Did you know that many small business owners pay the wrong amount of tax simply because they do not fully understand Corporation Tax rates? Each year, changes in thresholds and rules cause confusion, especially for limited company directors managing tax alongside day-to-day work.

Corporation Tax Rates decide much of your company’s profit goes to HMRC. If the rate is applied incorrectly, it can mean paying too much tax or not enough, both of which can cause problems later. Knowing how these rates work makes it easier for a small business to plan ahead and avoid cash flow issues.

In this blog, we break down UK Corporation Tax Rates for 2026 in a straightforward way. We look at how the rates apply, where changes have been made, how to work out what you owe, and when marginal relief comes into play. You will also see how certain situations can affect your tax and where getting the right support can save time and stress.

Understanding UK Corporation Tax Rates in 2026

UK Corporation Tax Rates in 2026 continue to follow a tiered system based on company profits. This means not all companies pay the same rate. The amount of tax a small business pays depends on total taxable profits, associated companies, and whether reliefs apply. These rates are set by the government and enforced by HMRC, so it is important to apply them correctly.

Main Corporation Tax Rate

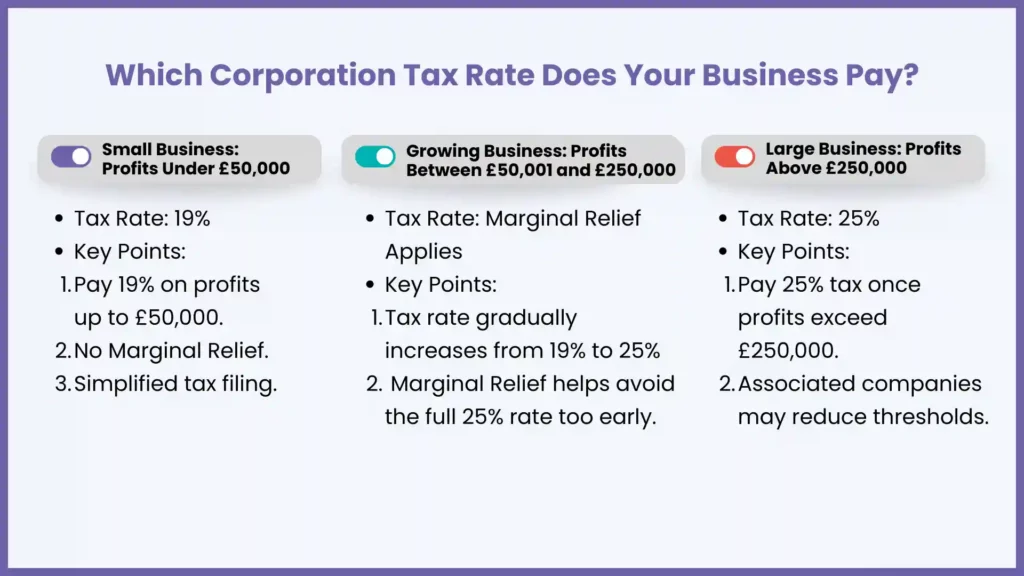

The main Corporation Tax rate applies to companies with higher profits. For 2026, this rate remains at 25 percent for companies with profits above the upper threshold of £250,000. Most medium sized and growing small firms fall into this category once profits increase.

Small Profits Rate

The small profits rate is designed to support smaller companies. Companies with profits at or below the lower threshold of £50,000 pay a reduced Corporation Tax rate of 19 percent. This rate helps early stage and lower profit small businesses manage their tax bills more easily.

Associated Companies and Short Accounting Periods

If a company has associated companies, the profit thresholds are shared between them, divided by (1 + number of associated companies). This can push a small business into a higher Corporation Tax rate sooner than expected. Short accounting periods also reduce thresholds, which can affect how much tax is due.

Special Sectors and Reliefs

Some industries benefit from special rules or reliefs that affect Corporation Tax Rates. These include sectors such as oil and gas, research focused companies, and creative industries. Applying the correct treatment is essential to avoid errors.

Marginal Relief for Middle Bands

Companies with profits between the lower and upper thresholds may qualify for marginal relief. This reduces the effective Corporation Tax rate rather than applying the full 25 percent. Many small businesses fall into this middle band.

Practical Implications for Businesses

Understanding Corporation Tax Rates allows small firms to plan dividends, salaries, and investments properly. It also helps with budgeting and avoiding cash flow problems at tax time. Applying the wrong rate can be costly. Summary of UK Corporation Tax Rates 2026

Summary of UK Corporation Tax Rates 2026

| Profit Level | Corporation Tax Rate |

| Up to £50,000 | 19% |

| £50,001 to £250,000 | Marginal Relief applies |

| Over £250,000 | 25% |

These Corporation Tax Rates apply to most limited companies, subject to specific circumstances.

Key Changes to Corporation Tax in 2026: What You Need to Know

Corporation Tax rules continue to evolve following the Autumn Budget 2025, and 2026 brings changes that small business owners should understand. These updates affect how profits are taxed, reliefs are applied, and capital deductions work.

