In the fast-paced landscape of UK commerce, staying ahead of tax obligations is not just a matter of compliance—it is a cornerstone of fiscal health. Value Added Tax (VAT) is one of the key concerns of business owners as we sail through 2026. As with any VAT-registered body, it is important to know the exact VAT return deadlines to prevent the sting of the points-based penalty system used by the HMRC and to maintain a healthy cash flow.

At MyIVA, we support hundreds of UK businesses through quarterly filings, and we see firsthand how easily the ‘one month and seven days’ VAT deadlines can slip past even with the most organised founders. Tax compliance isn’t just about filing on time; it’s about the administrative discipline required to avoid the new, stricter 2026 penalty points.

Sometimes, navigating the world of VAT may seem like a journey in a regulatory maze. Nevertheless, the main objective is the same: reporting your sales and purchases to HM Revenue and Customs (HMRC) and paying your tax. Being a start-up company that is newly registered or an established limited company, failure to meet your VAT return deadlines can cause unnecessary financial friction.

We at MyIVA know that it is challenging to run a business. Administrative tasks, such as keeping track of your VAT return filing deadline, can always be pushed to the bottom of the priority list until they become urgent. The blog post is designed with simplified 2026 timelines in mind and, in fact, helps you plan your financial calendar with accuracy and certainty.

What Are VAT Return Deadlines in the UK?

A VAT return deadline is the last day by which a business registered under VAT must submit its electronic records to HMRC and ensure that any payment that is due has cleared in the bank account of HMRC. These submissions are to be processed using functionally compatible software since the full implementation of Making Tax Digital (MTD).

The deadline to submit your VAT return will always be virtually the same date as that of the majority of businesses: one calendar month and seven days following the end of your VAT period. As an example, assuming that your VAT quarter runs to March 31st, your due date to submit and also to pay would be May 7th.

One should make a difference between the submission and the payment. Although they both have the same deadline, the payment should really be received by HMRC by the deadline. This means that if you are paying by a method that isn’t instantaneous (like BACS), you must initiate the transfer several days before the deadline for VAT return to ensure you aren’t marked as late.

VAT Return Quarters and Key VAT Deadlines for 2026

HMRC typically assigns businesses to one of three “staggers” for quarterly returns. Your specific quarterly VAT return deadline will depend on which cycle your business falls into.

Stagger 1: Quarters ending March, June, September, December

- Period ending 31st March 2026: Deadline is 7th May 2026

- Period ending 30th June 2026: Deadline is 7th August 2026

- Period ending 30th September 2026: Deadline is 7th November 2026

- Period ending 31st December 2026: Deadline is 7th February 2027

Stagger 2: Quarters ending January, April, July, October

- Period ending 30th April 2026: Deadline is 7th June 2026

- Period ending 31st July 2026: Deadline is 7th September 2026

- Period ending 31st October 2026: Deadline is 7th December 2026

- Period ending 31st January 2027: Deadline is 7th March 2027

Stagger 3: Quarters ending February, May, August, November

- Period ending 28th February 2026: Deadline is 7th April 2026

- Period ending 31st May 2026: Deadline is 7th July 2026

- Period ending 31st August 2026: Deadline is 7th October 2026

- Period ending 30th November 2026: Deadline is 7th January 2027

Better tax planning is possible when you know the exact times of annual VAT returns and use this knowledge to plan tax returns. By knowing these dates, you will be sure that the amount of money you need to cover your VAT liability is set aside and not tied up in operations.

