As the clock ticks toward the end of the financial year on April 5th, many UK business owners find themselves in a familiar sprint. Between managing daily operations and balancing the books, tax planning often falls to the bottom of the “to-do” list. However, rushing your filings or overlooking key regulations can lead to significant financial leakage.

HMRC is becoming increasingly sophisticated in its data-matching capabilities. From the rollout of Making Tax Digital (MTD) to more rigorous audits facilitated by AI-driven risk profiling, the margin for error is shrinking. For SMEs, a single oversight can result in hefty penalties, interest charges, or missed opportunities for tax relief claims for small businesses.

In this blog, we explore the most common tax mistakes and UK business tax errors that can drain your profits, and how you can avoid them to ensure a smooth, cost-effective financial year-end.

Introduction

The most complicated obstacle for any entrepreneur is tax compliance. The landscape in the UK is a changing mosaic of Corporation tax, VAT, National Insurance and Capital Allowances. Though compliance is the ultimate goal of most business owners, the abundance of legislation usually causes accidental HMRC tax errors.

The price of tax compliance issues UK businesses face is not simply the flat-rate penalty; the price is the opportunity missed at the cost of reliefs and at the cost of stress of receiving a surprise bill several months after the money isn’t spent anymore. Tax planning at the end of the financial year is the optimisation of cash flows. It guarantees your company some revenue that has been worked hard to invest in the future.

Mixing Personal and Business Finances

Among the most common tax errors SMEs make is when personal and business expenses are mixed. Using the business bank account as a personal piggy bank is a time bomb for business administration.

When you mix finances, bookkeeping becomes a tangled web. Estimating whether a payment was made on office stationery or a personal subscription is a lengthy process that may easily be inaccurate. HMRC can consider personal spending as a kind of hidden pay or illegal dividends, which can give rise to unexpected tax on Income Tax and National Insurance.

The Risk: On top of tax, mixing funds lifts the veil of incorporation of limited companies, and may subject directors to personal liability on company debts.

How to avoid it: Use a very distinct business bank account and a business credit card. When you charge the wrong card, credit the account back and use sticker labels in your accounting program to categorise the payment.

Not Keeping Proper Records

In the age of digital transformation, “the dog ate my receipt” is no longer a valid excuse. Small business accounting tips always start with one word: Documentation.

HMRC requires you to keep records for at least six years. Failure to produce a valid receipt for a claimed expense can result in that deduction being disallowed, instantly increasing your taxable profit and tax bill. Furthermore, under MTD, most businesses must maintain digital records using compatible software for VAT.

The Complexity: A restaurant receipt, for instance, must show if alcohol was purchased, as this affects the deductibility of “subsistence” claims.

How to avoid it: Leverage cloud software like Xero or QuickBooks and integrate apps like Dext. These allow you to photograph and upload receipts instantly, archiving the image safely in the cloud and minimising tax filing mistakes UK businesses make.

Misunderstanding What Counts as an Allowable Expense

Many owners either claim for everything (like a morning latte) or are too scared to claim at all. An expense is generally “allowable” if it is incurred “wholly and exclusively” for the purposes of trade. Common tax deductions for UK businesses include rent, insurance, and marketing, but “dual-purpose” items are tricky.

The Nuance of “Dual Purpose”:

- Home Office: You cannot claim your full mortgage, but you can claim a percentage of utilities based on the square footage used for work.

- Travel: Although commuting to a permanent office is not deductible, commuting to a client site is.

- Clothing: Standard business suits aren’t deductible, but branded uniforms or protective gear are.

How to avoid it: Learn more about it by reading the Business Income Manual by HMRC or have a list of the usual allowable costs. When in doubt, mark the receipt with your accountant to scrutinise it and then file.

Paying Yourself in a Tax-Inefficient Way

As a limited company director, sticking to a high salary triggers higher National Insurance Contributions (NICs). Strategic financial year-end tax planning often involves taking a lower salary (usually up to the Primary Threshold for NICs) and topping up with dividends.

