Every year, millions of small businesses and self-employed people send their tax returns to HM Revenue & Customs. Yet many still end up paying more tax than they need to, often because they leave planning too late. Corporation tax, income tax, VAT, and National Insurance can take a large share of your profit if you do not plan properly. Without clear Tax Planning Strategies, it is easy to face higher bills and pressure on cash flow.

Tax Planning Strategies simply mean arranging your finances in a legal way so you do not pay more tax than required. When done properly, they help you keep more of what you earn and avoid surprise tax bills later on.

In this blog, we explain practical Tax Planning Strategies that can help small businesses, sole traders, and Self Assessment filers reduce their tax legally. We also cover common mistakes, planning tips for growing businesses, and when it may be worth getting professional support.

What Is Tax Planning in the UK?

Tax planning in the UK refers to organising your financial affairs in a legal and structured way to reduce the amount of tax you pay. It involves using available allowances, reliefs, and approved structures to ensure you are not overpaying tax. Good Tax Planning Strategies focus on compliance while improving efficiency.

It includes decisions such as choosing the right business structure, claiming allowable expenses, managing director salary and dividends, and planning pension contributions. It also covers forecasting future tax liabilities so that you are prepared for payments to HM Revenue & Customs.

Importantly, tax planning is not tax avoidance. It does not involve hiding income or breaking rules. Effective Tax Planning Strategies operate within legislation and ensure accurate reporting while reducing unnecessary tax exposure.

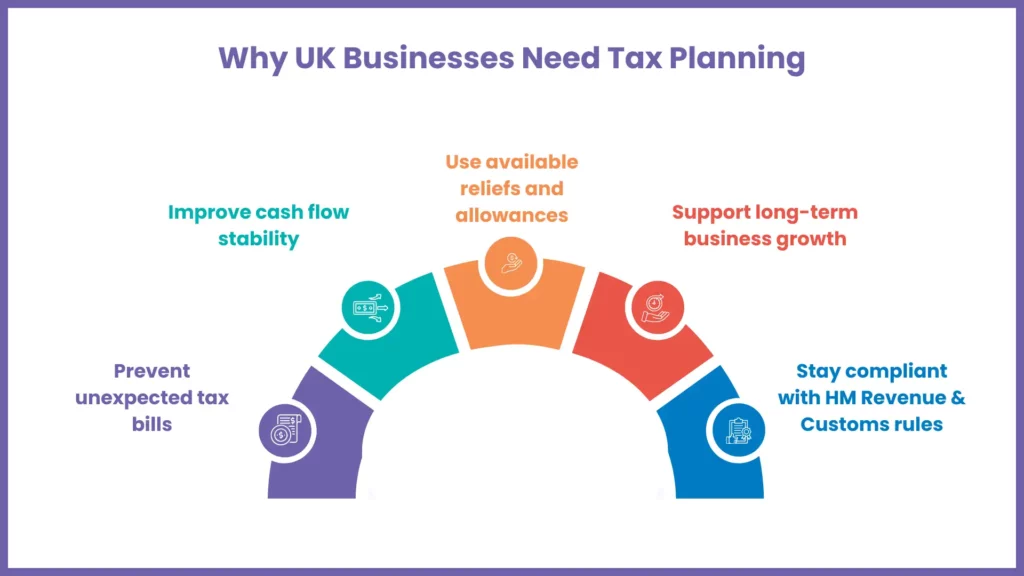

Why Effective Tax Planning Is Crucial for Business Owners

Effective tax planning is not only about paying less tax. It is about knowing where you stand financially and avoiding surprises. Without clear Tax Planning Strategies, many business owners face unexpected tax bills, cash flow problems, or miss out on reliefs they were entitled to claim. Planning ahead helps you stay compliant and keeps your finances more stable.

When you plan properly, you can see upcoming liabilities such as corporation tax, VAT, and payments on account well in advance. This gives you time to set money aside and avoid last minute pressure. It also helps you decide the right time to invest in equipment or make larger business purchases, so you can make full use of available allowances.

Most importantly, effective Tax Planning Strategies support long term growth. When your tax position is structured correctly, you retain more profit within the business, improve stability, and create a stronger base for expansion.

Core Tax Planning Strategies to Reduce Tax for UK Businesses

There are several core Tax Planning Strategies that every small business and sole trader should consider. These are practical steps that can significantly reduce tax liability when applied correctly and reviewed regularly.

Choosing the Right Business Structure

Your legal structure affects how much tax you pay. Operating as a sole trader means paying income tax and National Insurance on profits, while a limited company pays corporation tax and allows profit extraction through dividends. Reviewing your structure regularly is one of the most effective Tax Planning Strategies.

Optimising Director Salary and Dividend Strategy

For limited company directors, balancing salary and dividends is key. A lower salary within National Insurance thresholds combined with dividend payments can reduce overall tax liability. Structured income planning forms an important part of Tax Planning Strategies for company owners.

Capital Allowances and Asset Planning

Businesses can claim capital allowances on equipment, machinery, and certain business assets. The Annual Investment Allowance allows many purchases to be deducted from taxable profit. Planning asset purchases before year end can reduce corporation tax legally.

Pension Contributions as a Tax Planning Tool

Employer pension contributions are usually deductible expenses for limited companies. They reduce corporation tax while building long term personal wealth. Pension planning remains one of the most overlooked Tax Planning Strategies for directors and high earning sole traders.

R&D Tax Relief and Innovation Incentives

Businesses investing in product development or process improvement may qualify for R&D tax relief. This can reduce corporation tax or generate payable credits. For eligible companies, this is one of the most valuable Tax Planning Strategies available.

VAT Planning Strategies for Businesses

Selecting the right VAT scheme can improve cash flow and reduce administrative burden. Options such as the Flat Rate Scheme may benefit some businesses. Monitoring turnover to avoid late VAT registration penalties is also essential.

