Every year, millions of UK taxpayers are required to submit a Self Assessment return to HM Revenue and Customs. As 31 January draws closer, a significant proportion have still not filed. In recent years, more than five million returns were outstanding just weeks before the cut-off. That leaves a large number of people exposed to automatic penalties they could quite easily have avoided with a bit of earlier action.

Here is the part most people do not fully appreciate until it is too late. Missing the deadline brings an immediate £100 fine, and it does not matter whether any tax is actually owed. It does not matter whether the tax has already been paid. The moment the deadline passes, the penalty is issued. No warning. No second chance.

This article covers what the current HMRC warnings mean in practice, why so many people still miss the deadline year after year, how penalties stack up over time, who tends to be most at risk, and what sole traders, small firms and individuals can actually do to keep themselves out of trouble.

Millions Yet to File as HMRC Confirms Self Assessment Figures

Each January follows a similar pattern. HMRC publishes updates showing how many taxpayers have filed and how many are still outstanding. The figures often show millions waiting until the final month and hundreds of thousands filing in the final days.

There are practical reasons behind this. Many sole traders focus on keeping their work moving in January rather than sorting paperwork. Landlords may assume rental income is simple and delay gathering expense records. Company directors sometimes believe their company accounts cover all obligations, overlooking their personal filing requirement.

However, HMRC Tax Warnings make one thing clear. If you are registered for Self Assessment, you must submit a return unless HMRC confirms otherwise. Ignoring reminders or assuming no tax is due does not remove that obligation.

For example, a self-employed tradesperson who made very little profit during the year may assume filing is unnecessary. Yet if they remain registered for Self Assessment, the return is still required. When it is not submitted, the £100 penalty is issued automatically. The fine relates to late filing, not to the level of income earned.

HMRC systems apply the initial penalty automatically once the deadline passes. That is why these HMRC Tax Warnings are repeated so strongly in the weeks leading up to 31 January.

Note: If you’re unsure about your Self Assessment obligations, check our guide on how to register for Self Assessment.

What Happens If You Miss the Self Assessment Deadline

Missing the deadline rarely remains a minor issue. What begins as a £100 penalty can increase if the return remains outstanding or tax remains unpaid.

Below are the main consequences explained clearly.

1. £100 Automatic Late Filing Penalty

This is charged immediately after the deadline. It applies regardless of whether tax is owed.

2. Daily Penalties After Three Months

If the return is still outstanding three months later, HMRC can charge £10 per day for up to 90 days. This can total £900.

3. Six Month Additional Penalty

At six months late, a further penalty is applied. This is usually 5% of the tax due or £300, whichever is higher.

4. Twelve Month Additional Penalty

After twelve months, another 5% or £300 minimum penalty is charged.

5. Late Payment Penalties

If tax has not been paid, separate penalties apply in addition to filing penalties.

6. Interest on Outstanding Tax

Interest runs from the original payment deadline until the balance is cleared.

7. Increased Compliance Risk

Repeated late filing may increase the likelihood of further HMRC review in future years.

The consistent message in recent HMRC Tax Warnings is that delay increases cost. Filing promptly limits the damage.

Full HMRC Penalty Escalation Timeline

Missing a Self Assessment deadline and getting into trouble with HMRC isn’t just a case of getting slapped with a single fine. They slap penalties on you in stages and each stage just piles more money onto the bill.

1. Immediate Late Filing Penalty of £100

When the deadline comes and goes, HMRC applies a fixed £100 penalty and that’s even if you’ve got a pretty standard situation.

• No tax is owed

• Tax has already been paid

• The return is only one day late

No reminder is required before this penalty is triggered.

2. Three Months Late – Daily Penalties

After three months, HMRC may charge £10 per day for up to 90 days.

This can add £900 to the original £100 fine. Filing the return stops further daily penalties.

3. Six Months Late – Additional 5% Penalty

At six months, a further penalty applies. This is generally 5% of the tax due or £300, whichever is higher.

Even where tax due is small, the £300 minimum may apply.

4. Twelve Months Late – Further 5% Penalty

After twelve months, another 5% or £300 minimum penalty is charged.

In serious cases involving deliberate non-disclosure, higher penalties may apply.