Rates/thresholds unchanged per Autumn Budget 2025

The 19% small profits rate (£50,000 lower threshold), 25% main rate (£250,000 upper threshold), and marginal relief band remain the same for financial years starting on or after April 1, 2026. No hikes announced.

Main writing-down allowances drop to 14% from April 2026 (Autumn Budget 2025)

This impacts capital allowances calculations (Step 3 in “How to Calculate”), reducing tax relief on plant/machinery purchases for main pool assets. Special rate assets stay at 6%; consider full expensing while available.

Updated Threshold Monitoring

HMRC has increased checks around profit thresholds to ensure correct rates are applied.

Tighter Marginal Relief Reviews

Claims for marginal relief are being reviewed more closely to reduce errors.

Associated Company Rules Clarified

Guidance has been updated to clarify how associated companies share thresholds.

Digital Filing Expectations

HMRC continues to push online filing for Corporation Tax Returns.

Penalty Enforcement Changes

Late payment penalties are applied more consistently across cases.

Relief Claim Evidence

Companies must keep stronger records to support relief claims.

Compliance Focus on Small Firms

HMRC is increasing focus on small firm accuracy and record keeping.

These changes mean it is more important than ever to understand Corporation Tax Rates and apply them correctly.

How to Calculate Corporation Tax

Working out Corporation Tax can feel confusing at first, especially for new company owners. In reality, it follows a simple flow, and once you understand the steps, it becomes much easier to manage and plan for.

Step 1: Calculate Total Income

Start by looking at everything your small business earned during the accounting year. This usually includes sales, fees for services, and any other money that came into the company. Using bank statements and invoices together helps make sure nothing is missed.

Step 2: Deduct Allowable Expenses

Next, take off the costs that were needed to run your small business. This can include rent, wages, software, marketing, and other day to day expenses. Only genuine business costs should be included, as personal spending cannot be claimed.

Step 3: Apply Capital Allowances

Adjust profits for assets such as equipment and vehicles. These allowances reduce taxable profit rather than being treated as normal expenses.

Step 4: Account for Other Gains

Include gains from selling assets or investments. These form part of taxable profit for Corporation Tax purposes.

Step 5: Apply Corporation Tax Rates

Use the correct Corporation Tax Rates based on profit levels and reliefs. This determines the final tax due.

Why Accuracy Matters

Accurate calculation avoids penalties, interest, and HMRC queries. At MyIVA, small business owners receive expert support to ensure Corporation Tax calculations are correct, clear, and stress free.

Marginal Relief: How It Works and Who Can Claim It

Marginal relief is there to help companies that sit between the lower and upper profit limits. If your profits fall into this middle range, you do not suddenly jump from a low rate to the highest one. Many small businesses qualify for marginal relief but do not realise they are entitled to it.

What Is Marginal Relief?

Marginal relief is a way of easing a company into the higher Corporation Tax rate. For companies with profits between £50,000 and £250,000, the tax rate increases bit by bit rather than applying the full main rate straight away. This means the actual amount of Corporation Tax paid is lower than it would be at the top rate.

Who Can Claim Marginal Relief?

Companies may claim marginal relief if they fall within the profit band and are not excluded.

Eligible companies include:

- Limited companies with profits between thresholds

- Small firms without exempt income

- Companies without too many associated companies

Companies must meet HMRC conditions to claim correctly.

How Marginal Relief Is Calculated

- Identify taxable profits

- Confirm profit band eligibility

- Apply HMRC marginal relief formula

- Adjust final Corporation Tax bill

Example

A small business earns £100,000 in taxable profits. Without relief, tax at the main rate would be £100,000 × 25% = £25,000.

Marginal relief is calculated as (£250,000 upper limit – £100,000 profits) × 3/200 fraction = £150,000 × 0.015 = £2,250.

Final Corporation Tax payable: £25,000 – £2,250 = £22,750 (effective rate of 22.75%). This saves £2,250 compared to the full main rate.

Why Marginal Relief Matters

Marginal relief can save small firms thousands of pounds each year. Missing it means paying more tax than required.

Corporation Tax and Special Tax Regimes in the UK

Some limited companies are taxed differently because of the work they do or how they are set up. These special rules can affect the Corporation Tax Rates a small business pays.

