More than 5.5 million small businesses are currently active in the UK. Many of these are limited companies that need to deal with Corporation Tax each year. HMRC data shows that late registration and filing errors are common reasons small businesses face penalties and unwanted attention from tax authorities.

For many owners, registering for Corporation Tax can seem confusing at first. New rules, online systems, and strict deadlines can make it difficult to know where to begin. Small business owners often concentrate on sales and growth. Later, they realise that tax registration should have been handled much earlier.

Registering for Corporation Tax means informing HMRC that your small business is active and required to pay tax on profits. You usually need to complete this within three months of starting to trade.

This guide explains how to register for Corporation Tax in 2026, what has changed, when registration is required, and how small businesses can avoid costly mistakes.

What is Corporation Tax?

Corporation Tax is the tax that limited companies and certain other organisations pay on their profits. These profits can come from trading activity, investments, or selling company assets. When you register for Corporation Tax, you inform HMRC that your small business is part of this system.

Corporation Tax is important for how a small firm handles its finances. Once registered, the company must keep accurate records, file Corporation Tax returns, and pay any tax owed by the deadline. Mistakes or delays during registration can lead to penalties, interest charges, or inquiries from HMRC.

If a small business does not register or ignore its responsibilities, HMRC can issue estimated tax bills based on limited information. These estimates are often higher than the actual amount owed. Understanding Corporation Tax early helps small firms manage their cash flow and avoid issues later.

Understanding the Key Changes to Corporation Tax in 2026

For the financial year 2026, the main rate of UK Corporation Tax stays at 25% for companies with profits over £250,000. The small profits rate remains at 19% for companies earning up to £50,000. Marginal relief still applies to profits between £50,000 and £250,000. Although the rates are unchanged, several updates from the Autumn Budget 2025 affect how small businesses figure out reliefs and allowances.

Capital allowances changes

From April 2026, the writing down allowance for plant and machinery in the main pool reduces from 18% to 14%. This slows the pace at which tax relief is claimed on qualifying assets not covered by full expensing. A new 40 % first year allowance applies to certain new plant and machinery purchases made from 1 January 2026. This does not apply to cars, second hand assets, or overseas leasing. The Annual Investment Allowance remains at £1 million, which continues to support small firms investing in equipment.

Investment incentive updates

From 6 April 2026, the Enterprise Management Incentive scheme expands. Gross asset limits increase to £120 million, employee limits rise to 500, and option pools increase to £6 million. Exercise periods also extend to 15 years. The Enterprise Investment Scheme and Venture Capital Trust limits rise sharply, allowing more investment into small firms. However, VCT income tax relief for individuals reduces from 30% to 20%.

Other notable adjustments

Capital gains tax relief for Employee Ownership Trusts reduces to 50% for disposals from late 2025, with gains deferred until trustee disposal. Diverted Profits Tax is phased out from January 2026 and replaced by a 31% charge on certain unassessed transfer pricing profits. Pillar Two rules continue to apply mainly to large groups and bring no major new obligations for most small businesses.

Strategic implications and action steps

Small firms with profits under £50,000 continue to benefit from the lower 19% rate, while larger firms remain at 25 %. The new first year allowance and EMI expansion offer planning opportunities. Small businesses should review asset purchases before April 2026, assess share schemes after April 2026, and keep track of updated investment rules.

When Do You Need to Register for Corporation Tax?

Registering on time is one of the most important tax duties for a small business. HMRC expects companies to register for Corporation Tax soon after they become active, not when profits appear. Missing this step can cause delays, penalties, and filing problems later.

After Incorporating a Limited Company

Once a small business incorporates as a limited company, HMRC must be informed when trading begins. Incorporation alone does not complete the process. You must register for Corporation Tax once the company starts business activity.

When Your Company Starts Trading

A small firm is considered trading when it begins buying, selling, advertising, or offering services. From this point, the clock starts. Most companies must register for Corporation Tax within three months of this date.

If Your Company Has Taxable Income or Profits

Even if profits are low, taxable income still brings about Corporation Tax obligations. Registering makes sure HMRC records are accurate and prevents assumptions about undeclared income.

When Employing Staff or Paying Directors

If a small business pays directors or hires staff, it signals active trading. This is another clear point when you must register for Corporation Tax and align PAYE records.

If Your Company Owns or Rents Property

Rental income or property ownership can create taxable profits. Many small firms forget these counts as trading activity for Corporation Tax purposes.

For Dormant Companies That Become Active

A dormant company that starts trading must notify HMRC. Once active, it must register for Corporation Tax without delay.

If You Are a Non-UK Company Trading in the UK

Overseas companies with UK trading activity may also need to register for Corporation Tax. This depends on the nature of operations and presence in the UK.

