Did you know that thousands of small businesses in the UK pay more Corporation Tax than they should each year because they calculate it incorrectly? HMRC data shows that mistakes in profit calculations, missed reliefs, and incorrect deadlines are some of the most common problems found during checks.

Many small business owners know they need to pay Corporation Tax, but fewer are sure about how the final amount is calculated. The process can be confusing at first, especially with different tax rates, allowances, and reliefs involved. This is where knowing how to calculate corporate tax properly makes a real difference.

Corporation Tax is calculated by working out your taxable profits, applying the correct tax rate, and then reducing the bill using any allowances or reliefs your small business qualifies for.

In this blog, you will learn exactly how to calculate corporate income tax in the UK using clear steps, simple examples, and practical explanations. The aim is to help small businesses, sole traders operating through companies, and people responsible for tax filings understand the process and avoid common mistakes.

What Is Corporation Tax and Who Pays It?

Corporation Tax is a tax charged on the profits made by limited companies and certain other organisations. It applies to profits from trading, investments, and the sale of company assets. When people talk about how to calculate corporate income tax, they are usually referring to working out this liability correctly.

Corporation Tax is different from Income Tax. It applies to companies rather than individuals. Once a small business is registered for Corporation Tax, it must submit a Corporation Tax return each year and pay the tax due within HMRC deadlines.

Corporation Tax is paid by several types of organisations, mainly those operating as companies rather than individuals.

Who pays Corporation Tax:

- Limited companies registered in the UK

- Foreign companies with UK branches or offices

- Clubs, co-operatives, and associations

- Some unincorporated bodies that make taxable profits

Understanding who pays Corporation Tax is the first step before learning how to calculate corporate income tax accurately

UK Corporation Tax Rates Explained

Corporation Tax rates in the UK depend on the level of profit made by a small business. Since recent changes, the system now uses more than one rate, which can affect how much tax is due.

Small businesses with lower profits benefit from a reduced rate, while higher profits are taxed at the main rate. Companies that fall between the two limits receive marginal relief, which gradually increases the tax paid as profits rise.

UK Corporation Tax Rates

| Profit Level | Corporation Tax Rate |

| Up to £50,000 | 19% |

| £50,001 to £250,000 | Marginal relief applies |

| Above £250,000 | 25% |

These rates mean that knowing how to calculate corporate income tax requires understanding where your profit sits. Choosing the correct rate ensures your small business pays the right amount and avoids underpayment or overpayment.

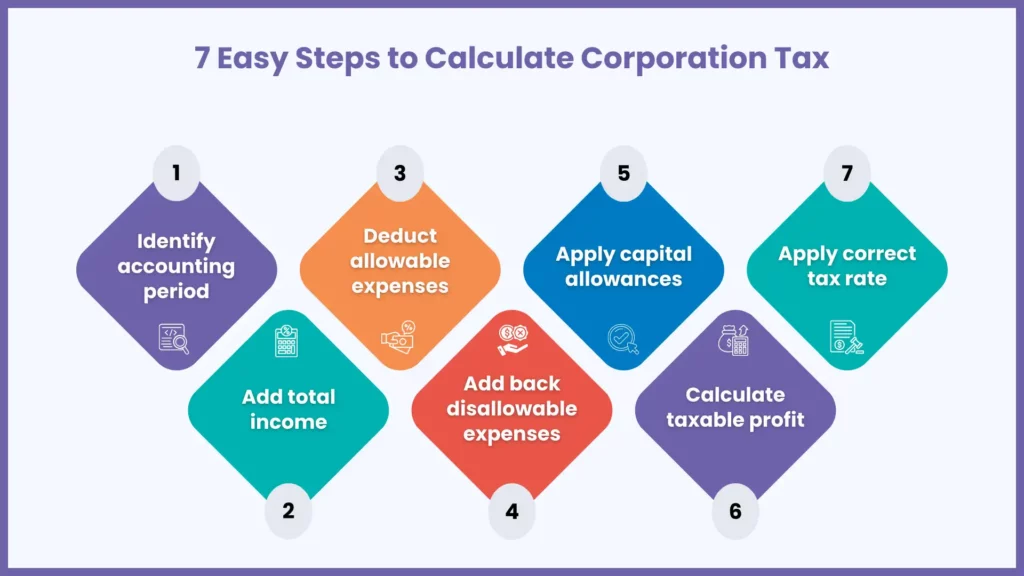

Step-by-Step: How to Calculate Corporation Tax

Calculating Corporation Tax becomes much easier when broken into clear steps. Below is a simple method used by accountants when working out how to calculate corporate income tax for a small business.

