micro-enterprises can legally reduce UK business tax by claiming every legitimate deduction.

Allowable expenses include:

- Rent, utilities, and office costs

- Software subscriptions, stationery, and equipment

- Business travel and mileage

- Marketing and advertising

- Professional fees such as accounting or legal support

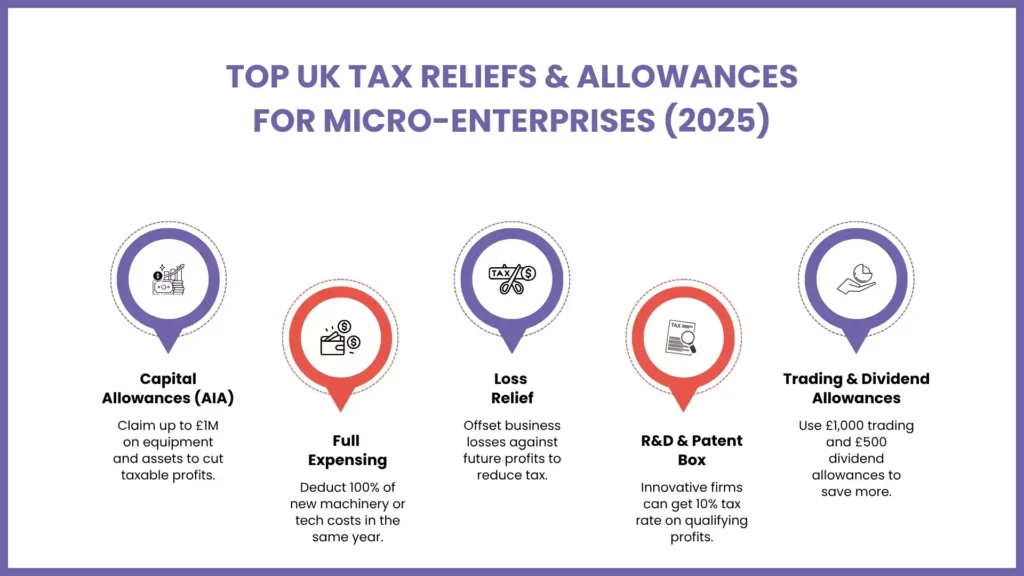

If you buy significant assets like computers or vehicles, you can claim capital allowances. The Annual Investment Allowance (AIA) currently lets you deduct up to £1 million of qualifying purchases from profits.

Other reliefs worth exploring:

- Full expensing: claim 100% of the cost of new equipment in the year you buy it.

- Loss relief: carry trading losses forward to offset against future profits.

- R&D Tax Relief: for businesses developing innovative products or systems.

These reliefs can make a big difference to your bottom line if used correctly.

Special Considerations for Micro-Enterprises: Dividends, Royalties, and Intellectual Property

Dividends

If you own a limited company, you may pay yourself through dividends. The first £500 of dividend income is tax-free. Beyond that, the rates are:

- 8.75% (basic rate)

- 33.75% (higher rate)

- 39.35% (additional rate)

Dividends are paid from post-tax profits, so they don’t reduce your company’s Corporation Tax bill, but they can still be more efficient than taking all income as salary.

Royalties

If your business earns royalties from intellectual property, those payments count as taxable income. At the same time, royalties you pay to others can often be deducted as business expenses.

Intellectual Property

Innovative companies may also qualify for Patent Box Relief, which applies a lower 10% tax rate to profits from patented inventions. If you sell shares or assets, Business Asset Disposal Relief can cut your Capital Gains Tax rate to just 10%, a valuable saving for entrepreneurs planning an exit.

What Happens if You Don’t Pay Taxes on Time?

Late tax payments can incur big penalties and for micro businesses even small fines can break the cash flow.

| Tax | Missed Deadline Consequence |

| Corporation Tax | £100 fine for up to 3 months late, rising with time |

| VAT | Surcharges from 2% of unpaid VAT |

| PAYE | Daily penalties for persistent late filings |

Common mistakes include not registering for tax, poor record keeping and missing filing dates. All of these are avoidable with good systems in place.

Use accounting software to track income and expenses, set calendar reminders for tax deadlines and keep digital copies of all invoices and receipts. Better still partner with a tax specialist who will file and manage everything for you.

Platforms like MyIVA help small business owners stay compliant and give them peace of mind that their tax affairs are in order.

Tax Planning Tips for Micro-Enterprises

Effective tax planning is all about timing, structure, and awareness. Here are a few strategies that work for small firms:

- Plan for cash flow: Set aside around 20–25% of profits for future tax bills.

- Use your allowances: The £1,000 trading allowance and £500 dividend allowance can reduce what you owe.

- Separate finances: Keep personal and business accounts apart for cleaner records.

- Review regularly: Revisit your structure each year, what worked as a sole trader might not work as you grow.

- Get professional input: An accountant can often save more in tax than they cost in fees.

Good accounting habits aren’t just for compliance; they help you understand how your business performs month to month.

FAQs: Frequently Asked Questions

Do I need to register for VAT if I’m under the threshold?

No, unless you choose to register voluntarily, which can be beneficial if you buy a lot of goods or services that include VAT.

What happens if I miss a Corporation Tax filing?

You’ll face a £100 penalty immediately, increasing the longer it’s outstanding.

Can I reclaim VAT on expenses?

Yes, as long as you’re VAT-registered and the expenses relate to business activities.

What are the biggest tax mistakes small firms make?

Missing deadlines, not keeping receipts, and failing to set aside money for taxes.

Which business structure saves the most tax?

It depends. Limited companies can be more efficient once profits grow, while sole traders benefit from simplicity at smaller scales.

Conclusion

UK business tax isn’t just a chore, it’s a skill that helps you make better decisions. For micro businesses every pound count and knowing where it goes (and why) can be the difference between surviving and thriving. If you’re unsure about your obligations or just want to get sorted before the next filing season, MyIVA can help.

From VAT and Corporation Tax to payroll and self-assessment filings, MyIVA works with small UK businesses to simplify compliance and free up your time to focus on growth. When you understand your taxes, you understand your business.