The UK Chancellor Rachel Reeves presented the Autumn Budget on 26 November 2025. This budget included various tax changes that will impact millions of taxpayers. It was crucial because it addressed personal tax, corporate tax, and long-term financial planning. Small businesses, sole traders, and individual taxpayers will experience the most significant effects in the coming years.

The Chancellor described the budget as a plan to stabilize public finances while also supporting investment in key sectors. Much of the focus was on freezing income tax thresholds, raising dividend taxes, changing rules for landlords, and altering corporate tax allowances. These measures set the direction for the government’s tax policies into the early 2030s.

Key Tax Changes at a Glance

| Category | What Has Changed | Old Position | New Position | When It Starts |

| Income Tax | Thresholds frozen | £12,570 / £50,270 / £125,140 | No change | Until April 2031 |

| VAT | No change in thresholds, e invoicing coming | Current VAT limits | Digital VAT invoices required | April 2029 |

| R&D and Transfer Pricing | Rules simplified | Older rules | Streamlined approach for small and growing firms | From 2026 |

| Dividend Tax | Rates increased by 2 points | 8.75% / 33.75% | 10.75% / 35.75% | April 2026 |

| Property Income Tax | Separate higher rates | Taxed within income bands | 22% / 42% / 47% | April 2027 |

| Savings Income Tax | Rates increased by 2 points | Current rates | All bands increase by 2 points | April 2027 |

| Cash ISA (Under 65) | Allowance reduced | £20,000 | £12,000 | April 2027 |

| Corporation Tax | Main rate unchanged | 25% | 25% | Ongoing |

| Capital Allowances | Writing down reduced | 18% | 14% and new 40% first year allowance | April 2026 / Jan 2026 |

| Business Rates | Permanent reductions for key sectors | Temporary support | Permanent support worth £900m | April 2026 |

| State Pension | Increase confirmed | Current rate | +4.8% to £12,547 per year | April 2026 |

Below is a clear summary of the most important tax changes and what they mean for personal taxpayers and small firms.

Personal Tax Changes

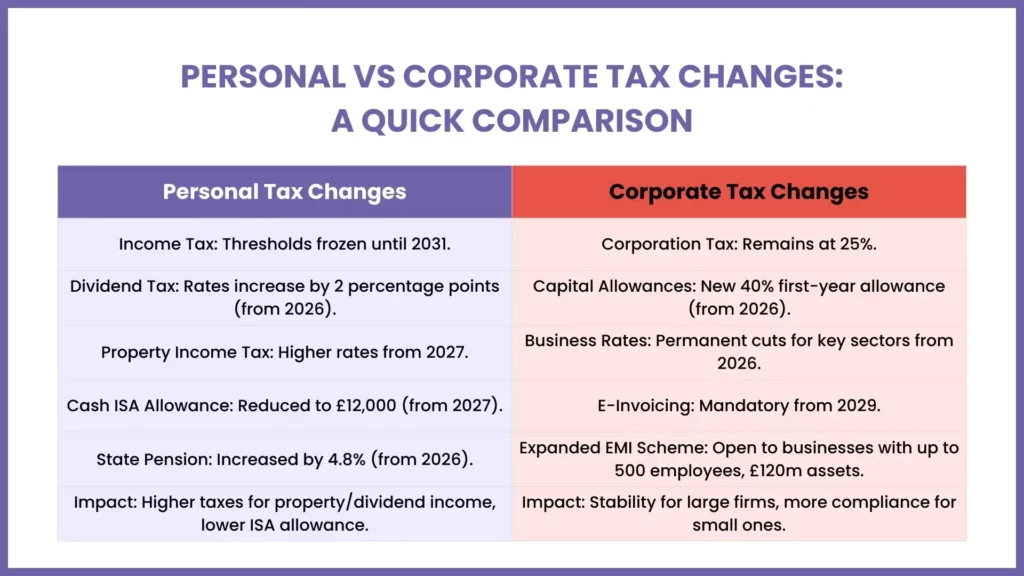

Income Tax Thresholds Frozen Until 2031

The personal allowance will stay at £12,570 until April 2031. The higher rate threshold remains at £50,270 and the additional rate threshold stays at £125,140. National Insurance thresholds for employees and self-employed people will also remain frozen between April 2028 and April 2031.

This freeze pulls more workers into higher bands as wages rise. It has already been described as a hidden tax rise. Government figures show it is expected to raise more than £8 billion by 2029 to 2030.

Dividend Tax Rates Going Up

From April 2026, dividend tax will increase by 2 percentage points. The basic rate rises to 10.75 percent and the higher rate rises to 35.75 percent. The additional rate stays the same. The dividend allowance remains at £500.

This change will hit directors of small limited companies who take profits as dividends instead of salary.

Higher Tax Rates for Property Income

From April 2027, property income will be taxed separately at higher rates. The new rates will be 22 percent for basic rate taxpayers, 42 percent for higher rate taxpayers and 47 percent for additional rate taxpayers. This is a 2-percentage point increase for every band.

