Corporation Tax is one of the largest expenses for small businesses in the UK. HMRC collects billions of pounds each year from this tax, and many small business owners pay more than necessary because they are not clear on what they can claim or how to plan ahead.

For many directors, Reducing Corporation Tax feels confusing and time-consuming. There are rules, deadlines, and tax reliefs, but most small business owners are focused on day-to-day work rather than tax planning. Small mistakes or missed claims can quietly increase the tax bill without anyone noticing.

In this blog, we explain how to reduce corporation tax using clear and practical steps that small businesses can put into action straight away. You will understand how Corporation Tax works, what affects the amount you pay, and ten proven ways to lower your tax legally while staying fully compliant with HMRC.

How Much Is Corporation Tax in the UK?

Corporation Tax is paid by limited companies and certain organisations on their profits. Simply put, it is the tax a small business pays on the money left after all allowable business expenses have been deducted. Knowing the rate is the first step in understanding how to reduce corporation tax effectively.

At present, the main rate of Corporation Tax is 25% for companies with profits above £250,000. For small businesses with profits under £50,000, a lower rate of 19% applies. If profits fall between £50,000 and £250,000, marginal relief may reduce the overall tax rate. This structure means careful planning can make a real difference to how much tax a small business pays.

Corporation Tax is calculated on profits after expenses, allowances, and reliefs. This is why understanding what can be claimed is so important. Many small businesses overpay because they do not use all available reliefs. Learning how to reduce corporation tax helps protect cash flow and supports long term growth.

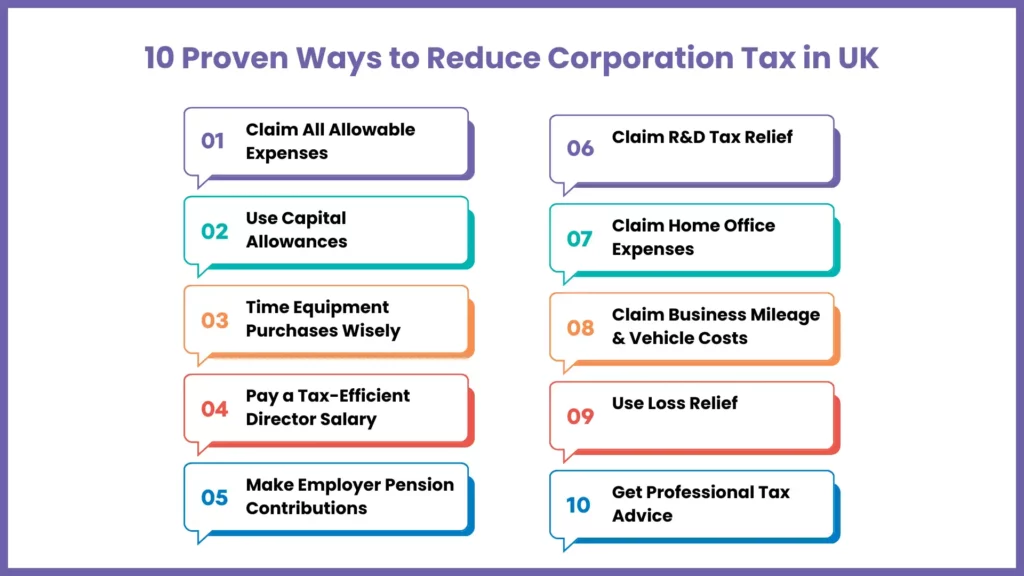

10 Proven Strategies to Reduce Corporation Tax for Small Businesses

There are many legal methods approved by HMRC to lower Corporation Tax. The key is to plan ahead and keep accurate records. Here are ten practical strategies that work well for small businesses and directors who want clarity and peace of mind.

Claim all allowable business expenses.

One of the simplest ways to reduce corporation tax is to claim all allowable business expenses. Everyday small business costs such as office supplies, software subscriptions, phone bills, professional fees, marketing spend, and insurance can all be used to reduce taxable profit.