In short, core Tax Planning Strategies focus on structure, income planning, expense claims, and available reliefs. When reviewed regularly, they reduce unnecessary tax and support stability.

Advanced Tax Planning Strategies for Growing Businesses

As businesses grow, their tax position becomes more complex. Advanced Tax Planning Strategies can further reduce liability and improve long term financial outcomes.

Group Structures and Profit Extraction Planning

For expanding businesses, forming a group structure with a holding company can improve profit extraction planning and asset protection. Dividends between group companies are often tax efficient, creating flexibility.

Loss Relief and Carry Forward Planning

If your business makes a loss, it may be possible to offset it against previous or future profits. Planning how and when to use losses can reduce overall tax liability significantly.

Property Tax Planning for Business Owners

Business owners investing in property must consider income tax, corporation tax, and capital gains tax implications. Proper structuring ensures rental income and disposal gains are treated efficiently.

Advanced Tax Planning Strategies require careful review and accurate records. Done correctly, they protect profit and reduce risk.

Common Tax Planning Mistakes That Increase Tax Bills

Even profitable businesses often overpay tax due to avoidable errors and poor timing. Small decisions made without proper planning can quietly increase your tax bill year after year.

- Leaving tax planning until year-end limits options. Tax Planning Strategies should begin early and be reviewed regularly.

- Mixing personal and business finances leads to missed deductions and compliance risk.

- Failing to claim allowable expenses such as home office costs, mileage, software, and capital allowances increases taxable profit.

- Choosing the wrong business structure can result in higher tax and National Insurance.

- Ignoring payments on account creates cash flow strain in January and July.

- Poor record keeping increases the risk of inaccurate returns and penalties.

- Incorrect VAT planning or late registration can lead to large liabilities.

- Structured Tax Planning Strategies prevent these common and costly mistakes.

When Should You Start Tax Planning?

Tax planning should begin at the start of your financial year, not just before deadlines. Early Tax Planning Strategies give you time to adjust income, control expenses, and make use of allowances.

Quarterly reviews help track profits, monitor VAT thresholds, and prepare for payments on account. This approach improves cash flow and reduces stress.The earlier you apply Tax Planning Strategies, the more control you have over your financial decisions.

Should You Consult a Professional Tax Advisor?

If your income is going up or you are thinking about changing your business structure, it may be the right time to speak to a tax advisor. UK tax rules can be confusing, and small errors can lead to penalties or missed savings. A good advisor looks at your overall situation, including your income, expenses, and future plans, and helps you organise everything in a tax efficient way. For many limited company directors and sole traders, the money saved through proper Tax Planning Strategies is often more than the cost of getting professional advice.

Advantages of Consulting a Professional Tax Advisor:

- Clear guidance on the most tax efficient business structure for your income level

- Identification of all allowable expenses and reliefs that may otherwise be missed

- Proper salary and dividend planning to reduce overall tax liability

- Advance planning for corporation tax, VAT, and payments on account to improve cash flow

- Ongoing support to keep your Tax Planning Strategies aligned with changing rules and business growth

How a Tax Specialist Can Help Reduce Your Business Tax

Managing tax is not just about filing returns. It involves applying the right Tax Planning Strategies throughout the year.

1. Choosing the Most Tax Efficient Structure

A specialist reviews whether sole trader or limited company status suits your income and growth plans.

2. Identifying All Allowable Expenses

Accurate expense claims reduce taxable profit and prevent under claiming.

3. Strategic Income and Dividend Planning

Proper salary and dividend structuring lowers combined tax liability.

4. Making Full Use of Reliefs and Allowances

From Annual Investment Allowance to pension contributions, a specialist ensures nothing is missed.

5. Managing VAT and Cash Flow

Selecting the right VAT scheme improves planning and avoids penalties.

6. Year-Round Planning

Regular reviews ensure Tax Planning Strategies remain aligned with profit levels and goals.

Professional support turns tax management into a structured financial process.

Ready for Proven Tax Planning? Get Expert Help for Just £125

Secure your £125 MyIVA consultation today. We’ll customise tax strategies for your UK business or Self Assessment, slashing corporation tax, optimising dividends, and improving cash flow legally.

FAQs: Frequently Asked Questions

Is tax planning legal in the UK?

Yes, tax planning is completely legal when done properly. It simply means using the allowances, reliefs, and rules set by HMRC to reduce your tax bill in a compliant way.

When should I review my tax strategy?

It is best to review your tax strategy at the start of the financial year. Checking it again every few months helps you stay on track and avoid surprises later.

Do sole traders need tax planning?

Yes, sole traders can benefit a lot from tax planning. Claiming expenses correctly and planning income properly can reduce stress and prevent overpaying tax.

Can tax planning reduce payments on account?

With proper forecasting, you can sometimes reduce your payments on account if your income is expected to fall. It is important to base this on realistic figures to avoid penalties later.

Is professional advice worth the cost?

In many cases, the tax savings gained from good planning are higher than the accountant’s fee. Professional advice also gives peace of mind and reduces the risk of costly mistakes.

Conclusion

Reducing business tax is not about shortcuts. It is about applying clear and structured Tax Planning Strategies that work within UK law. Planning ahead, keeping proper records, and making informed choices help you keep more of your profit and avoid unnecessary risk.

Many small businesses, sole traders, and Self Assessment filers miss out on tax savings simply because they do not review their position during the year. With regular checks and the right guidance, tax bills can be managed in a clear and controlled way.

MyIVA supports small firms, sole traders, and individuals with practical Tax Planning Services tailored to their needs. If you want to reduce your business tax legally and gain clarity over your finances, speak to MyIVA today and take the first step towards a more tax efficient future.