Dividends currently benefit from a lower tax rate than income tax, though the tax-free allowance has been reduced recently. Failing to balance this is one of the most expensive UK business tax errors.

The Strategy: Keeping your salary low also saves the company on Employer NICs, which can be as high as 13.8%.

How to avoid it: Review your extraction strategy every March. Ensure you are utilising your personal allowance (£12,570) and the current dividend allowance effectively to keep your effective tax rate low.

Missing VAT Registration Triggers

If your VAT-taxable turnover exceeds £90,000 in any rolling 12-month period, you MUST register. A common mistake is thinking the threshold is based on the fixed financial year; in reality, it is a rolling look-back performed every month.

If you register late, HMRC will expect the VAT you should have collected from the trigger date, even if you didn’t charge your customers. This can instantly wipe out a small business’s profit margin.

How to avoid it: Monitor cumulative turnover monthly. If you hit £85,000, seek advice on whether to register voluntarily or adjust your pricing for the 20% VAT addition.

Not Planning for Tax Bills Throughout the Year

There is nothing more stressful than reaching the year-end and realising you lack the cash for Corporation Tax. Avoiding tax penalties UK starts with disciplined cash flow.

Because tax is often paid in arrears, it’s easy to spend cash, forgetting a portion belongs to the Crown. The “Payment on Account” trap for Self-Assessment often includes a 50% “down payment” for the next year, which can result in a bill 150% higher than expected.

How to avoid it: Open a separate “Tax Savings” account. Every time a client pays, move 25–30% of that money (covering Tax and NICs) into the account. You’ll ensure the money is ready while earning interest in the meantime.

Ignoring the Director’s Loan Account (DLA)

A DLA records money you put in or take out outside of salary/dividends. If you “overdraw” and fail to pay it back within nine months and one day of the year-end, you trigger a “Section 455” tax at 33.75%.

While repayable once the loan is cleared, the recovery process is slow, hitting your company’s liquidity. If the loan exceeds £10,000, it may also be treated as a “Benefit in Kind,” triggering personal tax issues.

How to avoid it: Monitor your DLA quarterly. Ensure money taken is either categorised as a dividend (if profits allow) or repaid before the deadline to avoid the S455 charge.

Not Claiming Capital Allowances Properly

When purchasing plant and machinery (computers, vans, equipment), you normally claim Capital Allowances and not ordinary expenses. The Annual Investment Allowance (AIA) will allow a 100 per cent deduction of a qualifying asset cost (up to £1 million) on the taxable profits during the year of acquisition.

The Timing Mistake: Buying a laptop on April 6th means waiting a full year for the tax benefit. Buying it on April 4th (before year-end) provides relief in the current period.

How to avoid it: Keep a detailed asset register. Before year-end, review planned equipment purchases. Bringing a purchase forward can significantly reduce your current year’s tax liability.

Filing Returns Late

Late filing remains one of the most common HMRC tax mistakes. Whether it’s Self-Assessment, Corporation Tax, or VAT, penalties for being even one day late are automatic. For Corporation Tax, penalties start at £100 and escalate to 10% of the estimated tax if significantly late. Consistent late filing also flags your business as “high risk” to HMRC.

How to avoid it: Set digital reminders three months in advance. Aim to file at least one month early to account for technical issues. Remember: early filing doesn’t mean early payment—you still have until the due date to pay!

Not Getting Professional Advice Early Enough

Many SMEs only talk to an accountant once a year. By then, it’s often too late for effective financial year-end tax planning. You cannot retroactively change a dividend strategy or claim for an asset you haven’t bought yet.

Expertise is vital for spotting errors and identifying reliefs like Research and Development (R&D) Tax Credits. R&D isn’t just for labs; improving a manufacturing method or developing a software process could qualify you for significant tax back.

How to avoid it: View an accountant as a year-round growth partner. A mid-year tax review often saves you more in tax than the cost of the advice itself.