Step 1: Work Out Your Accounting Period

Your accounting period usually covers 12 months. It starts on the day your small business begins trading and ends on your chosen accounting date. All income and expenses must fall within this period.

Step 2: Calculate Your Total Income

Add together all income earned during the accounting period. This includes sales, fees, interest, and any other taxable income received by the small business.

Step 3: Deduct Allowable Business Expenses

Subtract allowable expenses such as rent, staff costs, software, professional fees, and office costs. These must be wholly and exclusively for the small business.

Step 4: Adjust for Disallowable Expenses

Some costs cannot be deducted for tax purposes, even if they appear in accounts. Common examples include fines and certain entertaining costs. These must be added back to profits.

Step 5: Apply Capital Allowances

If your small business bought equipment, machinery, or tools, you may claim capital allowances. These reduce taxable profits and play a key role in how to calculate corporate income tax correctly.

Step 6: Calculate Taxable Profit

After adjustments and allowances, the remaining figure is your taxable profit. This is the amount used to calculate Corporation Tax.

Step 7: Apply the Correct Tax Rate

Apply the appropriate Corporation Tax rate based on your taxable profit. Use marginal relief if profits fall between £50,000 and £250,000.

Following these steps ensures your small business calculates Corporation Tax accurately and stays compliant.

Corporation Tax Calculation Example

Example 1: Profit Below £50,000

A small business makes a taxable profit of £40,000.

Corporation Tax rate is 19%.

Tax due = £40,000 × 19% = £7,600.

Example 2: Marginal Relief Applies

A small business makes a taxable profit of £120,000.

This profit falls between £50,000 and £250,000, so marginal relief applies.

Marginal relief formula:

Marginal relief = (Upper limit − Profit) × 3 ÷ 200

Where the upper limit is £250,000.

Calculation:

(£250,000 − £120,000) × 3 ÷ 200

£130,000 × 3 ÷ 200 = £1,950 marginal relief

Corporation Tax at the main rate:

£120,000 × 25% = £30,000

Corporation Tax after marginal relief:

£30,000 − £1,950 = £28,050 Corporation Tax due

This gives an effective tax rate of around 23.4%.

Example 3: Profit Above £250,000

A small business makes a taxable profit of £300,000.

Corporation Tax rate is 25%.

Tax due = £300,000 × 25% = £75,000.

These examples show why it is important to understand how to calculate corporate income tax based on profit levels.

When Is Corporation Tax Due?

Corporation Tax deadlines don’t match up with those for Income Tax, which often gets small businesses into a pickle especially when they’re just starting out & trying to get to grips with things in the first year.

If either deadline gets missed, HM Revenue & Customs will be charging you interest & penalties, & may even send you a string of follow-up letters because you’ve made a late payment. Keeping track of the deadlines does help avoid incurring a whole load of extra costs, though.