Late Payment Penalties

Late payment penalties are separate from filing penalties. If tax remains unpaid, additional 5% charges can apply at 30 days, six months and twelve months after the payment deadline. Interest continues throughout.

Why Acting Early Matters

HMRC Tax Warnings exist to encourage early action. Filing quickly keeps penalties to a minimum. Once additional stages are triggered, resolving the issue becomes more expensive and more stressful. Early response protects cash flow and reduces long term risk.

HMRC Statement Urging Taxpayers to Act Now

HMRC repeatedly advises taxpayers not to leave filing until the final hours. Online systems become busy close to midnight, and technical problems are rarely accepted as reasonable excuses for late submission.

The financial impact is straightforward:

| Stage of Delay | Penalty |

| 1 day late | £100 fixed penalty |

| 3 months late | £10 per day up to £900 |

| 6 months late | 5% of tax due or £300 |

| 12 months late | Further 5% or £300 |

| Late payment | Separate 5% charges plus interest |

HMRC’s position is clear. File on time. If payment is difficult, contact them early rather than ignoring the issue. Most HMRC Tax Warnings are preventable with early action.

Support and Services Available on Deadline Days

Even if filing is left until the final day, support remains available.

1. Online Filing Portal

The online system provided by HM Revenue & Customs operates 24 hours a day. Returns can be submitted up to 11.59pm on the deadline date.

2. Online Payment Facilities

Tax due can be paid electronically using approved methods. Ensuring correct payment references are used helps avoid allocation delays.

3. Time to Pay Arrangements

Where full payment is not possible, eligible taxpayers may apply for a Time to Pay arrangement. Interest will apply, and approval depends on compliance history and debt level.

4. Professional Review

A small firm experienced in Self Assessment can review figures, confirm expenses and identify missing income before submission. Even last-minute advice can prevent errors.

5. Final Hour Filing Still Prevents the £100 Fine

Submitting before midnight avoids the automatic late filing penalty. Once the deadline passes, the system applies the fine automatically.

Even on the final day, timely action can prevent unnecessary penalties. Submitting before midnight ensures compliance and avoids the automatic £100 fine, protecting your record for the year ahead.

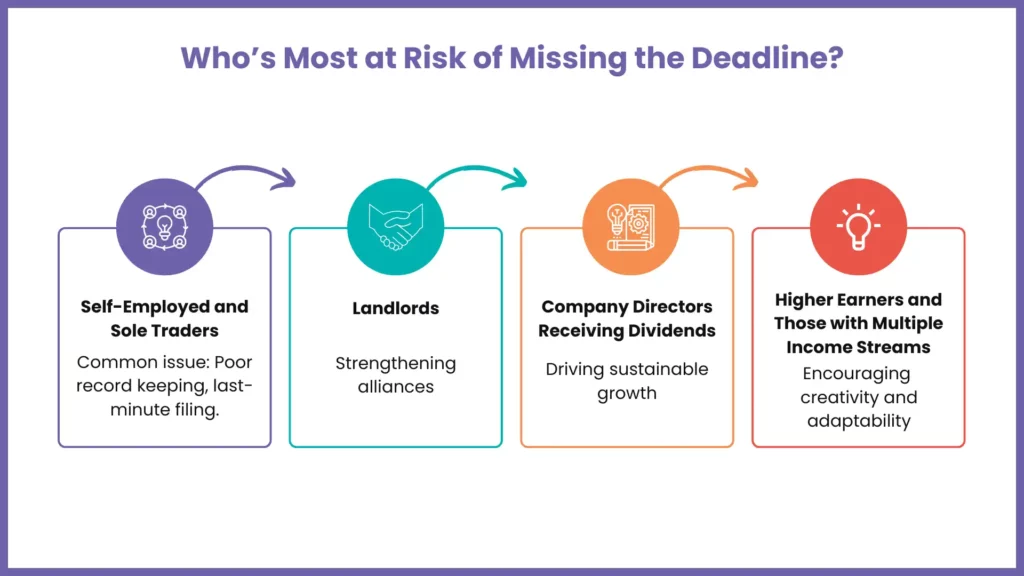

Groups Most Affected by the Self Assessment Deadline

Certain groups face greater exposure to HMRC Tax Warnings.