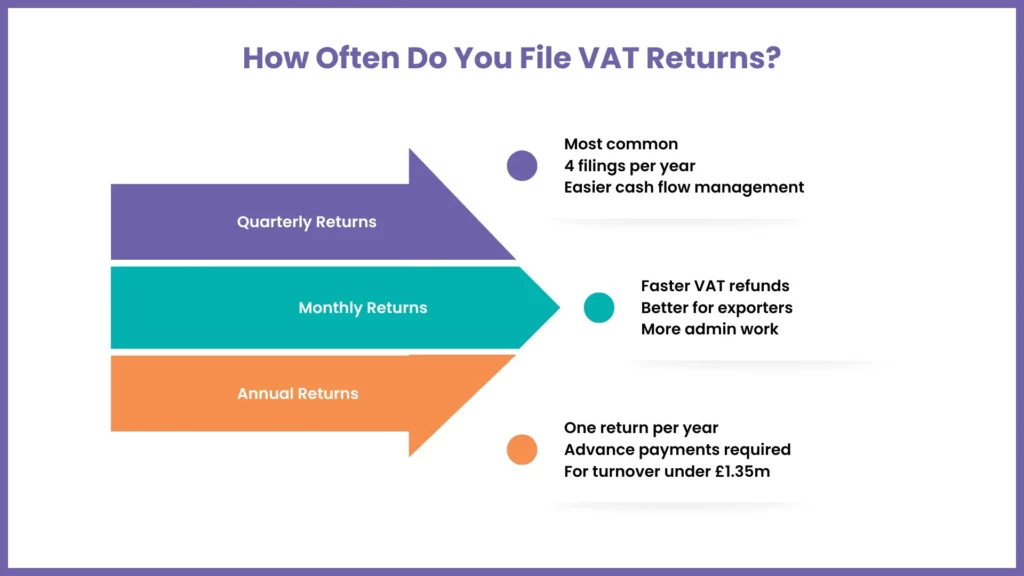

How Often Do Businesses Need to Submit VAT Returns?

The number of times you will deal with HMRC is determined by the VAT scheme you are registered in. Although most people have the quarterly VAT return deadline, other alternatives could be applied to fit various business models.

Quarterly VAT Returns

This is the default for the vast majority of UK businesses. You report to HMRC four times a year. The benefit of this system is that it balances the administrative burden with cash flow management. It prevents a massive year-end tax bill, spreading the liability across four manageable payments throughout the year.

Monthly VAT Returns

Businesses are free to make their monthly returns. Businesses that often receive VAT repayments to HMRC (such as exporters or those dealing with zero-rated goods, such as children’s clothes) often prefer this. These businesses are able to receive their refunds even more quickly, and this will have a tremendous effect on the liquid cash of such businesses. The monthly VAT return deadline is also subject to the same rule of one month and seven days.

Annual VAT Returns

The annual accounting scheme is accessible to companies whose turnover is 1.35 million or less. In this plan, you will only file one VAT return annually. But you will be required to pay in advance on your bill throughout the year (monthly or quarterly). The annual VAT return deadline is two months after your accounting year ends. Although it minimises paperwork, it needs disciplined budgeting that will ensure the final balancing payment is available.

How to Submit a VAT Return to HMRC

In 2026, the only way to submit a VAT return is through Making Tax Digital (MTD) compatible software. The days of logging into the HMRC portal and manually typing in your nine boxes are effectively over for almost everyone.

To submit successfully:

- Keep Digital Records: You must record every sale and purchase digitally.

- Use Compatible Software: Ensure your accounting software (like Xero, QuickBooks, or Sage) is linked to your HMRC digital tax account.

- Review the Figures: Before hitting “submit,” ensure your inputs are accurate. The software will calculate the VAT owed or reclaimable based on your entries.

- Authorise the Submission: Your software will send the data directly to HMRC’s systems, providing you with a confirmation receipt.

Failure to use MTD-compliant software can result in penalties, even if you meet the VAT return filing deadline.

In our experience, clients who integrate MTD-compliant software with a dedicated ‘Tax Pot’ savings account are significantly less likely to face late-payment interest. At MyIVA, we implement a ’10-day pre-deadline’ internal check for our clients; this buffer allows us to resolve any software-to-HMRC communication errors long before the final submission push.

VAT Payment Deadlines and Payment Methods

Meeting your VAT return deadlines is a two-step process: submitting the form and paying the bill. HMRC must receive the funds by the same deadline (the 7th of the second month).

Common payment methods include:

- Direct Debit: This is the most “set and forget” method. HMRC will automatically withdraw the exact amount from your account three working days after the deadline. This guarantees you never miss a payment as long as funds are available.

- Online/Telephone Banking (Faster Payments): Usually reaches HMRC on the same or next day.

- CHAPS: Generally, same-day payment, but it usually carries a bank fee.