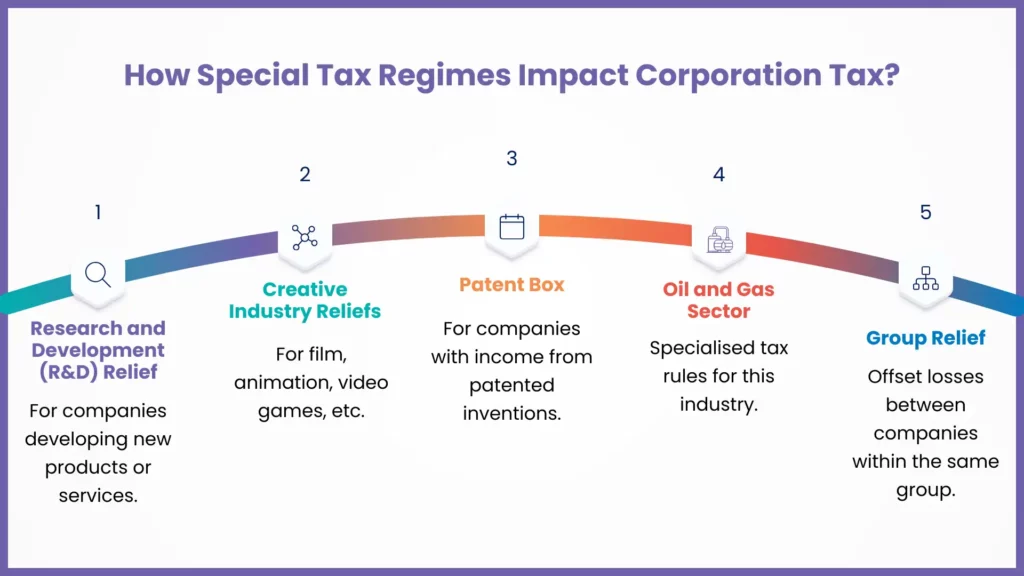

Research and Development Relief

This relief is available to companies that spend money trying to develop new products, services, or processes. The project does not need to succeed to qualify. Claiming this relief can reduce the amount of Corporation Tax a small firm pays and may even result in a refund.

Creative Industry Reliefs

These apply to companies working in film, television, animation, and video games. The reliefs are designed to support creative work carried out in the UK. When claimed correctly, they can lower the effective Corporation Tax Rates on qualifying income.

Patent Box Regime

Companies that earn income from patented inventions may qualify for the Patent Box. This allows profits linked to those patents to be taxed at a lower Corporation Tax rate. Detailed records are needed to support a claim.

Oil and Gas Sector Rules

Companies operating in the oil and gas industry are taxed under separate rules. These may involve higher or adjusted Corporation Tax Rates due to the nature of the sector.

Group Relief

Group relief allows losses from one company to be offset against the profits of another company within the same group. This can reduce the overall Corporation Tax bill for connected small firms.

Understanding these special regimes helps ensure Corporation Tax Rates are applied correctly and that your small business remains compliant with HMRC.

Special Considerations for Non-Resident Companies

Non-resident companies that operate or earn income in the UK still need to consider Corporation Tax rules. Even without a UK registered office, tax obligations can still apply.

UK profits may still be taxable

Income earned from UK activities may be subject to Corporation Tax. This can include trading, services provided in the UK, or income linked to UK assets.

Permanent establishment rules apply

A company may be treated as having a permanent establishment if it has a branch, office, or long-term presence in the UK. Once this applies, Corporation Tax is usually charged on profits linked to that presence.

Withholding taxes may affect income

Certain payments, such as interest or royalties, may have tax deducted before the money is received. This can affect cash flow and must be considered when calculating overall tax.

Double tax treaties can reduce liability

The UK has agreements with many countries to prevent income being taxed twice. These treaties can reduce Corporation Tax, but they must be applied correctly.

Filing requirements differ

Non-resident companies often have different reporting rules compared to UK-based companies. Returns still need to be filed with HMRC in line with these requirements.

Payment deadlines still apply

Corporation Tax payment deadlines are strict, even for non-resident companies. Late payments can result in interest and penalties.

Accurate records are essential

HMRC may request detailed records to support income and expense figures. Keeping clear and accurate records helps avoid delays and disputes.

Non-resident small firms should seek expert advice to ensure they meet UK Corporation Tax obligations and avoid compliance issues.

FAQs: Frequently Asked Questions

What are the UK Corporation Tax Rates for 2026?

For most companies in 2026, Corporation Tax Rates fall somewhere between 19 percent and 25 percent. The rate you pay depends on your company’s profit and whether marginal relief applies.

Do small businesses pay lower Corporation Tax Rates?

In many cases, yes. If profits are on the lower side, a small business may pay a reduced rate rather than the full main rate.

How often do Corporation Tax Rates change?

They do not change every year, but they can be updated after a government budget or new tax rules. It is always worth checking before you file.

Can I reduce my Corporation Tax legally?

Yes, as long as you stay within HMRC rules. Using allowable expenses, reliefs, and proper planning can reduce the amount of tax due.

Do directors pay Corporation Tax personally?

No. Corporation Tax is paid by the limited company itself. Directors and shareholders are taxed separately on salaries or dividends.

Conclusion

Understanding Corporation Tax Rates is essential for every limited company. The rate your company pays depends on how much profit it makes, whether any reliefs apply, and how the company is set up. These details matter, as using the wrong rate can affect how much tax you owe.

For small businesses, getting Corporation Tax Rates right makes it easier to manage cash and avoid problems with HMRC. Errors can be expensive and time consuming, but understanding how the rates work helps reduce that risk.

MyIVA supports small businesses, sole traders, and limited company directors with expert Corporation Tax guidance. From calculations and filings to planning and compliance, MyIVA makes Corporation Tax simple and paperless. Speak to MyIVA today and let our experts handle your tax so you can focus on growing your small business with confidence.