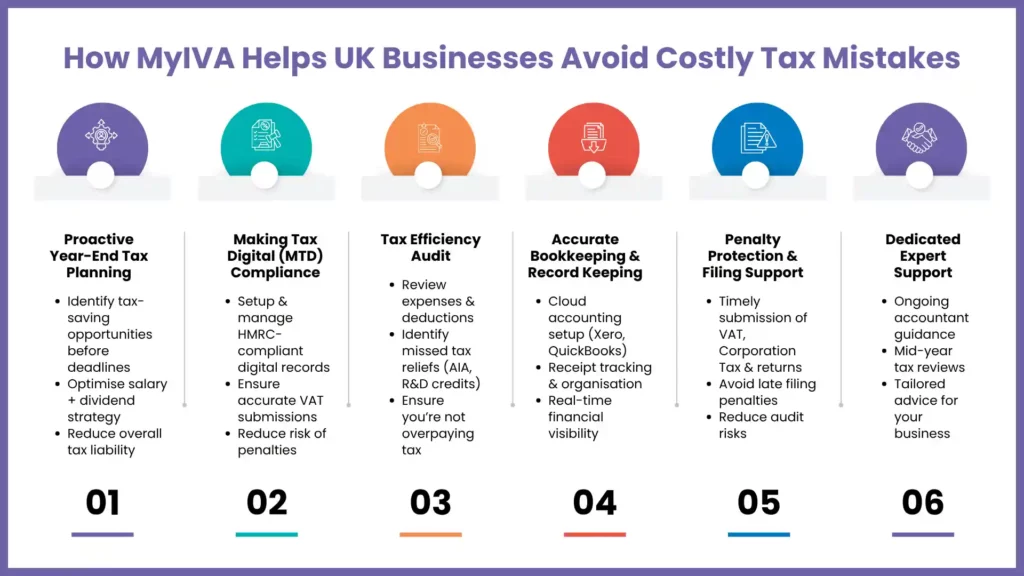

How MyIVA Can Help You Avoid Costly Tax Mistakes

At MyIVA, we understand the demands of running a business. We specialise in helping UK businesses navigate the tax system with clarity and confidence, avoiding any tax mistakes.

Our team provides:

- Proactive Year-End Planning: Strategies for dividends, expenses, and allowances before deadlines pass.

- MTD Compliance: Helping you transition to digital, HMRC-ready record-keeping.

- Tax Efficiency Audits: Ensuring you aren’t overpaying or missing out on R&D or AIA reliefs.

- Penalty Protection: Managing your filings to stay on the right side of HMRC.

Unsure If You’re Making These Mistakes?

Get a quick tax health check with MyIVA, uncover hidden risks, identify missed savings opportunities, and ensure your business stays fully compliant before HMRC does.

FAQs: Frequently Asked Questions

What are the most common tax mistakes for SMEs?

The common tax mistakes for SMEs are failing to keep accurate digital records. Without a clear audit trail, HMRC can disallow deductions, leading to higher bills and “careless” record-keeping fines.

Can I claim for working from home?

Yes. You can claim a proportion of household bills based on room usage or use HMRC’s simplified flat-rate “use of home” allowance.

When is the UK financial year-end?

For individuals, it’s April 5th. For limited companies, it depends on your accounting reference date (usually the anniversary of the month you incorporated).

What happens if I make a mistake on my tax return?

You can usually amend it within 12 months of the deadline. If HMRC finds it first, penalties range from 0% to 100% depending on whether it was careless or deliberate.

Are all business lunches tax-deductible?

No. Entertaining clients or suppliers is not allowable. However, staff entertaining (like a Christmas party) may be deductible up to £150 per head.

Conclusion

The end of the financial year doesn’t have to be stressful. By avoiding these common tax mistakes, you take control of your business’s financial health. Effectiveness isn’t just about following rules; it’s about being proactive. Whether it’s maximising tax deductions for UK businesses or correcting filings before submission, early preparation is the key to profitability.

Take time this month to review your records and consult with professionals. A little planning today saves thousands tomorrow.