Landlords in England, Wales and Northern Ireland will be affected.

Savings Income Tax Rise

Savings income will also see a 2-percentage point rise from April 2027. The government says more than 90 percent of taxpayers will not be affected because they have no taxable savings income.

Cash ISA Allowance Cut

From April 2027, people under 65 will see their cash ISA limit fall from £20,000 to £12,000. The stocks and shares ISA limit stays at £20,000.

Pension Salary Sacrifice Cap Introduced

From April 2029, National Insurance relief on salary sacrifice pension contributions will be capped at £2,000 per employee each year. Most basic rate taxpayers will not be affected, but higher earners who make large pension contributions through salary sacrifice will pay more NICs above this limit.

Council Tax Surcharge on High Value Homes

From April 2028, homes worth £2 million or more will pay a new annual surcharge. Charges start at £2,500 and rise to £7,500 for homes valued above £5 million. This applies to properties in England and affects fewer than one percent of homes.

State Pension Increase Confirmed

The state pension will rise by 4.8 percent from April 2026. The new state pension will increase to £12,547 a year.

Reduced CGT Relief for Employee Ownership Trusts

From 26 November 2025, capital gains tax relief on disposals to Employee Ownership Trusts drops from 100 percent to 50 percent.

Mileage based Charge for Electric Vehicles

From April 2028, electric and plug in hybrid cars will face a new mileage-based charge. EV drivers will pay around half of the fuel duty paid by petrol and diesel drivers. The average cost is expected to be around £240 per year.

Corporate Tax Changes

Corporation Tax Rate Unchanged

The main corporation tax rate stays at 25 percent. The government says this keeps the UK competitive within the G7. There are no changes to headline rates.

New Capital Allowances and Adjustments

A 40 percent first year allowance for main rate assets starts on 1 January 2026.

The writing down allowance for main rate assets reduces from 18 percent to 14 percent from April 2026.

Full expensing for main rate plant and machinery continues.

The £1 million Annual Investment Allowance remains.

These changes encourage investment but may increase tax bills for companies with slower asset depreciation.

Business Rates Reform

Lower business rates will be made permanent for retail, hospitality and leisure sectors from April 2026. This support package is worth nearly £900 million a year.

Firms expanding into a second property will benefit from a longer Small Business Rates Relief grace period, now increased from one year to three years.

A higher business rates multiplier will apply to properties with rateable values above £500,000.

Mandatory E Invoicing

From April 2029, all VAT registered businesses must use e invoicing software that meets government standards.

Digital Compliance Investment

The government is investing £59 million to introduce digital prompts for VAT and corporation tax filing software. Late filing penalties for corporation tax will double from April 2026.

Expanded EMI Scheme

From April 2026, the EMI scheme will allow companies with up to 500 employees and gross assets up to £120 million to qualify. The company share option limit rises to £6 million.

R&D and Transfer Pricing Reform

New rules will simplify the tax treatment of related party transactions, non-resident companies and profits diverted from the UK.

VAT Update

No changes to VAT thresholds or rates.

However, private hire vehicle operators will no longer be able to use administrative schemes intended for tour operators from January 2026.

Employer NICs

Employer National Insurance contribution rates remain unchanged. Plans to apply NICs to LLP profits have been dropped.

Gaming and Betting Duties

Remote Gaming Duty rises from 21 percent to 40 percent from April 2026. A Remote Betting Rate of 25 percent begins from April 2027. Bingo Duty will be removed from April 2026.

Impact on Small Businesses and Sole Traders

Small firms and sole traders will feel the effects of tax threshold freezes, higher dividend taxes and new rules for property income. Directors who pay themselves with salary and dividends will see higher overall tax bills from 2026. Landlords will see higher property income tax from 2027. The freeze on income tax thresholds continues to draw more small business owners into higher bands.

For companies, maintaining the 25 percent corporation tax rate offers stability, but changes to capital allowances and higher digital compliance requirements will bring added planning needs. Sectors such as retail and hospitality will benefit from lower business rates, which should ease cost pressures in 2026.

Unsure how the 2025 Autumn Budget affects you or your business? Let MyIVA help you navigate the new rules and plan for the future. Contact us today for expert advice and support!

Key Takeaways

- Income tax thresholds frozen until 2031

- Dividend tax rising from April 2026

- Higher property income tax rates from 2027

- Savings tax and ISA changes for younger savers

- New EV mileage charge from 2028

- Corporation tax rate remains 25 percent

- Capital allowances updated, full expensing continues

- Permanent cuts to business rates for key sectors

- E invoicing required from 2029

- Increased support for investment and EMI schemes

Need Support Understanding These Changes

If you are unsure how the Autumn Budget affects your tax position, MyIVA can help you understand what the new rules mean for your income, investments or small firm. Our team can guide you through the updates and help you stay prepared for the changes coming over the next few years.