Corporation Tax Deadlines

| Requirement | Deadline |

| Pay Corporation Tax | 9 months + 1 day after year end |

| File CT600 return | 12 months after year end |

| Submit company accounts | 12 months after year end |

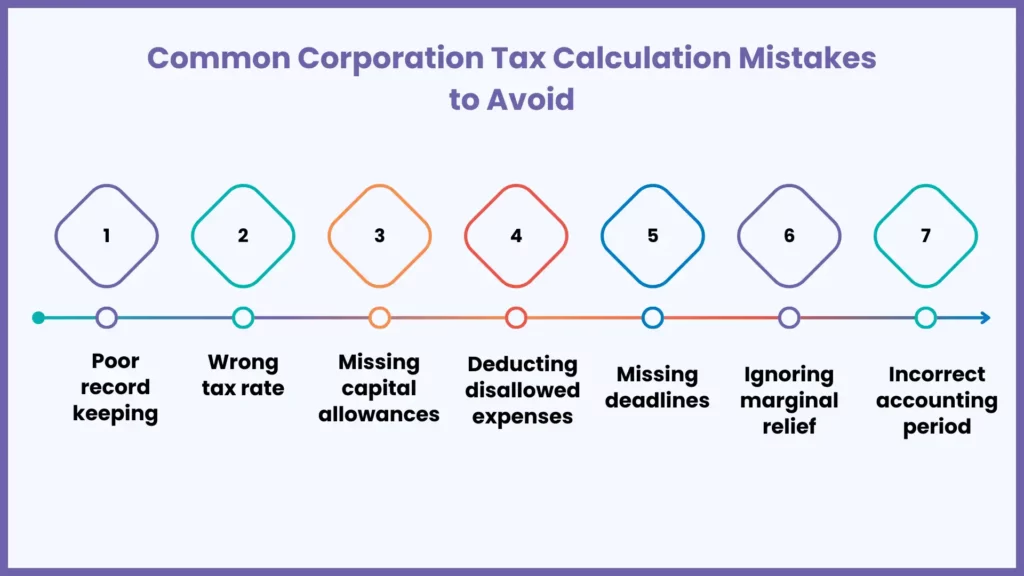

Common Corporation Tax Calculation Mistakes to Avoid

Many small businesses make errors when working out Corporation Tax. These mistakes often happen due to poor record keeping or misunderstanding the rules.

Not Keeping Proper Records

Missing invoices or expense records lead to incorrect profit figures and tax errors.

Using the Wrong Tax Rate

Applying 19% or 25% incorrectly can result in underpayment or overpayment.

Forgetting Capital Allowances

Failing to claim allowances means paying more tax than needed.

Including Disallowed Expenses

Some costs should not be deducted and must be adjusted.

Missing Deadlines

Late payment and filing cause penalties and interest.

Incorrect Accounting Period

Wrong dates can lead to duplicate or missing returns.

Ignoring Marginal Relief

Many small businesses miss this relief, which results in increase tax unnecessarily.

Not Seeking Advice

Trying to calculate tax without guidance often leads to mistakes.

Avoiding these errors helps small businesses calculate tax accurately and confidently.

Can I Delay My Corporation Tax Payment?

In short, Corporation Tax payments cannot be delayed without consequences. HMRC expects payment by the due date, and interest starts immediately after that date passes.

Penalties increase the longer payment is delayed. However, in some cases, HMRC may agree to a Time to Pay arrangement if contacted early.

Late payment penalties:

- 1 day late: No fixed penalty; interest at 7.75% begins immediately

- 3 months late: Interest continues; no additional fixed penalty for payment

- 6 months late: 10% of unpaid tax added

- 9 months late: Interest and prior penalties accumulate; further enforcement risk increases

- 12 months late: Additional 10% of unpaid tax; debt recovery actions possible

Contact HMRC promptly for Time to Pay to potentially avoid or pause further charges.

Need Help Calculating Your Corporation Tax?

Avoid costly mistakes, missed reliefs, and HMRC penalties. MyIVA’s Corporation Tax Services are available for just £325, covering accurate Corporation Tax calculations, CT600 preparation, and timely submission to HMRC.

FAQs: Frequently Asked Questions

How To Calculate corporate income tax for a new company?

Start by working out the company’s taxable profit for the accounting period. Deduct allowable expenses and apply any capital allowances. Then use the correct Corporation Tax rate based on the profit level.

Do small businesses pay Corporation Tax if they make a loss?

No Corporation Tax is due if a small business makes a loss. However, the company must still file a Corporation Tax return with HMRC. Losses can often be carried forward or back to reduce future tax bills.

Is Corporation Tax paid monthly or yearly?

Most small businesses pay Corporation Tax once a year. Payment is usually due nine months and one day after the end of the accounting period. Larger companies may have different payment rules.

Can I reduce my Corporation Tax bill?

Yes, many small businesses can reduce their tax bill by claiming allowable expenses and capital allowances. Reliefs such as marginal relief and loss relief can also lower the amount due. Accurate records are key to claiming everything correctly.

Do directors pay Corporation Tax personally?

No, Corporation Tax is paid by the company, not by individual directors. Directors pay Income Tax on salaries and dividends instead. These are separate from the company’s tax obligations.

Conclusion

Understanding how to calculate corporate income tax is essential for every small business operating as a limited company. When profits, expenses, and allowances are managed properly, Corporation Tax is much easier to handle. Following the right steps and examples helps prevent mistakes, penalties, and surprise tax bills. Staying organised and mindful of deadlines gives small businesses better control over cash flow.

MyIVA supports small businesses, sole traders, and people who file taxes by handling Corporation Tax calculations, returns, and payments accurately. If you want peace of mind and expert support, contact MyIVA today and let professionals manage your Corporation Tax with confidence.