- BACS: Takes three working days to process. If using BACS, you must initiate the transfer well before the deadline for VAT return.

Note that you can no longer pay VAT at the post office or via a corporate credit card.

Penalties for Missing VAT Return Deadlines in 2026

HMRC uses a points-based penalty system designed to be fairer to those who make occasional mistakes while penalising persistent offenders.

- Submission Penalties: For every VAT return submission deadline you miss, you receive one penalty point. Once you reach a certain threshold (usually 4 points for quarterly filers), you are hit with a £200 fine. Every subsequent late submission also triggers a £200 fine.

- Payment Penalties: This is where it gets expensive. Late payment penalties are calculated as a percentage of the VAT you owe:

- Up to 15 days late: No penalty if paid in full.

- 16–30 days late: 2% of the VAT owed.

- 31+ days late: 2% of what was owed at day 15 plus 2% of what was owed at day 30.

- Daily Penalties: After 31 days, you also accrue an annual penalty rate of 4%, calculated daily.

Additionally, HMRC charges late payment interest (Base Rate + 2.5%) from the first day the payment is overdue.

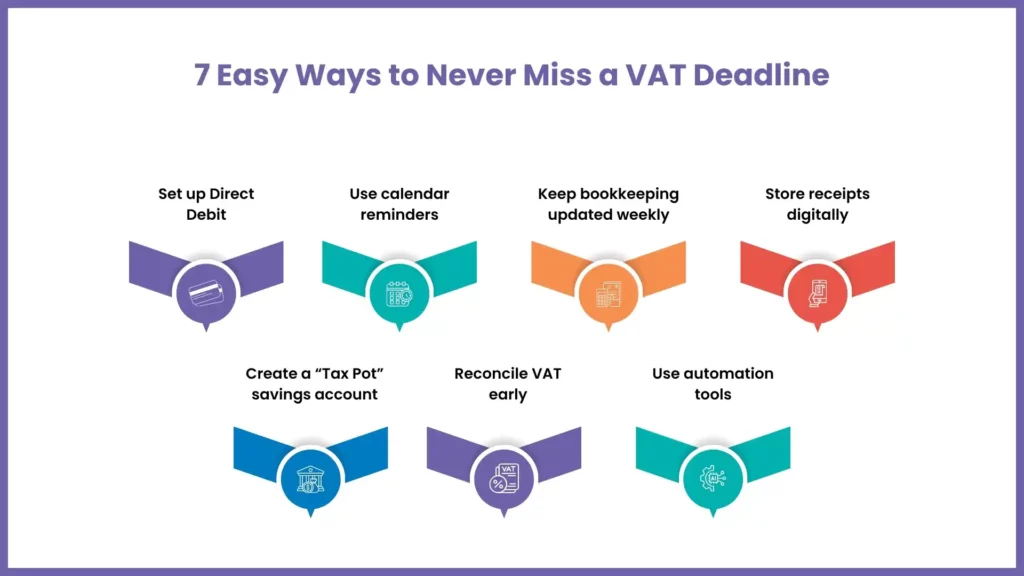

Easy Tips to Never Miss VAT Return Deadlines

Maintaining a spotless record with HMRC doesn’t have to be stressful. Here are some pro-tips:

- Set Up Direct Debit: This is the one most successful method of ensuring that your VAT return filing date never causes you to be fined for paying your taxes.

- Calendar Alerts: Mark your staggers in your digital calendar with reminders one week and two days before the 7th.

- Real-time Bookkeeping: Don’t wait until the end of the quarter to enter your receipts. Take the time to update your software, spending 15 minutes a week updating your software. This reduces the ultimate submission to a five-minute assignment as opposed to the two-day headache.

- Use “Watch” Folders: Many accounting apps allow you to email photos of receipts directly into the system. This ensures you never lose a VAT deduction.

- Monitor Cash Flow: Always keep a separate “tax pot” in your business savings account. Transfer the VAT portion of every invoice you get paid into this pot immediately so the money is ready for the quarterly VAT return deadline.

The most successful businesses we advise don’t scramble on the 6th of the month. They treat VAT as a recurring, automated operation. By setting an internal ‘VAT reconciliation’ date early in the final month of the quarter, you transform a high-stress tax event into a routine administrative procedure.