Registering early gives clarity, prevents backdated issues, and keeps your small business compliant from day one.

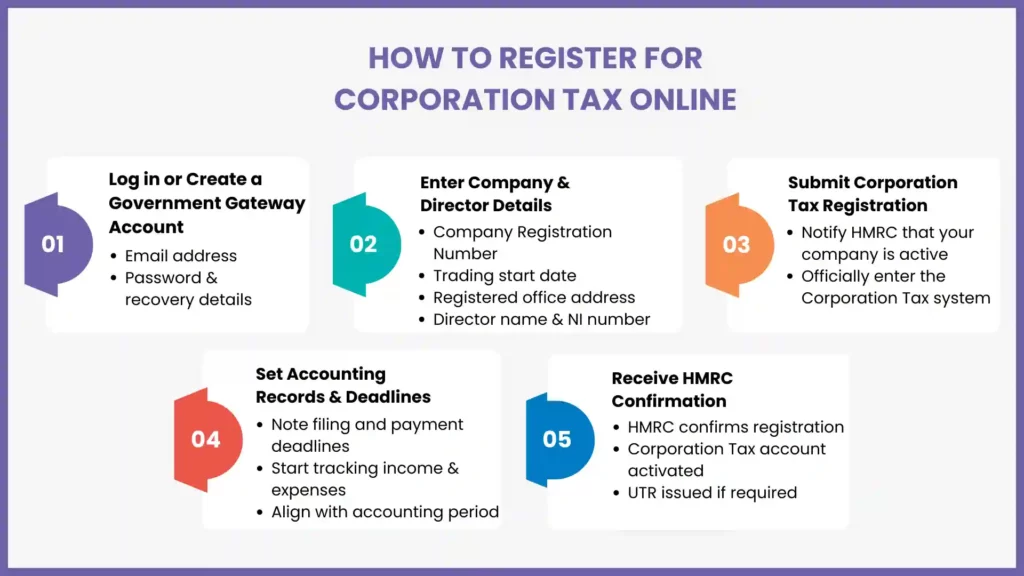

Step-by-Step Guide: How to Register for Corporation Tax Online in 2026

Registering online remains the fastest and simplest option for small businesses. The process is straightforward if details are prepared in advance.

Create or Sign in to Your Government Gateway Account

You will need a Government Gateway account to access HMRC services. Most small firms already have one from incorporation or PAYE setup.

Gather Your Company and Director Details

Have your Company Registration Number, trading start date, registered address, and director information ready. Accurate data speeds up approval.

Register for Corporation Tax with HMRC Online

Log in and complete the Corporation Tax registration form. This officially tells HMRC that your small business is active and liable for tax.

Set Up Corporation Tax Deadlines and Records

Once registered, note filing and payment deadlines. Set up basic accounting records to track income and expenses.

Receive Confirmation and Prepare for Filing

HMRC will confirm registration and issue a Unique Taxpayer Reference if needed. You can now prepare for your first Corporation Tax return.

Completing these steps on time keeps your small business organised and penalty free.

Documents Required for Corporation Tax Registration

Having the right documents ready makes it easier to register for Corporation Tax without delays. HMRC checks these details to confirm your company’s identity and activity.

Company Registration Number

Confirms your company is registered with Companies House.

Certificate of Incorporation

Shows the legal formation date of the company.

Company Unique Taxpayer Reference

Used by HMRC to track Corporation Tax records if already issued.

Registered Office Address

Ensures official correspondence reaches the correct location.

Details of Business Activities

SIC codes explain what your small business does.

Accounting Period Details

Defines the period covered by your Corporation Tax return.

Trading Start Date

Determines deadlines for registration and filing.

Director’s Full Name and Personal Details

Identifies those responsible for tax compliance.

Director’s National Insurance Number

Links personal and company tax records.

Shareholder Details

Required for ownership and profit allocation checks.

Company Contact Details

Allows HMRC to communicate efficiently.

PAYE Reference

Needed if the company employs staff or pays directors.

Government Gateway Login Details

Grants access to HMRC online services.

Details of Associated Companies

Used to assess profit thresholds and reliefs.

Preparing these documents early helps small firms register for Corporation Tax smoothly and avoid repeated requests from HMRC.

What Happens After You Register for Corporation Tax?

After registration, HMRC sets up your Corporation Tax account. You will receive confirmation and any reference numbers needed for future filings. From this point, your small business is officially on HMRC’s Corporation Tax system.

You must then keep accurate financial records. This includes income, expenses, payroll, and asset purchases. These records support your Corporation Tax return and protect your small firm during checks.

Each year, you must file a Corporation Tax return and pay any tax due within the deadline. Even if no tax is owed, filing is still required once registered.