As long as an expense is used only for small business purposes, it is normally allowable. Keeping receipts organised and uploading them regularly makes it much easier to claim everything you are entitled to. Claiming expenses correctly is a core part of how to reduce Corporation Tax.

Use Capital Allowances to Reduce Corporation Tax

Capital allowances let a small business carve a bit off its taxable profit by claiming back the cost of certain assets. Common items like computers, office furniture, tools and equipment usually qualify.

Many purchases can be claimed in the same year using the Annual Investment Allowance. When used correctly, capital allowances can lower a Corporation Tax bill and are a reliable way to understand on how to reduce Corporation Tax.

Invest in Plant, Machinery & Equipment at the Right Time

The timing of larger purchases can affect how much tax a small business pays. Buying qualifying equipment before the end of the accounting year can reduce profits for that year.

For example, purchasing machinery worth £10,000 before year end can lower taxable profit and reduce the tax due. Planning these purchases in advance helps manage Corporation Tax in a legal and sensible way.

Pay Yourself a Tax Efficient Director’s Salary

Directors often pay themselves using a mix of salary and dividends. Setting the right salary level can reduce Corporation Tax while staying within National Insurance thresholds.

A low salary is usually treated as an allowable expense, which reduces profits. Dividends are paid from post tax profit but often have lower personal tax rates. This structure helps explain how to reduce Corporation Tax in a balanced way.

Make Employer Pension Contributions

Employer pension contributions made by a small business are usually tax deductible. They reduce profits and are not subject to National Insurance.

This method helps directors save for retirement while lowering the company tax bill. Pension contributions are a practical and often overlooked strategy for reducing Corporation Tax.

Claim R&D Tax Relief (If Your Business Qualifies)

Some small businesses can get their hands on Research and Development tax relief, and it is not just limited to laboratories or tech companies.

If your business is coming up with new processes, improving systems,or fixing knotty technical issues, it is worth a look. R&D relief could be the key to reduce Corporation Tax or even lead a tax refund, so it is a valuable tool that’s well worth getting your head around.

Claim Home Office & Business Use of Home Expenses

Directors who work from home can claim part of their household costs. This includes heating, electricity, broadband, and council tax in some cases.

HMRC allows either a flat rate or actual cost method. Claiming home working costs correctly helps explain how to reduce Corporation Tax without adding risk.

Claim Business Mileage & Vehicle Expenses Correctly

Using a personal vehicle for business trips allows you to claim mileage, rates are set by HMRC and it is simple to apply.

On the other hand, if you’ve got company vehicles, you might be able to claim back fuel, maintenance and even leasing costs. But the one thing you absolutely must do is keep an accurate mileage log, or else you risk getting your claim wrong.

Use Loss Relief to Offset Profits

If a small business makes a loss, it does not have to be wasted. Losses can often be carried forward or backward to reduce future or past tax bills.

Using loss relief properly can reduce Corporation Tax over several years. This is an area where professional advice is often valuable.

Plan Ahead with Professional Tax Advice

Tax planning should not be left until the filing Corporation tax deadline. A qualified accountant can spot opportunities early and avoid mistakes.

Professional advice helps small businesses apply the right reliefs and understand changing rules. This strategic approach is often the biggest factor in how to reduce Corporation Tax successfully.

In summary, these ten strategies show that reducing Corporation Tax is not about shortcuts but about planning, accuracy, and understanding the rules. When used together, they can make a meaningful difference to a small business tax position.

How to Calculate Corporation Tax

Calculating Corporation Tax correctly helps a small business avoid penalties and overpayments. Many errors happen because figures are rushed or expenses are missed.

Formula:

Taxable Profit = Income minus allowable expenses and allowances

Corporation Tax = Taxable Profit × Applicable Tax Rate

Example:

Income: £100,000

Allowable expenses: £40,000

Taxable profit: £60,000

If the tax rate is 19 percent:

£60,000 × 19 percent = £11,400 Corporation Tax due

Accurate calculations support better planning and show clearly how to reduce Corporation Tax with confidence and control.