Common VAT Deadline Mistakes Businesses Make

Even experienced entrepreneurs can stumble. Avoid these common pitfalls:

- The “Bank Holiday” Confusion: In case the last date of filing the VAT return (7th of the month) is a weekend or a bank holiday, then your return and payment have to reach HMRC by the last working day before that date.

- The “NIL” Return Trap: We frequently work with clients who mistakenly assume that if their business had no sales or purchases, they don’t need to file. However, ignoring “NIL” returns is a common trap that triggers automatic penalty points. We always remind our clients: no activity does not means, no filing obligation

- Assuming the “7th” is for Submission Only: Many think they can submit on the 7th and pay later. Both must be completed by the deadline to avoid interest and points.

- Mismatched Accounting Periods: Ensure your internal bookkeeping software dates match the quarters HMRC has assigned to you.

- Not Updating Contact Details: When HMRC sends you a notice about changes in your VAT returns deadlines, and it goes to an outdated email address, then not updating your contact details is not a valid excuse.

Don’t Risk HMRC Penalties—Let MyIVA Handle Your VAT Compliance

Confused by the new 2026 MTD rules or worried about missing your VAT deadline? Stop stressing over spreadsheets and let our experts take over.

FAQs: Frequently Asked Questions

What is the deadline for submitting a VAT return?

The standard VAT return submission deadline is one calendar month and seven days after the end of your VAT period. This applies to both the submission of the return and the payment of any VAT due.

Is VAT due every 3 months?

For most businesses, yes. The deadline for quarterly VAT return occurs four times a year. However, depending on your scheme, you may be required to submit monthly or annually.

What are the VAT quarters in 2026?

VAT quarters depend on your assigned stagger. The most common cycles end in (Jan/Apr/Jul/Oct), (Feb/May/Aug/Nov), or (Mar/Jun/Sep/Dec). You can find your specific dates in your HMRC online account.

Can I change my VAT accounting period?

Yes, you can request a change of your “stagger” through your HMRC online account if, for example, you want your VAT quarters to align with your company’s financial year-end.

What Records Must a Limited Company Keep for Tax Purposes?

A limited company must keep digital records of all sales, purchases, VAT accounts, and self-billing agreements. These must be kept for at least six years. Under MTD, these records must be digital.

What happens if I miss a VAT deadline by one day?

You will likely receive one penalty point. If the payment is also late, interest will start accruing immediately, though the 2% financial penalty usually only kicks in if the payment is more than 15 days late.

Can I pay VAT in instalments?

Standard VAT must be paid in full. But, in case of difficulty, you can call the HMRC to request a “Time to Pay” arrangement. This is supposed to be done prior to the deadline of the VAT return filing.

What Happens if You Submit Incorrect VAT Returns?

If you realise you made a mistake, you can often correct it in your next return if it’s under a certain threshold (£10,000). For larger errors, you must notify HMRC specifically using form VAT652. Intentional errors can lead to heavy “careless” or “deliberate” inaccuracy penalties.

Conclusion

VAT returns management is a part of a successful UK business in 2026. Although the rules might appear to be strict, they are intended to give a stable pattern to the national taxation. You can transform what might be a highly stressful quarterly event into an ordinary administrative procedure by learning about your staggers and by implementing MTD-compliant software and setting up automated payment systems.

If your business is struggling to adapt to the full MTD mandate, our team at MyIVA provides comprehensive MTD-filing support, ensuring your records are always HMRC-compliant and submitted well before the deadline.

The key to staying compliant is preparation. Do not wait until the 6th of the month to check out your accounts. Always be on top of things, update your digital records, and always remember to prioritise the VAT return deadline so as to maintain your business in excellent credit and reputation with HMRC.

Our mission at MyIVA is to assist UK businesses to understand the complications of debt, tax and financial management. Unless you are experiencing any problem with VAT arrears or you are feeling that your tax liabilities are getting out of control, contact our team of professionals today. We provide the guidance and solutions needed to get your business back on a path of sustainable growth.

For more information about UK tax deadlines, you can read our other article on all tax deadlines in UK for 2026.