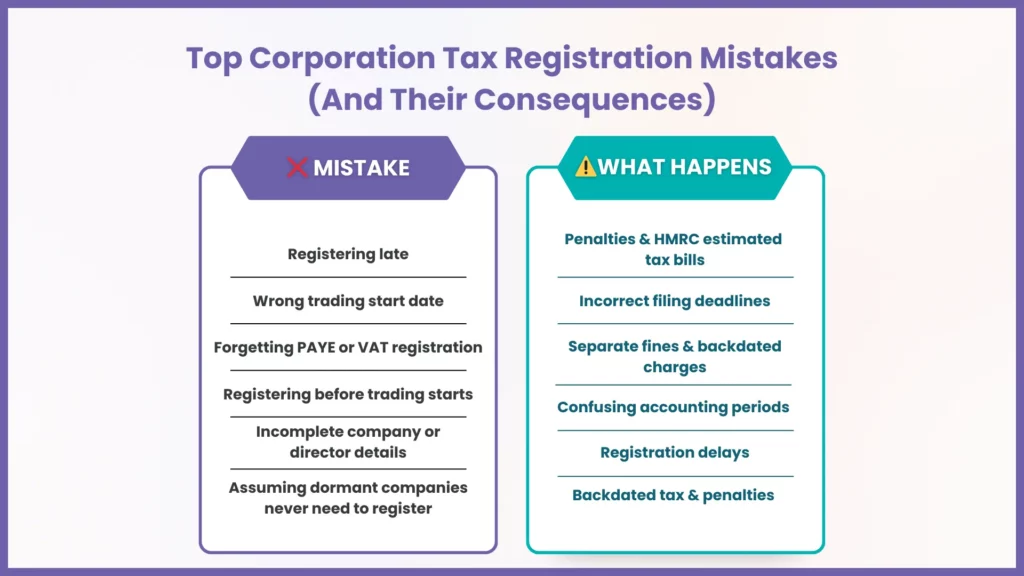

Common Mistakes to Avoid When Registering for Corporation Tax

Many small businesses make avoidable errors when they first Register for Corporation Tax. These mistakes often happen due to lack of guidance or misunderstood HMRC rules.

Missing the Corporation Tax Registration Deadline

Failing to register within three months of trading can lead to penalties and HMRC follow ups.

Registering Before the Company Starts Trading

Registering too early can create confusion around accounting periods and filings.

Entering Incorrect Trading or Accounting Dates

Wrong dates can trigger incorrect deadlines and late filing notices.

Providing Incomplete Director or Company Details

Missing information slows processing and can cause rejection of registration.

Forgetting to Register for PAYE or VAT Separately

Corporation Tax registration does not cover PAYE or VAT. These require separate actions.

Assuming Dormant Companies Do Not Need Registration

Once a dormant company becomes active, registration is required immediately.

Avoiding these errors saves time, money, and stress for small firms.

What If You Miss the 3-Month Deadline for Registration?

If a small business misses the three-month deadline, HMRC may still allow registration, but penalties can apply. The longer the delay, the higher the risk of fines and interest charges.

Late registration often leads HMRC to estimate profits and issue tax demands. These estimates may not accurately reflect the company’s actual situation, leading to disputes and extra work.

Acting quickly minimises the damage. Register as soon as possible, correct records, and seek professional help if penalties are issued. Taking action early shows cooperation and can help limit costs.

Corporation Tax Registration & Support for £325

Get your limited company registered correctly with HMRC and stay fully compliant without stress. MyIVA’s Corporation Tax service is just £399, with expert support from start to finish.

Frequently Asked Questions

Do I need to register for Corporation Tax if my company is dormant?

No, dormant companies do not need to register. Once the company becomes active, you must register for Corporation Tax promptly.

Can I register for Corporation Tax before I start trading?

You should wait until trading begins. Registering too early can cause issues with accounting periods.

How long does it take to get a Corporation Tax reference number?

HMRC usually issues confirmation within a few days. In some cases, it can take up to two weeks.

How do I change my accounting period after registration?

You can update this through your HMRC account or by contacting HMRC directly.

What happens if I stop trading? Do I still need to file a Corporation Tax return?

Yes, you must file until HMRC confirms the company is dormant or closed.

Conclusion

Registering for Corporation Tax is a key responsibility for every small business operating as a limited company. Doing it on time sets the foundation for accurate filings, proper planning, and peace of mind.

The rules for 2026 bring stability in corporation tax rates but introduce changes that affect allowances and incentives. Understanding these early helps small firms make informed decisions and avoid missed reliefs.

MyIVA supports small businesses, sole traders, and individuals by handling Corporation Tax registration, filings, and ongoing compliance. If you want to register for Corporation Tax without stress and get expert support at every stage, speak to MyIVA today and let professionals take care of the numbers while you focus on growth.