Does a Limited Company Need an Accountant to Reduce Corporation Tax?

A limited company is not legally required to use an accountant, but professional support makes a major difference when managing Corporation Tax.

An accountant helps ensure:

- All allowable expenses are claimed

- Tax calculations are accurate

- Deadlines are met

- Reliefs are applied correctly

- HMRC rules are followed

For directors who want clarity, support, and time savings, working with an accountant is often the safest way to understand how to reduce Corporation Tax while staying compliant.

Common Mistakes That Increase Corporation Tax

Small mistakes can quietly raise the Corporation Tax bill. Below are common errors many small businesses make.

Missing Allowable Expenses

Many small businesses forget to claim everyday costs such as software, phone bills, marketing, or professional fees. When expenses are missed, profits appear higher, which increases the Corporation Tax bill unnecessarily.

Poor Record Keeping

Lost receipts and incomplete records often mean valid expenses cannot be claimed later. This usually results in higher taxable profits and makes HMRC queries harder to handle if they arise.

Incorrect Salary Planning

Paying a salary that is too high can increase National Insurance costs for both the director and the small business. A poorly structured salary can reduce tax efficiency and increase overall tax liability.

Late Planning

Waiting until the end of the accounting year removes many opportunities to reduce Corporation Tax. Good tax planning needs time, and last minute decisions often lead to missed reliefs.

Ignoring Capital Allowances

When capital allowances are not claimed, the small business misses out on tax relief for equipment and assets already purchased. This results in paying more Corporation Tax than necessary.

Claiming Ineligible Expenses

Including personal or non allowable costs can raise red flags with HMRC. Incorrect claims may lead to penalties, extra tax, and unnecessary stress for directors.

Forgetting Loss Relief

Some small businesses fail to use losses to offset future profits or past tax. This means valuable relief is wasted and Corporation Tax stays higher than it should.

DIY Tax Without Knowledge

Handling Corporation Tax without proper understanding often leads to overpayments and compliance risks. What seems like a saving upfront can cost more in the long run. Avoiding these common mistakes plays a major role in how to reduce corporation tax steadily and safely over time, while keeping a small business fully compliant with HMRC.

Ready to Reduce Your Corporation Tax and Keep More of Your Business Profits

Speak to a MyIVA tax expert today for clear, professional advice and stress-free Corporation Tax planning, all for just £325.

FAQs: Frequently Asked Questions

What is the easiest way to reduce Corporation Tax?

The easiest way is to make sure every allowable small business expense is claimed. Many small businesses overpay simply because everyday costs like software, travel, and professional fees are missed or recorded incorrectly.

Can small businesses legally reduce Corporation Tax?

Yes, small businesses can reduce Corporation Tax legally by using HMRC approved reliefs and allowances. As long as claims are accurate and supported by records, reducing tax is fully compliant and encouraged.

How often is Corporation Tax paid?

Corporation Tax is normally paid once a year, around nine months and one day after the accounting period ends. Filing on time helps avoid penalties and keeps the small business in good standing with HMRC.

Are dividends deductible for Corporation Tax?

No, dividends are not tax deductible because they are paid from profits after Corporation Tax. However, dividends are often tax-efficient for directors on a personal level when used alongside a small business salary.

Can losses reduce future Corporation Tax?

Yes, if a small business makes a loss, it can usually be carried forward to reduce future taxable profits. This helps lower Corporation Tax in later years and supports recovery during quieter periods.

Conclusion

Reducing Corporation Tax is about understanding the rules and applying them correctly. With the right planning, small businesses can lower their tax bill while staying fully compliant. Knowing how to reduce Corporation Tax allows directors to protect cash flow and plan with confidence.

MyIVA supports small businesses with fast, paperless Corporation Tax filing, expert advice, and clear guidance. Our dedicated accountants help you claim what you are entitled to and file accurately with HMRC.

Speak to a MyIVA tax expert today and reduce your Corporation Tax with confidence.