1. Self Employed Individuals and Sole Traders

They calculate their own income and expenses. Without organised records, filing becomes difficult as January approaches.

2. Company Directors Receiving Dividends

Dividends and other untaxed income must be reported separately from company accounts. Personal filing obligations remain.

3. Landlords

Rental income must be declared accurately, and allowable expenses must be calculated correctly. Reporting errors are common where records are incomplete.

4. Higher Earners and Those with Additional Income

Individuals receiving dividends, foreign income, capital gains or side business income may be required to file even if tax has been deducted elsewhere.

5. Individuals with lots of different income streams

If you’ve got multiple income streams and not all of it is being taxed at source, then the responsibility for getting it all sorted falls on you. That just increases the risk of things going wrong if those deadlines get missed.

For people in those kinds of situations, it’s really important to get your paperwork sorted early and to get your reporting accurate so you can avoid any penalties, extra interest and certainly any scary compliance checks that can come with missing deadlines. Knowing your own filing obligations and keeping on top of your records throughout the year really does make a big difference in avoiding last-minute stress and HMRC taking a close look at your affairs.

Upcoming: Making Tax Digital for Income Tax (MTD ITSA)

From 6 April 2026, MTD for Income Tax requires self-employed individuals and landlords with over £50,000 turnover to maintain digital records and file quarterly updates using compatible software (threshold drops to £30,000 in 2027).

Non-compliance triggers a points-based system, with automatic £200 fines per breach, on top of Self Assessment late filing penalties.

This shift from annual to quarterly reporting amplifies risks for sole traders; start adapting records now to sidestep HMRC escalation.

Separate HMRC Warning Letters Being Sent to Savers

In addition to broader compliance reminders, HM Revenue & Customs has been contacting individuals whose savings interest may exceed their Personal Savings Allowance. With interest rates having risen in recent years, more taxpayers are finding that modest savings balances now generate taxable interest.

The current allowances remain:

- Basic rate taxpayers – up to £1,000 tax free

- Higher rate taxpayers – up to £500 tax free

- Additional rate taxpayers – no Personal Savings Allowance

Banks and building societies report annual interest payments directly to HMRC. Where this data does not align with what has been declared (or where no return has been filed despite interest exceeding allowances), HMRC may issue a nudge or warning letter.

In many cases, these letters are not automatic penalties but requests for clarification. However, ignoring them can escalate matters. If discrepancies remain unresolved, HMRC may amend tax codes, issue assessments, charge interest on underpaid tax, or begin formal compliance checks. Reviewing savings income annually and checking tax codes carefully can prevent unexpected liabilities.

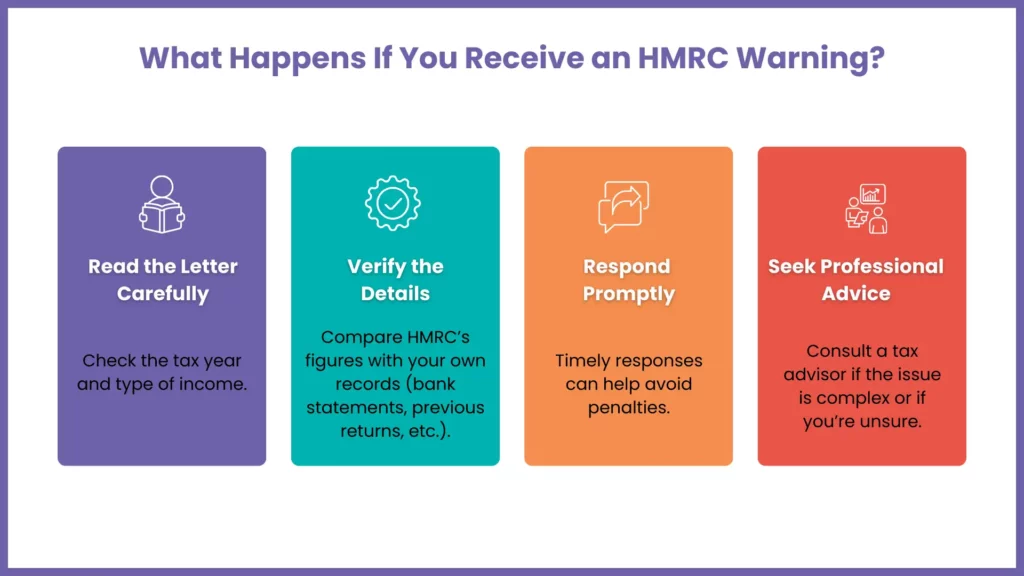

What to Do If You Receive a Tax Warning Letter

If you receive a letter from HM Revenue & Customs, do not panic. Follow these practical steps:

Step 1: Read the Letter Carefully

Check the tax year, the type of income referenced, and what action HMRC is requesting. Some letters are reminders, while others request clarification or payment.

Step 2: Verify the Details Against Your Records

Compare HMRC’s information with your own documents, including:

- Bank statements (interest received)

- Dividend vouchers

- Rental income records

- Previous Self Assessment returns

- PAYE coding notices

Identify whether there is a genuine discrepancy.

Step 3: Confirm the Accuracy

When verifying records, consider if you need to amend Self Assessment tax return for prior years, act within the 12-month window to avoid formal checks. If HMRC’s figures are correct and income was missed, calculate the potential tax due. If the information appears incorrect, gather supporting evidence to demonstrate why.

Step 4: Respond Promptly

Do not ignore the letter. Timely responses often reduce the risk of penalties. HMRC generally takes a more reasonable approach where taxpayers cooperate and engage early.

Step 5: Seek Professional Advice if Unsure

If the issue involves multiple income streams, complex calculations, or potential underpayment, consult a qualified tax adviser. Early professional guidance can prevent interest, penalties, or a compliance check from escalating further.

Taking structured action quickly protects your position and keeps the matter manageable.

HMRC Warns Taxpayers to Stay Alert to Scams

Tax deadlines often bring a surge in scam activity, with fraudsters exploiting urgency and anxiety. Criminals frequently impersonate HM Revenue & Customs through emails, text messages, phone calls, and even social media, claiming refunds are due or demanding immediate payment to avoid penalties.

Common red flags include:

- Threats of arrest or legal action if payment is not made immediately

- Requests for full banking passwords or sensitive security details

- Links directing you to unofficial websites

- Messages creating pressure to act “within hours”

HMRC does not demand payment through gift cards, cryptocurrency, or direct threats over the phone. It also does not request full passwords or sensitive banking credentials.

If in doubt, taxpayers should avoid clicking on links within messages and instead log in directly to their official HMRC online account through the government website. Remaining cautious during deadline periods protects both finances and personal data, and helps prevent becoming a victim of tax-related fraud.

Avoid HMRC’s £100 Fine – Self Assessment Help for Only £99

HMRC is issuing a tax warning. Don’t miss the Self Assessment deadline! Get professional help for just £99 to file your return on time and avoid a £100 fine. Act now!

FAQs: Frequently Asked Questions

Do I need to file if I made no profit?

Yes, if you are registered for Self Assessment, you must still submit a return. Only HM Revenue & Customs can confirm if filing is no longer required.

What if I miss the deadline by one day?

A £100 penalty is issued automatically once the deadline passes. Filing immediately helps prevent additional penalties.

Can I appeal a penalty?

Yes, appeals are allowed where there is a genuine reasonable excuse. Evidence must be provided to support your claim.

Should I file if I cannot pay?

Yes, submitting the return on time avoids further filing penalties. Payment arrangements can be discussed separately.

How can small firms reduce risk each year?

Maintain accurate records and monitor income regularly. Seeking early professional advice significantly reduces compliance risk.

What about tax scams near deadlines?

Verify via gov.uk or HMRC app, ignore unsolicited demands. Report phishing emails to phishing@hmrc.gov.uk or contact Action Fraud directly.

Conclusion

The latest HMRC Tax Warnings underline how firm the Self Assessment system is. The £100 penalty is automatic. Further penalties build in stages. Interest continues until payment is made.

For sole traders, landlords, company directors and individuals with additional income, staying organised and filing early is the safest approach.

MyIVA supports small firms, sole traders and individuals across the UK with accurate Self Assessment preparation and submission. If you have received a warning or are concerned about a missed deadline, taking advice now can prevent further penalties and restore control over your tax position.